A Premium Finance Insurance Case That Went Well!

I typically see Premium Finance cases in the concept stage and probably see about 3-4 of these cases per week. A lot of advisors would like to offer Premium Finance to their high-net-worth clients who need insurance, but not every case makes the cut. In this week’s ONEIdea we discuss a Premium Finance insurance case – with options – that went well!

THE PREMIUM FINANCED CONTRACT

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the linked blog post from Gonzalo Garcia, CLU). Others are actual Premium Finance cases that have been discussed in detail with the advisor and client who like the strategy of using leverage to obtain the required financial and insurance goals.

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the linked blog post from Gonzalo Garcia, CLU). Others are actual Premium Finance cases that have been discussed in detail with the advisor and client who like the strategy of using leverage to obtain the required financial and insurance goals.

THE ATTRACTION OF A PREMIUM FINANCE CASE

Advisors continue to show Premium Finance cases because they are typically LARGE, and they appeal to high-net-worth clients who like the idea of borrowing funds to pay for the life insurance rather than liquidating existing investments. The majority of the cases we see at AgencyONE request a design where the client:

- pays as little as possible;

- posts NO collateral;

- pays minimal interest; and

- pays off the loan using the value in the policy.

ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

One reason is that the typical criteria for the sale is NOT REALISTIC! It is best for clients to have some “skin in the game” and to be prepared to pay interest annually and post the needed collateral AT A MINIMUM. The more the client contributes to a Premium Finance case the more likely the policy will perform as designed and remain viable to help the client “weather” any down years that might impact the contract. Benefits of the client financially contributing to a Premium Finance deal are:

- flexibility on borrowing amounts;

- flexibility on years to borrow;

- ability to exit the loan earlier and more efficiently; and

- less risk to the policy over time.

ILLUSTRATING PREMIUM FINANCE DESIGNS UNDER AG49A

Limits are set on the allowable max index rates and also for par loans. When par loans are used the crediting rate of the policy is restricted to 50 basis points higher than the par loan rate. Example – a 5% par loan restricts the crediting rate of the illustration to 5.5%. Real performance is not affected, but these AG49A restrictions are an issue for some advisors since we are not permitted to show anything above the established illustration parameters.

A PREMIUM FINANCE INSURANCE CASE (with options) THAT WENT WELL

Recently, an AgencyONE 100 advisor presented a 52-year-old male client who was heavily invested in real estate and needed about $5,000,000 in life insurance coverage. The client had plenty of net worth but not much available cash for paying the insurance premiums. The client was in a position to pay the interest but was concerned about how he could exit the loan efficiently. The original request from the agent was to use a participating policy loan to pay off the bank loan. I explained that this design just MOVES the loan from the bank to the life insurance policy. The burden of the loan still exists but is shifted elsewhere. I then explained the risks of leaving the loan inside the policy. The contract would have to continue to perform and maintain positive cash value for the life of the insured to make this plan work. If the policy were to lapse, a huge taxable event would occur for the policy owner. The advisor and client were not comfortable with this possibility, so we continued to discuss the case and other available options.

PREMIUM FINANCE ALTERNATIVE OPTION #1

Discussions between the advisor and client revealed that the client had been considering selling some of his real estate rental properties in the next 10 -15 years. Could he use the sale proceeds to pay off the bank loan? This plan would leave the client with a cash-rich life insurance policy that could generate tax free income down the road. On the other hand, If the real estate sale proceeds were deposited into a brokerage account (instead of an IUL life policy) the growth would be taxable – an unacceptable and avoidable option.

