Death Benefit Design Options Using Section 7702 Carrier Products

At the time of writing this, 2021 is already half over and AgencyONE was seeing quite a few of our carrier partners introduce their compliant Section 7702 IUL options. From a design standpoint, our case design team has noticed that the initial face amounts generated are noticeably lower and the income is higher based on the 7702 changes. Some advisors have expressed concern that their clients are sacrificing too much death benefit for such a small increase in projected income. This week’s ONEIdea will discuss death benefit design options using Section 7702 products.

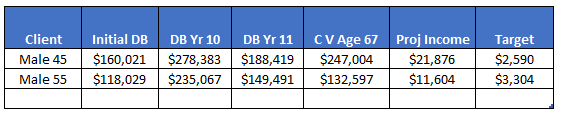

PROJECTED INCOME – TRUE MINIMUM NON MEC DESIGN

If projected income is the most important aspect of the sale, than a true minimum non mec design will provide the highest possible income for your client (Click here for a FAQ and explanation of MEC). This design requires leveling and dropping the death benefit at the end of the premium payment period to further maximize the design. Let’s consider two different ages since these comparisons perform differently based on age. Assume the following:

- Male 45 and Male 55, both preferred non-tobacco

- $10,000 premium for 10 years; then a maximum death benefit drop in year 11

- Income from ages 68 – 85 using withdrawals to standard loans

- Maximum carrier AG49 rate

The table below shows a true minimum non mec design illustrated today:

The information set forth in the table above does not allow any extra room for additional funding and also does not provide much death benefit, if needed. Many of our AgencyONE 100 advisors prefer to have additional cushion built into the death benefit so that their clients can increase premiums down the road. While they do not keep a policy optimally funded, the new product versions offer clients the option to increase future premiums.

DOUBLE MINIMUM NON MEC FACE AND MAINTAIN PREMIUM

Another scenario to consider is to keep the premiums the same but double the previous minimum non mec face to see what that looks like. The table below explores this option:

TWO SCENARIOS – DIFFERENCES

The main differences between the two comparisons above are that the face amounts are higher for 10 years in one scenario but then drop quite a bit after the reduction to the corridor limits in year 11. Cash values are lower which cause the income to also decrease. Target is 2X the minimum non mec amount. Even though the design builds in premium and allows room for the client to increase the funding later, it drags down the values. There is too much death benefit for the premium paid and, if the client does not increase the funding of the policy, it will impact the policy’s future values in a negative way.

A BALANCED OPTION

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

RESULTS OF A BALANCED OPTION

This balanced option provides more initial death benefit and only slightly impacts the cash values and income. The percentage drops are within a more acceptable range and allow the clients to increase contributions down the road as their income levels increase. This design gives the client more options without impacting the cash value and income – as much as the doubling of the face amount scenario. Is the small decrease in values worth the extra death benefit trade off? Only you and your client can decide that.

AgencyONE’s Case Design Department is very well-versed in carrier product intelligence, has an exceptionally high degree of case design experience, and stands ready to assist our AgencyONE 100 Advisors and their clients in considering the best death benefit design options using Section 7702 products.