What it Means to Make a Gift Under the Federal Gift Tax System

The legal, accounting, insurance and wealth management professions are constantly telling us what it means to make a gift and why it is important. I am guilty of that myself and I am not talking about giving a bottle of champagne to a dear friend to celebrate an occasion. I am talking about something far more exciting than that … the Federal Gift Tax system under the Internal Revenue Code (IRC). I spend hours writing articles and creating case studies to help people understand how gifting works, but I do not believe I have ever detailed the basic tenants of gifting under the IRC. This is my attempt to break it down, but I must admit that it is a little bit like telling people how a watch is made when all they want to know is the the time.

THE FEDERAL GIFT TAX

There are three concepts that are intrinsically tied together that we must understand first, so let’s break them down one at a time.

1. The Annual Exclusion Gift

The IRS says that a gift is “any transfer to an individual, either directly or indirectly, where full consideration (measured in money or money’s worth) is not received in return”. Any taxpayer is allowed to gift, to any individual, an amount of up to $15,000 per year without paying a gift tax. This amount is indexed annually but goes up in increments of $1,000.

Contrary to what many people believe, a gift tax IS NOT paid by the recipient of the gift, but rather by the person making the gift should he or she exceed the annual exclusion amount. A gift DOES NOT create an income tax deduction for the person making the gift, so there is no income tax benefit to the taxpayer making the gift, just as there is no taxable income to the recipient and hence no income tax due. A taxpayer can give (gift) $15,000 to as many people as he or she may want without paying any gift taxes. Let’s say that I have 2 children and I had $30,000 burning a hole in my pocket, I could give (gift) them each $15,000 with none of the parties paying a tax (gift or income) or even having to file a gift tax return. It is a bit of an honor system.

If my spouse wanted to do the same, collectively, we could give (gift) our two kids $60,000 ($15,000 each, times 2 kids, times 2 spouses). We could also make gifts to our grandchildren, to our nephews and nieces, or to anybody we wanted to, just so long as each gift does not exceed $15,000.

2. The Lifetime Gift Tax Exemption

The IRS is actually very friendly, so long as you play by their rules. They give you “a pass” if you want to gift more than $15,000 without paying a gift tax, but you must report and track any amounts gifted over the $15,000. This is where the Lifetime Exemption comes into play. Currently, in 2020, the Lifetime Exemption is $11,580,000 – yes, you read that right – ELEVEN MILLION, FIVE HUNDRED AND EIGHTY THOUSAND DOLLARS. This amount is also indexed annually and goes up every year based on IRS guidelines for indexing or adjusting for inflation.

As I said, the IRS is a very friendly governmental agency, so much so, that a married couple can actually double that amount and give (gift) away $23,160,000 in their lifetime, PLUS all the annual exclusion gifts that they can afford. But how exactly does this work?

Let’s say that I know 772 people and I want to give (gift) them all $15,000. How much gift tax would I have to pay? The answer is – ZERO. 772 times $15,000 equals $11,580,000, but that is a trick question. Those gifts would ALL qualify under the annual exclusion amounts so I would not even have to file a gift tax return.

I could however, give (gift) the $15,000 to 771 people AND give (gift) $11,595,000 ($11,580,000 + $15,000) to my favorite nephew and still pay ZERO gift tax, but in this scenario I would have to file with the IRS Form 709, which is the “United States Gift (and Generation Skipping Transfer) Tax Return”, reporting that I gifted the $11,580,000 above the annual exclusion amount to my nephew.

Clear as mud?

Let me try again. I have 2 children and my spouse and I want to give (gift) them each $100,000. What we know is that we can each give (gift) them $15,000 each no problem. That is $30,000 per child as a married couple. We would have to file Form 709 in 2020 reporting a taxable gift to each child in the amount of $70,000 ($100,000 gift minus the $30,000 annual exclusion), thereby using part of the $11,580,000 exemption each and reducing it to $11,510,000 for each of us.

3. The Lifetime Estate Tax Exemption

The Estate Tax Exemption and the Gift Tax Exemption are the same amount at $11,580,000 and they coexist to make sure that what you give away in your lifetime reduces the amount that you can transfer to your heirs estate tax free at your death.

To follow the example from above, if I died next year after making a $100,000 gift in 2020, I would have $11,510,000 left of my estate exemption, adjusting for whatever inflation factor 2021 brings, because as I said before, the IRS is a very friendly governmental agency.

The gift and estate tax rates are 40% of any taxable gift OVER the lifetime exemption or of the taxable estate, if the exemption has not been previously used. The taxpayer does not HAVE to use their estate exemption amount for gifts in excess of the annual exclusion amount and could in fact pay the gift tax in the year in which it is due and preserve the estate exemption … but nobody does that – it doesn’t make mathematical sense. Once the entire gift tax exemption is used, then a gift tax is due if gifts exceed the annual exclusion amount.

