")

Planning Opportunities & How Collaboration Can Increase Your Sales

As an Advanced Planning and Case Design resource to many wealth management professionals, I am often asked “what’s hot in the area of products or sales ideas?” I have never said this to anyone before, but …. I LOATHE that question!

I have been doing this long enough to know that various products and design ideas have been hot over the years at various times for various reasons. A lot of these “hot” ideas and concepts are no longer around thanks to perceived abuses and action taken by Congress or the IRS. Plans that were “designed to sell life insurance” such as 419 and 412i Plans and Captive Insurance Companies were killed by the IRS. Consider, as well, the product migration that took place from decade to decade such as Whole Life (70s), Universal Life (80s), Variable Universal Life (90s), Index Universal Life (00s) …. you get the point. As I mentioned, I have been around for a while and have seen many of these products cycle in and out of favor.

I have been doing this long enough to know that various products and design ideas have been hot over the years at various times for various reasons. A lot of these “hot” ideas and concepts are no longer around thanks to perceived abuses and action taken by Congress or the IRS. Plans that were “designed to sell life insurance” such as 419 and 412i Plans and Captive Insurance Companies were killed by the IRS. Consider, as well, the product migration that took place from decade to decade such as Whole Life (70s), Universal Life (80s), Variable Universal Life (90s), Index Universal Life (00s) …. you get the point. As I mentioned, I have been around for a while and have seen many of these products cycle in and out of favor.

Why do some advisors chase the latest product or concept? Wouldn’t it make more sense to ask the consumer/the client what they want and/or need and what is important to them? I believe that the answer is “Yes”, but statistics show that while most consumers are clear on what they think they want, when it comes to mortality, morbidity, longevity, and tax planning they:

1. Do not know how to achieve what they want;

2. Are confused and need help in gaining clarity or;

3. Are unaware of the issues and need to be educated.

While every advisor should consider what is currently available in the market, which may include “hot” or the latest products and concepts (it is the advisor’s fiduciary duty to consider everything), we should not be solely focused on the latest planning and/or design trend. As financial advisors, we need to help our clients determine what is IMPORTANT to them. To do this, we need to gain clarity by asking pertinent questions in order to make the right planning recommendations.

While every advisor should consider what is currently available in the market, which may include “hot” or the latest products and concepts (it is the advisor’s fiduciary duty to consider everything), we should not be solely focused on the latest planning and/or design trend. As financial advisors, we need to help our clients determine what is IMPORTANT to them. To do this, we need to gain clarity by asking pertinent questions in order to make the right planning recommendations.

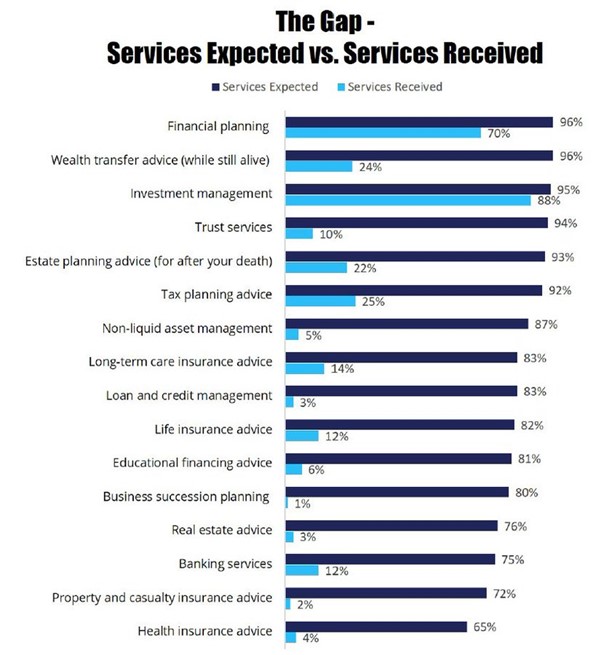

![]() One thing is very clear to me, and I have written about this before. Consumer expectations for financial services are NOT being delivered, specifically in the following areas where we are presumably experts:

One thing is very clear to me, and I have written about this before. Consumer expectations for financial services are NOT being delivered, specifically in the following areas where we are presumably experts:

1. Estate planning advice (for after your death);

2. Long-term care insurance advice;

3. Life insurance advice;

4. Business succession planning;

5. Property and casualty insurance advice; and

6. Health insurance advice.

As Advisors, we are in a unique position to provide these services but as seen in the chart below, which references a recent study conducted by the Spectrem Group, we are woefully under-accomplished.

There are basic demographic trends that support the economic principle of supply and demand. I will not bore you with the statistics about the 10,000 Baby Boomers retiring every day and the fact that they remained the largest living adult population until 2019 – just shy of 70MM Boomers in the US according to the latest US Census Bureau count. Our aging population is also creating a MASSIVE economic shift in wealth transfer and people need financial advice and planning assistance.

Following are areas of demand in the marketplace that are not being fully met and might create opportunities for you as a financial advisor:

1. If Boomers are retiring at 10,000 per day, that is 3.65MM in a year. According to the US Bureau of Labor Statistics, in 2021 there were 330,300 financial advisors in the United States. That means that every financial advisor could get 11.05 retirees as clients each year! Supply and demand.

1. If Boomers are retiring at 10,000 per day, that is 3.65MM in a year. According to the US Bureau of Labor Statistics, in 2021 there were 330,300 financial advisors in the United States. That means that every financial advisor could get 11.05 retirees as clients each year! Supply and demand.

2. The greatest wealth transfer in the history of humanity – TRILLIONS of dollars – is happening right now. Think of the opportunities to advise clients in wealth transfer planning. Shockingly, only 22% of financial advisors deliver this service to their clients, while 93% expect it!! Supply and demand.

