Executive Bonus Plans for Key Executives

The retention of employees has been on the minds of many lately – including advisors and their business owner clients. Business owners are more concerned than ever in retaining and rewarding their key employees and executives in order to maintain their businesses and manage them efficiently. At AgencyONE, we’ve received numerous 4th quarter requests from our AgencyONE 100 Advisors that suggest this “concern” is factoring into the financial planning for many businesses.

One longtime employee retention plan is called a Section 162 bonus plan. When was the last time you used one of these for a client? AgencyONE has quoted these periodically over the last year, but I recently was surprised by a similar request from two different advisors who were interested in using this to help their corporate clients. We even went a few steps further and presented a Double Bonus Funding Pattern with a Restrictive Endorsement.

A 162 Bonus Plan aka Executive Bonus Plan

A 162 Bonus Plan aka Executive Bonus Plan

What is a Section 162 Bonus Plan or an Executive Bonus Plan? This is a plan put in place by an employer that is essentially a “raise in pay” that usually involves the purchase of a life insurance contract on the life of an employer’s selected key executive. The employer pays the premiums on the policy in the form of the bonus and can deduct that amount as a business deduction for ordinary and necessary business expenses under Section 162(a)(1) of the Internal Revenue Code of 2001. Total compensation, including bonus, must stay within the bounds of reasonable compensation.

How an Executive Bonus Plan Works

The following is a basic structure for an Executive Bonus Plan:

- The insurance policy is owned from the outset by the executive. The executive names their beneficiary and has all rights of ownership in the contract.

- The employer pays the bonus in the form of premiums sent directly to the insurer.

- The entire premium paid is by the employer under an executive bonus arrangement and is charged to the executive as ordinary compensation income and reported on their IRS Form W-2. Each bonus is subject to FICA and FUTA tax. The bonused premiums are considered a non-cash, fringe benefit for withholding purposes, so the premiums will be added to regular cash wages paid during the year and the appropriate withholding adjustment will be made. In many cases, the employer will assist the executive even further by paying an amount sufficient to pay both the premiums and the tax on the bonus. This is often called either a “double bonus” or “grossing up.” (The arrangement is generally not recommended for S Corporation owners or partners since those businesses are not separate taxpaying entities.)

A Sample Case

Let’s review one of the recent cases I mentioned above. The owner of a small company has been concerned with employee retention. All of the press regarding the “Great Resignation” has been worrying and he wanted to make sure that two of his most key executives were incentivized to stay with the company (male executive age 38 and female executive age 42). The owner was willing to bonus each employee $10,000 per year for 15 years and also wanted to “gross up” the bonus to cover the taxes due. Assuming the executives were in a 35% tax bracket, that would result in a total bonus of $15,385 per year.

Let’s review one of the recent cases I mentioned above. The owner of a small company has been concerned with employee retention. All of the press regarding the “Great Resignation” has been worrying and he wanted to make sure that two of his most key executives were incentivized to stay with the company (male executive age 38 and female executive age 42). The owner was willing to bonus each employee $10,000 per year for 15 years and also wanted to “gross up” the bonus to cover the taxes due. Assuming the executives were in a 35% tax bracket, that would result in a total bonus of $15,385 per year.

Restrictive Endorsement Bonus Agreement (REBA)

To provide the retention incentive that the employer wanted, the AgencyONE 100 Advisor recommended the addition of a Restrictive Endorsement to the bonus arrangement. A Restrictive Endorsement is created between the employer and the key executive. This agreement requires the employer’s consent for the executive to have access to the policy values, which provides enticement for the executive to remain employed for a specific length of time. The agreement may also stipulate a vesting and repayment schedule in the event the executive does not fulfill the employment time frame set forth in the agreement. AgencyONE’s plan was designed to allow the executive 10% access to the cash value in year one and this will increase by 10% each year through year 10. In year 10 the Executive will be fully vested in the plan and will have 100% access to the cash value. Our carrier partner on this case has the administrative processes in place to help implement and monitor the terms of the Restrictive Endorsement.

arrangement. A Restrictive Endorsement is created between the employer and the key executive. This agreement requires the employer’s consent for the executive to have access to the policy values, which provides enticement for the executive to remain employed for a specific length of time. The agreement may also stipulate a vesting and repayment schedule in the event the executive does not fulfill the employment time frame set forth in the agreement. AgencyONE’s plan was designed to allow the executive 10% access to the cash value in year one and this will increase by 10% each year through year 10. In year 10 the Executive will be fully vested in the plan and will have 100% access to the cash value. Our carrier partner on this case has the administrative processes in place to help implement and monitor the terms of the Restrictive Endorsement.