WHY IS FINANCIAL GIFTING IMPORTANT TODAY?

The Tax Cut and Jobs Act (TCJA) of 2017 temporarily doubled the gift and estate tax exemptions  from $5,000,000 to $10,000,000 per taxpayer, with the ensuing indexing amount – currently at the $11,580,000 mentioned above. TCJA has what is called a “sunset provision” which takes effect on January 1, 2026 and absent any legislative action, the exemption amount will revert back to pre-2017 levels, adjusted for inflation.

from $5,000,000 to $10,000,000 per taxpayer, with the ensuing indexing amount – currently at the $11,580,000 mentioned above. TCJA has what is called a “sunset provision” which takes effect on January 1, 2026 and absent any legislative action, the exemption amount will revert back to pre-2017 levels, adjusted for inflation.

This means that in 2026, affluent taxpayers will lose their opportunity to “double-up” on gifting. This is meaningful for large estates. There was some initial concern among advisors that if a taxpayer made a gift for the additional $5,000,000 (the effective doubling up) that the IRS could later come back and “claw it back” into the estate and tax it. There has been definitive guidance at this point that the IRS WILL NOT claw back any gifts prior to 2026 that exceeds the pre-2017 TCJA amount.

A bigger issue may come sooner than 2026, as COVID has caused massive increases in the US National Debt and Congress is already looking for ways to increase tax revenue. Should the Democrats win, I believe that the writing is on the wall. There are already proposals from the Biden camp that the Gift and Estate Tax Exemption would decrease to $3,500,000 per taxpayer.

WHY MAKE A FINANCIAL GIFT NOW?

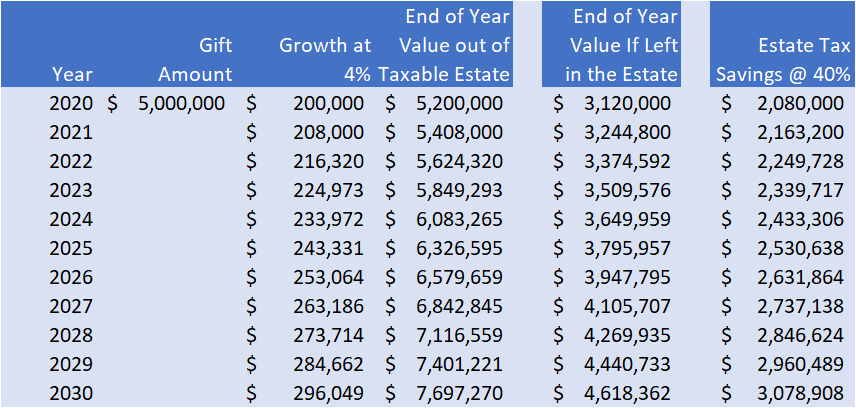

If a taxpayer has a significant estate or expects to have a significant estate (growth, inheritance, or otherwise), then it would be a big mistake not to take advantage of this temporary opportunity to make a gift either outright to descendants or to a trust for the benefit of those descendants. Consider the following example. A taxpayer makes a gift today of $5,000,000. Remember – ZERO Gift Tax and ZERO Clawback. That $5,000,000 plus all the growth is now forever out of the client’s estate. By 2030, that is almost a $3,100,000 increase to the transferred wealth!

Further strategies to enhance that wealth transfer leverage can be deployed with life insurance in the trust, essentially doubling or more (depending on a variety of factors) the wealth transfer effect of that gift.

The biggest objection to the question of “why not gift the money now?” is “well, what would happen if I needed the money later in my life?”. There are ways to provide access to the funds gifted to a trust that are commonly used, such as Spousal Lifetime Access Trust. A good financial advisor, along with a trust and estate attorney, will be very familiar with these tools.

There are also strategies that combine gifts with the sale of assets to a trust in exchange for a note to the grantor (the person making the gift) that provide an enormous amount of flexibility during this time of uncertainty as to what will happen to the Gift and Estate Tax regime in the United States. And considering that interest rates on intra-family loans or notes are at record lows, there has never been a better time to implement these planning strategies.

Don’t let uncertainty, or worse, ignorance, derail your wealth transfer plans and goals. The government is banking on that and will gladly take 40% of what you leave to your children, grandchildren or other loved ones.

AgencyONE has a variety of strategies to assist you with your clients’ estate and financial planning goals. Please call AgencyONE’s Marketing Department for more information or to discuss a case.

")