3. An RIA Intel article includes statistics from Boston-based Cerulli Associates and says that over “111,500 advisors will retire” over the next 10 years – a number that represents more than “one-third of the workforce and assets”. Supply and demand.

4. Elder care services are needed as the population ages. According to many studies, approximately 70% of adults aged 65 or older will require long-term care at some point. The average length of stay in long term care is 3.2 years and over 20% of residents will require care for 5 years or longer. Referring back to point number 1 above, this means that 7,000 people each day may end up in long term care! Yet only 14% of advisors provide long term care advice while 83% of consumers expect it! Supply and demand.

5. Probably my favorite. There are millions of business owners who are looking to retire or pass on their business to family members or to key executives. COVID-19 accelerated the urge to do so, however many business owners cannot afford to retire or do not know how to sell and generate enough capital to support their retirement. There are over 33MM small businesses in the United States and only 1% of advisors provide business succession planning! Do you think there is an opportunity for you? Supply and demand.

The economic headlines are full of predictions of inflation, a US national debt crisis, increasing taxes, a pending recession, environmental disasters, new emerging viruses, and potential pandemics. I could go on and on. Your retiring clients – all 70MM of them – read these headlines and worry about their golden years. This transition offers a tremendous opportunity to be of service to your clients and their families AND to potentially expand your business.

There is a HUGE demand for what you do! While many advisors are not specialists in ALL areas of planning, they know when they are out of their depth. Think of the medical industry. An oncologist and a gynecologist are very different areas of expertise, but that does not mean that a gynecologist cannot diagnose cervical cancer and consult with the oncologist for the proper course of treatment. Often times they work together collaboratively for the benefit of the patient/client. Why should financial services be any different?

There is a HUGE demand for what you do! While many advisors are not specialists in ALL areas of planning, they know when they are out of their depth. Think of the medical industry. An oncologist and a gynecologist are very different areas of expertise, but that does not mean that a gynecologist cannot diagnose cervical cancer and consult with the oncologist for the proper course of treatment. Often times they work together collaboratively for the benefit of the patient/client. Why should financial services be any different?

In financial services, wealth management is a comprehensive term and reflecting on the Spectrem Study mentioned above, I believe that there may be a reason why only two of the areas of service listed are mostly being provided: Financial Planning and Investment Management.

I will put forth a theory which may get me in trouble with some readers. I think that many Financial Planners and Investment Managers substantially ignore the rest of the services that clients expect them to provide, because they do not have the expertise to deliver advice confidently or choose to ignore it all together.

I will put forth a theory which may get me in trouble with some readers. I think that many Financial Planners and Investment Managers substantially ignore the rest of the services that clients expect them to provide, because they do not have the expertise to deliver advice confidently or choose to ignore it all together.

Collaboration is critical to holistic wealth management, just as it is in the medical field for holistic health management. The DEMAND for our services as COLLABORATIVE TEAMS of professionals exists. Changes in our industry dictate that we seek collaborative relationships in order to properly serve our clients and help our businesses flourish. Attorneys, Accountants, Investment Managers, Financial Planners and Risk Managers all have the potential to contribute to the very important journey that 70MM people are either planning for or have embarked on.

At AgencyONE, we recognize the need and embrace the opportunity for collaboration among different disciplines in the planning industry. Collaborative planning leads to a more holistic and well-rounded financial plan for all our clients. With that in mind, AgencyONE has developed a collaborative training program – High Performance Collaborative Teams Training – that combines the concepts of True Wealth Mentorship and Empowered Wealth (as presented by Ron Nakamoto to our advisors over the past few years on behalf of AgencyONE) and collaborative financial planning. We have already hosted a number of these collaborative programs and gained overwhelmingly positive reviews.

At AgencyONE, we recognize the need and embrace the opportunity for collaboration among different disciplines in the planning industry. Collaborative planning leads to a more holistic and well-rounded financial plan for all our clients. With that in mind, AgencyONE has developed a collaborative training program – High Performance Collaborative Teams Training – that combines the concepts of True Wealth Mentorship and Empowered Wealth (as presented by Ron Nakamoto to our advisors over the past few years on behalf of AgencyONE) and collaborative financial planning. We have already hosted a number of these collaborative programs and gained overwhelmingly positive reviews.

The High-Performance Collaborative Teams Training program brings together insurance advisors and their invited Centers of Influence (COI) – the “planning pod” – for a full day of high-performance collaboration.

The centerpiece of the program is an Evolving Case Study that is presented to the attendees in sections over the course of the day. Each “planning pod” discusses their client recommendations from the perspective of their planning disciplines and the changing fact patterns of the case study. The ultimate goal is to create a financial plan that considers the expertise from each of the planning specialties and is customized to the unique needs of the client.

The High-Performance Collaborative Teams Training program is designed to be duplicated anywhere in the country for our AgencyONE 100 Advisors. If you work with COIs and would like to establish a closer relationship with these advisors and generate more referrals, we hope you will consider hosting a High-Performance Collaborative Teams Training program along with AgencyONE in your hometown. We are actively working with two more of our AgencyONE 100 advisors to host a High-Performance Collaborative Teams Training program this summer in their hometowns.

establish a closer relationship with these advisors and generate more referrals, we hope you will consider hosting a High-Performance Collaborative Teams Training program along with AgencyONE in your hometown. We are actively working with two more of our AgencyONE 100 advisors to host a High-Performance Collaborative Teams Training program this summer in their hometowns.

We would be happy to share additional information and the roadmap we have created to host this successful program.

Please contact the AgencyONE Marketing Department at 301.803.7500 for more information or to discuss a case.