Long-Term Care and Survivorship Insurance

I recently spoke with a friend whose father just transitioned into a nursing home. Since I have a parent in a similar situation, we were able to talk about the costs of long-term care coverage and the “crazy” overall expense. The Genworth Cost of Care Calculator shows the average cost of a private room in a Washington, D.C./ Maryland nursing home facility is $13,049 per month. In Tampa, FL (where my mother is located) the average projected cost is $9,885 per month. Those are the costs at the time of this writing (February 2022). My friend and I also discussed what might happen as we age and possibly need the same kind of Long-Term Care (LTC) coverage. Using the calculator to look out 20 years, the projected costs INCREASED to $23,568 per month in MD/DC and $17,853 in Tampa!! Insane increases!

I recently spoke with a friend whose father just transitioned into a nursing home. Since I have a parent in a similar situation, we were able to talk about the costs of long-term care coverage and the “crazy” overall expense. The Genworth Cost of Care Calculator shows the average cost of a private room in a Washington, D.C./ Maryland nursing home facility is $13,049 per month. In Tampa, FL (where my mother is located) the average projected cost is $9,885 per month. Those are the costs at the time of this writing (February 2022). My friend and I also discussed what might happen as we age and possibly need the same kind of Long-Term Care (LTC) coverage. Using the calculator to look out 20 years, the projected costs INCREASED to $23,568 per month in MD/DC and $17,853 in Tampa!! Insane increases!

So, what are the options for managing these potential costs instead of self-funding? Remember, it’s only considered TOO LATE to start planning if you ALREADY NEED the coverage. Start planning NOW. The younger you start the lower the costs are to obtain LTC coverage. However, for some, the money is not available early on to buy the coverage. Other financial obligations such as kids in school, new drivers in the household, college tuition, and other expenses may take priority over funding LTC coverage. My buddy and I quickly agreed never to go into a managed care facility, dropped the subject, and switched to something more fun to discuss.

you ALREADY NEED the coverage. Start planning NOW. The younger you start the lower the costs are to obtain LTC coverage. However, for some, the money is not available early on to buy the coverage. Other financial obligations such as kids in school, new drivers in the household, college tuition, and other expenses may take priority over funding LTC coverage. My buddy and I quickly agreed never to go into a managed care facility, dropped the subject, and switched to something more fun to discuss.

Long-Term Care Facts

The facts and circumstances surrounding long term care coverage should be considered seriously. Following are a few sobering facts from the Genworth Cost of Care website:

- 7 of 10 people over the age of 65 will need some type of long-term care support;

- 66% of caregivers used their own retirement and savings to pay for care; and

- 100% of their families are affected in some way.

Long-Term Care Options for Coverage

Current options to obtain LTC coverage include stand-alone products, life products with LTC/Chronic riders, and hybrid products. These options give the client a variety of ways to approach obtaining coverage. I have illustrated countless scenarios over the years and am aware of a carrier partner that offers a joint Universal Life solution that can provide LTC benefits on both clients (spouses). This product can also be guaranteed if needed (depending on client ages). Did you know that you can write this joint policy on a PARENT AND CHILD as the insureds (depending on client ages)?

Current options to obtain LTC coverage include stand-alone products, life products with LTC/Chronic riders, and hybrid products. These options give the client a variety of ways to approach obtaining coverage. I have illustrated countless scenarios over the years and am aware of a carrier partner that offers a joint Universal Life solution that can provide LTC benefits on both clients (spouses). This product can also be guaranteed if needed (depending on client ages). Did you know that you can write this joint policy on a PARENT AND CHILD as the insureds (depending on client ages)?

This joint SUL product can assist with:

- Legacy or estate planning strategies;

- Accessing the accumulation value of the policy (if needed and depending on the initial design);

- Protecting a family member with special needs; and

- Providing an additional LTC rider which can cover one or both clients (additional underwriting is required).

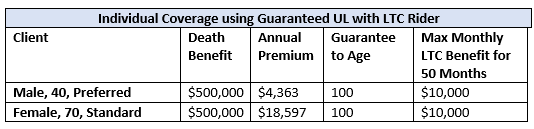

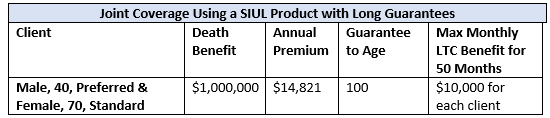

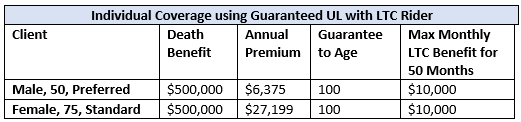

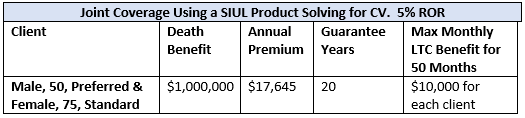

Long-Term Care Comparison – Individual vs Joint Coverage

Let’s look at a comparison of costs using an Individual Guaranteed UL product and a Joint Survivor IUL product with a Guarantee Rider.

The following scenario includes a parent over the age of 70. For individual coverage, we can use a Guaranteed UL product with an LTC rider. With the joint coverage option, the LTC rider is available up to age 80 while the Guaranteed option is not available beyond the age of 70. The premium solve is to age 121 and assumes an indexed return of 5% in all years.

Long-Term Care – Comparison Results

This individual versus joint coverage question results in a very interesting comparison with the JOINT OPTION making more sense for a variety of reasons:

- It offers a significant cost savings compared to the two individual options.

- It can help cover LTC costs down the road for both the mother and the son (1/2 of the death benefit is available for each insured), assuming both clients qualify.

- The product has a monthly cash indemnity benefit which offers more options for the clients.

- The beneficiaries will receive any remaining death benefit if one or both insureds use only a portion of the LTC benefits.

- The beneficiaries will receive the full death benefit upon the second death assuming the insureds have not used the LTC benefits.

AgencyONE Case Designers are experts in carrier product intelligence and work collaboratively with our AgencyONE 100 advisors to develop a design that fulfills their client’s risk, financial, and long-term care planning goals.

")