How to Design an Efficient Life Insurance Contract Under the Section 7702

Section 205 of the Consolidated Appropriations Act, 2021 (H.R. 133) signed by President Trump on December 27th, 2020 made changes to Internal Revenue Code Section 7702 providing for the use of a more dynamic interest rate methodology when calculating the “Definition of Life Insurance” (or DOLI) that dates to the 1984 Deficit Reduction Act, also known as DEFRA, where Section 7702 was first introduced. The new methodology will allow changes over time in line with market interest rates, versus the traditional fixed rate that was established in a very high interest rate environment.

Section 7702 Defined

A discussion of U.S. Code Section 7702 where “the definition of life insurance” is described can be found in a variety of places, including the Internal Revenue Code, but I have provided the following (more simple, if that is even possible) information from Cornell Law School’s Legal Information Institute. A full discussion of Section 7702 goes beyond the purpose of this article, but the aforementioned link provides a suitable framework to understand where this is going.

Simply stated, Section 7702 was enacted under DEFRA in response to the abuses created by single premium life insurance contracts (a tax shelter\haven) in the early 1980s thereby limiting the funding pattern of life insurance, discouraging single premiums, and discouraging further abuses. This was also around the time when Universal Life was just coming to market with illustrated rates in excess of 10%. I started in the insurance industry in 1982 and remember these “glory” days, I am sure many of you do as well.

As interest rates have steadily decreased for 35 plus years, since 1984, the funding limitations for life insurance (the maximum allowable premiums as defined under Section 7702) were limited by either a 4% or 6% interest rate test depending on which methodology was chosen. These rates were fixed in the codification of Section 7702 and hence artificially high in today’s interest rate environment.

While H.R. 133 was really intended to solve some very significant challenges that Whole Life was experiencing due to the current interest rate environment, it may also present some unintended consequences for Universal Life that the law did not anticipate. As a result of H.R. 133, the maximum Guideline Premiums under DEFRA and, by consequence, the maximum non-MEC (Modified Endowment Contract) premiums introduced subsequently by TAMRA in 1987, are going up substantially, potentially doubling at certain ages.

Designing an Efficient Contract Within the Tax Code

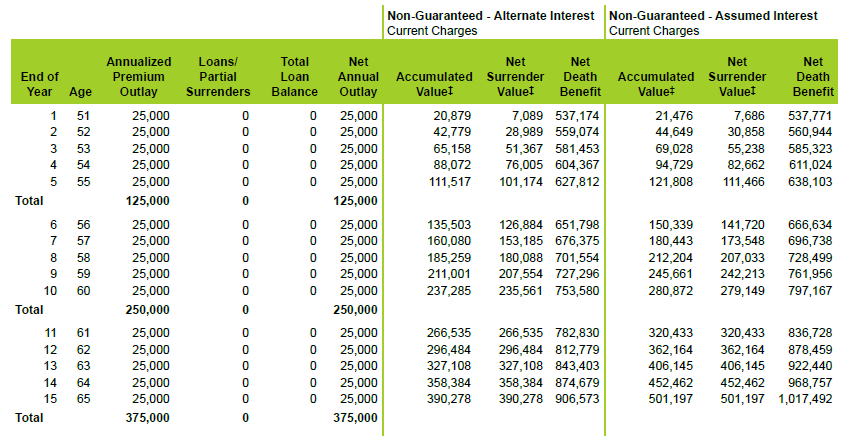

Now to the actual subject matter of this article because this is where things really get interesting. By way of example, let us use a 50-year-old male, Preferred Non-Tobacco class, in a supplemental retirement accumulation scenario. The goal of this proposal design is to make the life insurance contract as efficient as possible without violating the tax code, meaning, contributing the maximum premium allowable under DEFRA and TAMRA, as previously afforded under the law, for the minimum death benefit.

In this case you will see the following:

- An initial premium contribution of $25,000 per year for 15 years (to the client’s age 65)

- An initial minimum non-modified endowment death benefit of $516,295

- An increasing death benefit option during the premium payment period (death benefit PLUS accumulation account)