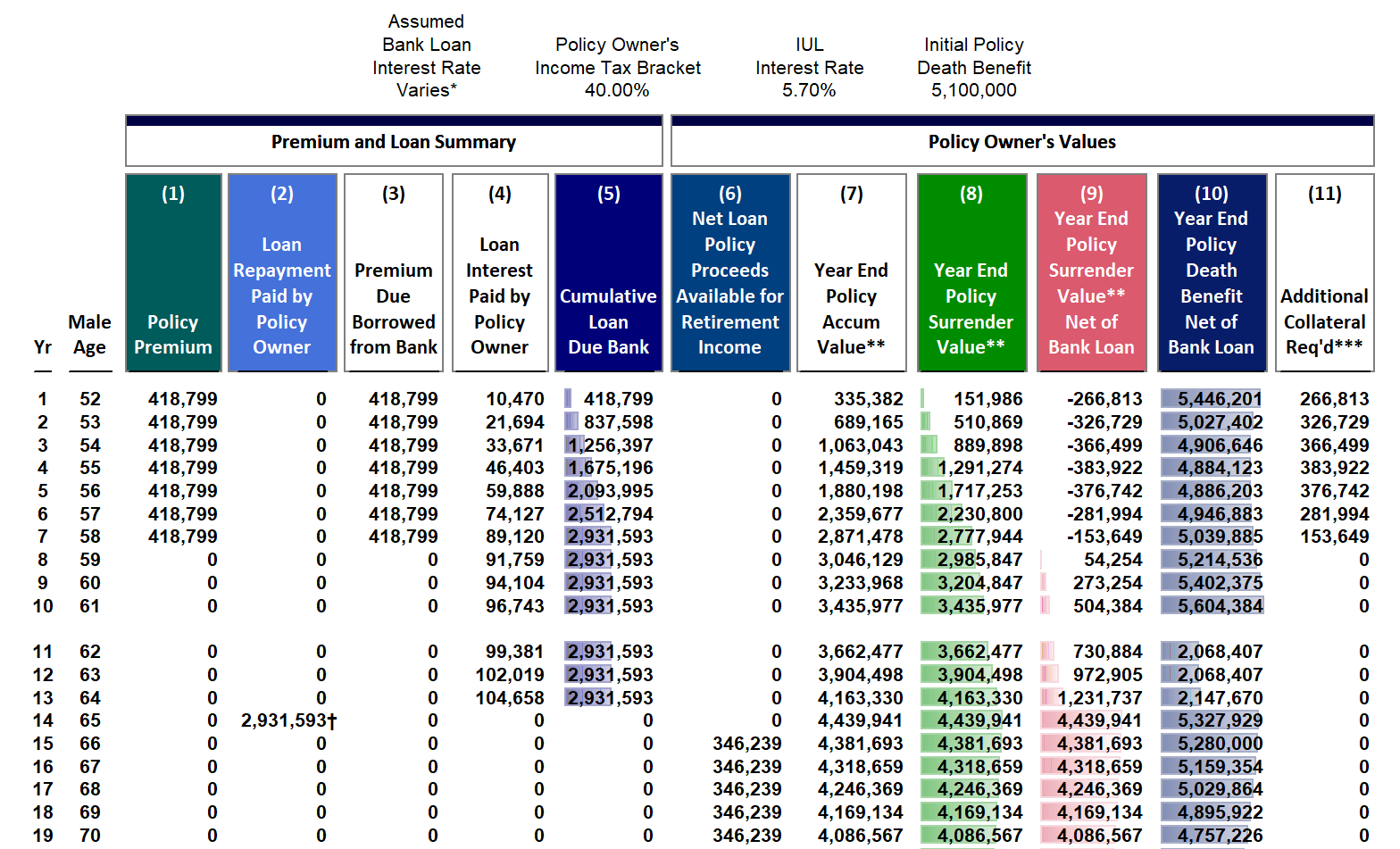

AgencyONE uses Insmark to illustrate Premium Finance cases. The Insmark illustration below shows the client borrowing an annual premium of $418,799 per year for 7 years. Since the client was not using the policy value to pay off the loan, he was able to borrow LESS. The client pays all the interest along the way AND pays the loan off by selling a portion of his rental property. He can then take withdrawals to basis/standard loans from the policy of approximately $346,239 per year for the years 15 to 38 –

The finance sheet above has quite a bit of useful information: premiums borrowed, projected interest payments due, cumulative loan, policy values, and additional collateral required in the right-hand column. The advisor and client were amenable to paying interest but were unsure about the additional collateral required (column 11). To address this concern, AgencyONE presented another option for the client to consider.

