The Problem with Cross-Purchase Buy-Sell Agreements & a Unique Solution

Have you ever had business owner partners or shareholders who varied in age and health? Have these business partners or shareholders ever asked you to explain why, for the same amount of insurance to fund their buy-sell agreement, the premium was so dramatically different? It happens all the time. If you have never heard of a Cross Endorsement Buy-Sell Arrangement (CEBS), read on because it presents an incredibly elegant solution for this otherwise inequitable situation.

The Cross-Purchase Buy-Sell Scenario

Imagine a male, non-tobacco user, business owner who is 55-years-old and his 40-year-old female partner, also a non-tobacco user. They are both in excellent health. They are 50% partners in a successful $10MM business and, at the recommendation of their attorney, have asked you to quote life insurance to fund their Cross-Purchase Buy-Sell Agreement. You quote $5MM of 10-year term at Preferred Best rates as follows:

Imagine a male, non-tobacco user, business owner who is 55-years-old and his 40-year-old female partner, also a non-tobacco user. They are both in excellent health. They are 50% partners in a successful $10MM business and, at the recommendation of their attorney, have asked you to quote life insurance to fund their Cross-Purchase Buy-Sell Agreement. You quote $5MM of 10-year term at Preferred Best rates as follows:

- Male, 55, Pref Best NT = $6,381 per year

Female, 40, Pref Best NT = $1,123 per year

The younger female partner asks why she must pay so much more premium out of HER pocket to pay for the insurance on her partner – almost 6 times more; she does not see it as equitable to their partnership. But the story does not end there.

After underwriting the case, it is discovered that the male partner is not in very good health and the underwriting is negotiated at Standard NT. The premium is now $13,800 and the female partner is REALLY not happy. They need the insurance to fund the buy-sell agreement for their successful business. The female partner is now faced with the reality that her business partner’s health is fragile, but she wants a more equitable funding arrangement.

(If the male 55 owner were Table 2, the premium would be over $20,000, if Table 4, over $28,000 and if a standard nicotine user, over $40,000. The inequity can grow very quickly and exponentially!)

What is a Cross Endorsement Buy-Sell Arrangement

The Cross Endorsement Buy-Sell Arrangement requires the use of permanent insurance. In full disclosure, additional cash flow will be required, but the partners, especially the younger partner, will benefit greatly from this solution in the form of cash value growth. Let’s unpack this.

The typical cross-purchase agreements is most often used to benefit the surviving partner with a step-up in basis of the re-purchased shares after the death of a partner. This contrasts with a stock redemption buy-sell agreement where the business owns the insurance and redeems the stock of a deceased shareholder. However, a cross-purchase agreement presents several problems, including:

- If a partner retires or leaves the business, the remaining partner will own the policy on his or her life;

- If a partner dies while owning a policy on the other partner’s life, then the ownership of the surviving partner’s insurance ends up in the hands of the deceased partner’s spouse, children, or estate; and

If a partner’s health deteriorates and the insurance is critical to personal financial objectives, the policy is owned by, and the beneficiary is, the other partner.

How a Cross Endorsement Buy-Sell Arrangement Works

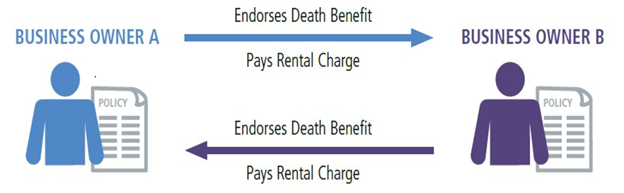

The Cross Endorsement Buy-Sell Arrangement is unique in that it allows each partner to own the needed insurance on their own life and always retain complete control of the policy. However, under the agreement, the owner of the policy endorses or “rents out” a portion of the face amount of the policy sufficient to meet the buy-sell obligation to the other partner\shareholder. See diagram below:

The rental charge/ premium is based on the economic benefit cost as measured either by the government or the insurance company rate table. This table is an increasing annual amount and is completely agnostic to:

- sex (it is a unisex table)

- nicotine usage\smoking habits

- health rating class

With a Cross Endorsement Buy-Sell Arrangement, the premiums for each of the partners will be simply based on the difference in age – a far more equitable solution that does not penalize an otherwise perfectly healthy woman.

The Nitty-Gritty of a Cross Endorsement Buy-Sell Arrangement

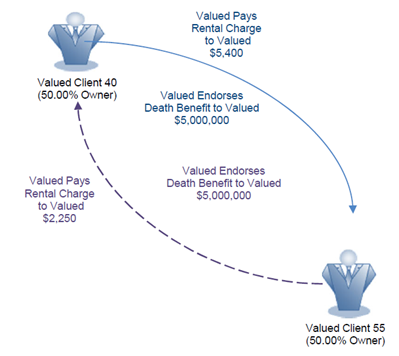

In the first year of a Cross Endorsement Buy-Sell Arrangement, the premium differential is just less than double (purely age based) as can be seen in the diagram below:

Each business owner purchases, owns, and pays the premium and names the beneficiary of their own permanent life insurance policy.

Each business owner purchases, owns, and pays the premium and names the beneficiary of their own permanent life insurance policy.

They immediately endorse the needed portion of the face amount/death benefit that is required to meet the agreed upon amount of their buy-sell agreement over to the other partner.

This amount can be modified on a year-by-year basis should equity ownership in the business change, including the addition of partners.

Depending on the funding desire, ability, or commitment of each individual owner, the cash value will grow accordingly. That is a personal decision as to how each partner wants to fund their own policy. It can vary greatly, depending on the product chosen, and range from the minimum guaranteed premium to the maximum non-MEC (Modified Endowment Contract) premium.

The Cross Endorsement Buy-Sell Arrangement Scenario

As an example, the 55-year-old male owner could fund his policy up to the maximum amount of $442,965 each year for 7 years. This would be offset by the “rental income” from the other partner each year, and result in a very meaningful cash value growth at age 65, 67 or age 70. Lower premiums could also be paid depending on the objectives and cash flow of the client.

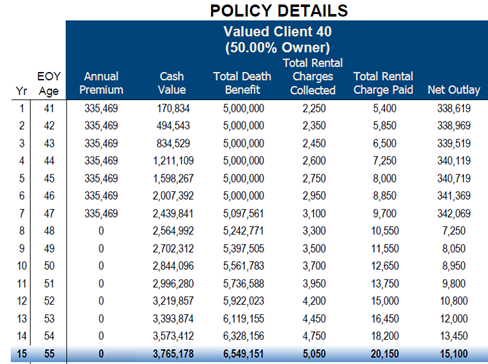

Similarly, the 40-year-old female owner could fund her policy up to the maximum of $335,469 annually for 7 years, which would again be offset by the “rental income” from the other partner.

Another important benefit of a younger partner setting aside funds in this manner is that it provides for liquid cash to help her fund a lifetime buy-out of her partner should he decide to retire or sell a portion of his shares to her. For example, as seen in the adjacent table, the female partner’s cash value growth using an Index Universal Life product for illustration purposes, would be $3,765MM in year 15, her partner’s age 70.

Another important benefit of a younger partner setting aside funds in this manner is that it provides for liquid cash to help her fund a lifetime buy-out of her partner should he decide to retire or sell a portion of his shares to her. For example, as seen in the adjacent table, the female partner’s cash value growth using an Index Universal Life product for illustration purposes, would be $3,765MM in year 15, her partner’s age 70.

Each partner also has the ability to terminate the endorsement as needed and enjoy the cash value as part of a tax-free income stream during retirement.

|

|

|

")

")

")