Key Executive Benefits Under the Plan

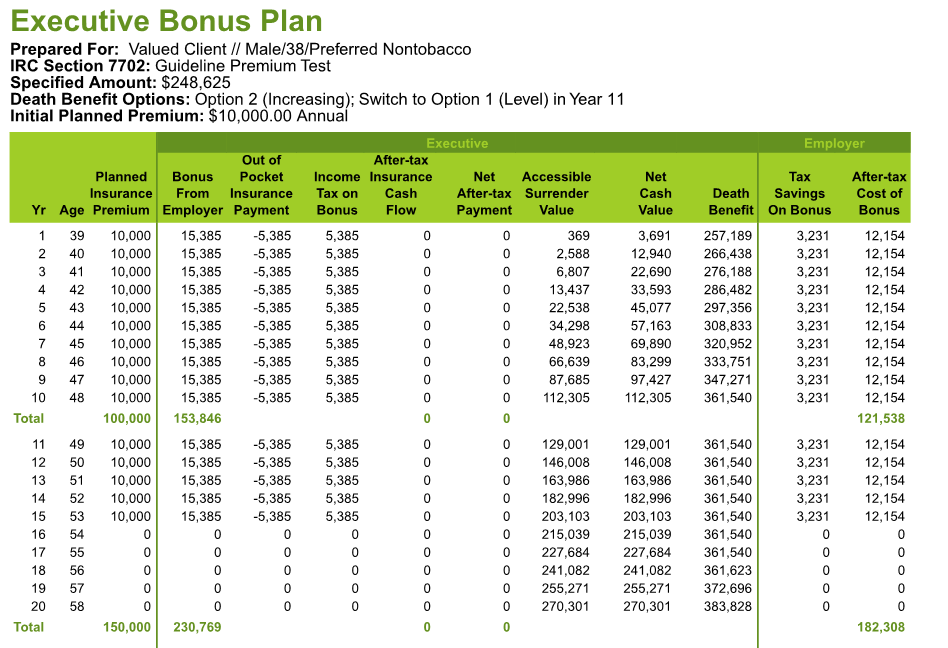

Let’s explore what the key executive receives under this arrangement. We will focus on the younger client’s projected values (male executive age 38).

As you can see in the first few columns to the left under “Executive”, the employer bonuses a total of $15,385 per year with $10,000 of that going to the policy premium. The remainder of $5,385 per year goes to the executive to pay the required taxes. Then looking further right under the “Executive” section you can see the illustrated Net Cash Values and the key executive’s accessible cash values (Accessible Surrender Value). Finally, the last two columns on the right show the Employer’s Tax Savings on the Bonus and After-tax Cost of Bonus. After 10 years, the executive (insured) has 100% access to the cash values (the specified length of time in the Restrictive Endorsement), and in our design, the employer makes 5 more payments to the plan. Assuming a 5.75% crediting rate, this projects an income stream of $50,484 per year to the key executive from ages 71-85. Of course, the key executive can access the money any way he chooses AFTER the Restrictive Endorsement expires.

Highlights of an Executive Bonus Plan

For the Employee:

- The policy funding the plan is owned by the executive

- The plan can be designed to meet personal needs

- The executive’s tax cost can be covered by an additional bonus from the employer

- Any growth in policy cash values accumulate tax deferred

- Tax preferred income can be received from the plan via withdrawals and loans

- The executive has some control over the plan, including beneficiary selection and asset allocation

For the Employer:

- Bonuses are tax-deductible

- The employer has complete discretion in selecting who is included

- There are no maximum or minimum contribution requirements

- No IRS approval required

- Minimal administration expense

- Plan may be terminated at any time pursuant to the agreement

- Plan design is simple

- Using a Restricted Endorsement Bonus Arrangement (REBA) can create “golden handcuffs”

Underwriting for this Solution

The executive will need to be fully underwritten for use of this solution. Since the face amount on this case is below $1,000,000 and the key executive is younger, he can apply through Accelerated Underwriting (AUW) which could result in a quick turn-around assuming he qualifies. The details of this case tend to be right in the “sweet spot” for AUW solutions which are run with a minimum non mec death benefit to maximize the cash value over time. You can find an up-to-date Accelerated Underwriting spreadsheet on your personal AgencyONE Advisor Dashboard in the Underwriting dropdown tab. The sheet outlines all of our carrier partners’ AUW programs. Please note that you will need to be authorized to use our website to access this tool.

Accelerated Underwriting (AUW) which could result in a quick turn-around assuming he qualifies. The details of this case tend to be right in the “sweet spot” for AUW solutions which are run with a minimum non mec death benefit to maximize the cash value over time. You can find an up-to-date Accelerated Underwriting spreadsheet on your personal AgencyONE Advisor Dashboard in the Underwriting dropdown tab. The sheet outlines all of our carrier partners’ AUW programs. Please note that you will need to be authorized to use our website to access this tool.

More business owners and employers are looking to retain key executives during this “Great Resignation” job market. An Executive Bonus Plan arrangement is a creative way to help incentivize these executives. The additional compensation paid into the policy, the opportunity to eventually receive vested policy cash values, and the beneficiary death benefit may encourage key executives to remain employed longer.

AgencyONE has the experience and knowledge to assist in the planning, underwriting, and placing of insurance solutions to fit any of your clients personal or business needs.