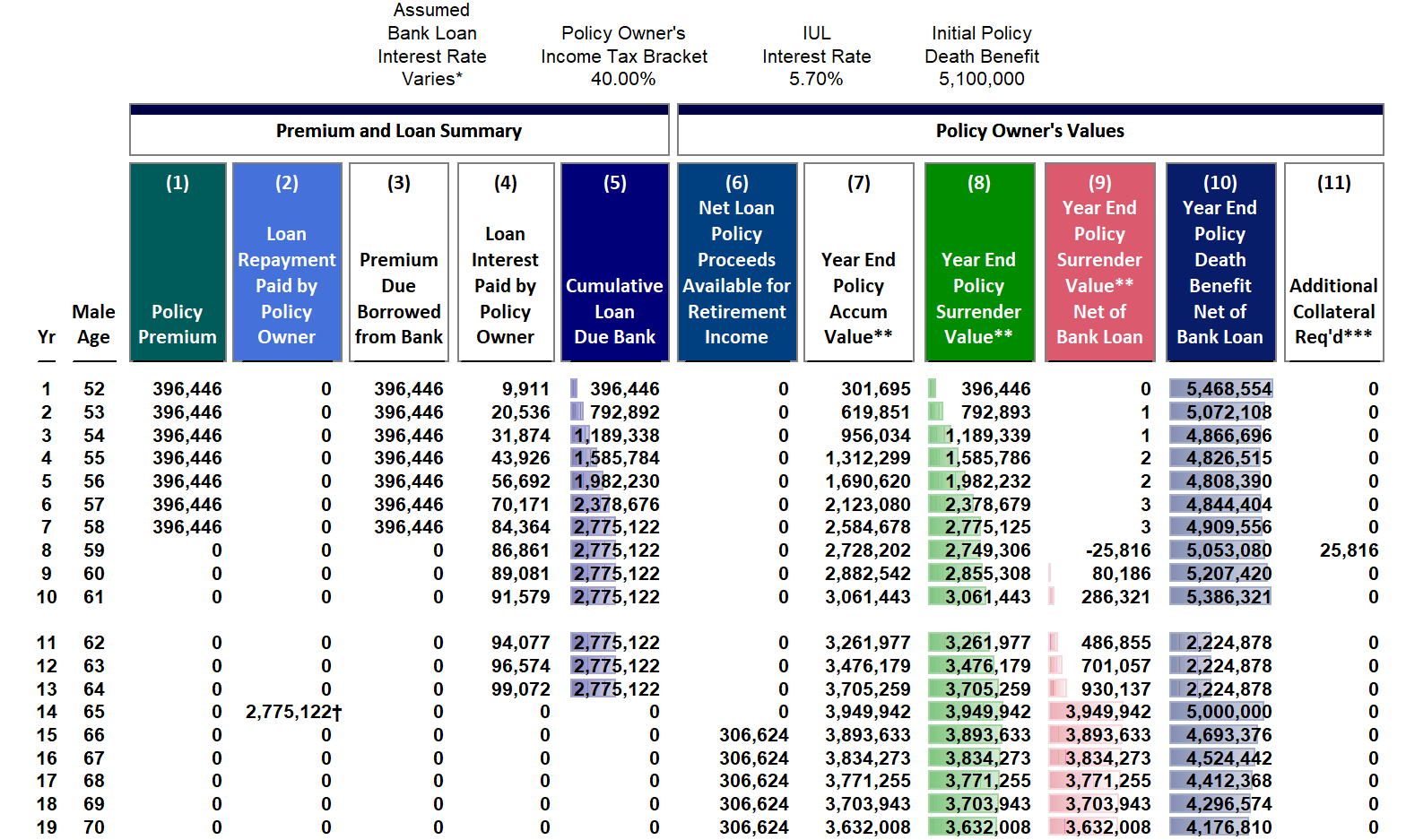

PREMIUM FINANCE ALTERNATIVE OPTION #2

In this scenario, we added an Early Cash Value (ECV) rider to the contract that would OFFSET the collateral requirement the client was required to pay (except for a small projected amount in year 8). The addition of the ECV rider:

- LOWERED the borrowed amount;

- impacted advisor compensation by spreading comp over 4 years;

- added a chargeback provision; and

- also reduced the projected income to the client by $39,615 per year.

The ECV rider will, however, provide the full 100% Cash Surrender Value (CSV) to offset the collateral through year 7.

BUT, is adding the ECV rider to avoid posting collateral worth losing a projected $950,760 of income over the time period illustrated, years 15 to 38? This depends upon client preference and requires detailed discussions between the advisor and the client. The AgencyONE 100 advisor presented both options to the client for review.

AgencyONE’s Advanced Markets and Case Design Team possess the knowledge and expertise to assist with all of your Premium Finance cases. We are available to talk concept, design, and implementation, AND we have strategic relationships with funders, such as US Bank, who can assist with lending on your cases.

Please contact AgencyONE’s Case Design Team at 301.803.7500 for more information or to discuss a case.

")