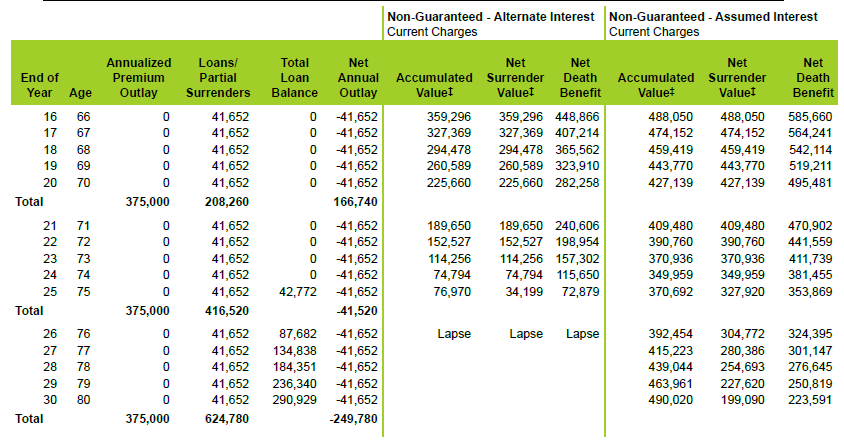

- When premiums cease (age 65), a lowering AND leveling of the death benefit option to maintain the DEFRA and TAMRA compliance corridor

- Tax-free withdrawals to basis starting at age 66 and tax-free loans after the basis has been withdrawn for the balance of 20 years (to age 85)

Pre-Retirement (funding period)

Post-Retirement (distribution period)

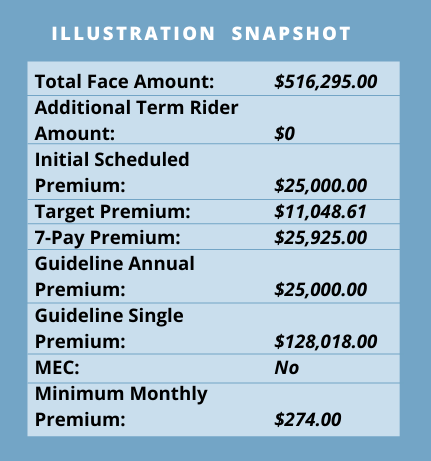

A snapshot of the various premium limits is seen to the left. As you can see, the $25,000 scheduled premium meets the Guideline Annual Premium and is below the 7-Pay (Non-MEC) Premium by a small amount, maintaining Non-MEC status. The target premium is also listed as $11,048.61.

A snapshot of the various premium limits is seen to the left. As you can see, the $25,000 scheduled premium meets the Guideline Annual Premium and is below the 7-Pay (Non-MEC) Premium by a small amount, maintaining Non-MEC status. The target premium is also listed as $11,048.61.

For those of you that are not familiar with the concept of a target premium, it is the premium for which the writing agent is compensated on at the first-year rate and anything over that ($25,000 minus $11,048.61) is compensated at the “excess rate”, which is a fraction of the first-year rate.

If we go back to what was said earlier about the Guideline Premium essentially doubling, under the new rules a client would be able to contribute $50,000 to this same policy with a $516,295 death benefit.

The target premium is a per thousand rate that is face amount driven. If you do that math, then you will conclude, as I have, that while doubling the premium contribution on the part of the client, the target premium would stay the same. The impact of this is that there is a LOT more excess premium with no expense\load for first year commission.

NOT doubling (or increasing) the target commissionable premium would have the impact of:

- Making the contract much more efficient and benefitting the client from an accumulation standpoint, AND

- Reducing the compensation to the agent per dollar of actual premium collected on the sale by half (approximately).

The question is …. will the carriers, when they start re-designing their products to comply with H.R. 133, double (or increase) the target premium or will they expect insurance agents to receive half of their previous compensation for the “same sale”?

Increased Insurance Sales Under Section 7702?

If the insurance community expects that the tax-deferred efficiency of life insurance along with lower-loads on premiums will lead to more sales of life insurance, then it can make up the difference in more sales to tax savvy clients. If not, then the carriers will have to decide who wants to play the game of chicken by not increasing target premiums while other carriers do and risk that some advisors will not sell their product and pivot to the carrier that has a product with a more compelling target premium instead.

Let us be mindful that the industry has been under a lot of pressure from regulators and fee-based pundits that commission-based life insurance is a “bad investment as a retirement vehicle”. Before this 7702 change we know that was an erroneous allegation; post 7702, it will still be wrong, but just by a matter of degrees. How much will the industry put on the table to provide a much more cost-efficient product for consumers and hopefully gain more customers? Or will the “new insurance advisor” be more wealth management driven as is the fee-based\ fiduciary advisor community?

It is up to the insurance company executives and actuaries to figure out how this will play out. Will the solution be “on target”?

Again, please join AgencyONE tomorrow (January 28, 2020), at 4:00 p.m. EST for a complete discussion about the changes to IRC Section 7702 and how these changes are likely to impact your sales practices.