Annuities & Planning for Longevity

In addition to the many life challenges that your clients will face in retirement, their retirement plans may also be subject to market and financial risks. From a financial perspective, your clients will face market volatility, interest rate risk, withdrawal rate risk, sequence of return risk and longevity risk… just to name a few. The list of challenges that a retirement plan faces can seem daunting, but luckily you can help your clients insure against many of the challenges that they will face during a retirement that could last 30 years or more. In many cases, a Deferred Income Annuity (DIA) or a Fixed Index Annuity (FIA) with a lifetime income rider (LIR) [also known by catchy names like Guaranteed Minimum Withdrawal Benefit (GMWB) or Guaranteed Minimum Income Benefit- (GMIB)] may be an appropriate solution to hedge against longevity. This blog post addresses Annuities & planning for longevity.

will face market volatility, interest rate risk, withdrawal rate risk, sequence of return risk and longevity risk… just to name a few. The list of challenges that a retirement plan faces can seem daunting, but luckily you can help your clients insure against many of the challenges that they will face during a retirement that could last 30 years or more. In many cases, a Deferred Income Annuity (DIA) or a Fixed Index Annuity (FIA) with a lifetime income rider (LIR) [also known by catchy names like Guaranteed Minimum Withdrawal Benefit (GMWB) or Guaranteed Minimum Income Benefit- (GMIB)] may be an appropriate solution to hedge against longevity. This blog post addresses Annuities & planning for longevity.

While employer pensions are rare these days, your clients are likely attracted to the concept of a retirement income stream that is guaranteed and cannot be outlived. Employers may not offer such benefits, but you can help your clients set up their own future pensions.

How Do Annuities Work?

A Deferred Income Annuity (DIA) works similarly to the Single Premium Immediate Annuity (SPIA). The client purchases a policy with a lump sum, 1035 or qualified transfer which then generates a stream of income that lasts as long as the client is alive. A DIA differs in that, rather than providing an immediate income stream, the client chooses WHEN they want their payments to begin.

A Deferred Income Annuity (DIA) works similarly to the Single Premium Immediate Annuity (SPIA). The client purchases a policy with a lump sum, 1035 or qualified transfer which then generates a stream of income that lasts as long as the client is alive. A DIA differs in that, rather than providing an immediate income stream, the client chooses WHEN they want their payments to begin.

A Fixed Indexed Annuity (FIA) has a similar function to an Index Universal Life (IUL) policy. The client’s account value tracks one of many indices and is credited interest based on a cap or participation rate. Importantly, the client’s principal is protected from market downturns with a 0% floor. A Lifetime Income Rider (LIR) creates a second bucket of values in the policy that grows at a guaranteed crediting rate. At a time specified by the client, they can choose to activate the LIR and receive guaranteed payments for life. The payments are simply a withdrawal percentage (that increases with the client’s age) multiplied by the LIR amount which continues to grow during the deferral period. Once the distributions begin, the account value is reduced, but remains available for the client to access should they need. The LIR provides income for as long as the client is alive, even after the account value reaches $0.

on a cap or participation rate. Importantly, the client’s principal is protected from market downturns with a 0% floor. A Lifetime Income Rider (LIR) creates a second bucket of values in the policy that grows at a guaranteed crediting rate. At a time specified by the client, they can choose to activate the LIR and receive guaranteed payments for life. The payments are simply a withdrawal percentage (that increases with the client’s age) multiplied by the LIR amount which continues to grow during the deferral period. Once the distributions begin, the account value is reduced, but remains available for the client to access should they need. The LIR provides income for as long as the client is alive, even after the account value reaches $0.

The important similarity between both options described above is that both generate a guaranteed stream of income that the client CANNOT outlive. Furthermore, deferring the start of income, especially with younger clients, can generate more income for less premium.

Annuity Case Study:

Jennifer is a 60-year-old female who is at a point in her life where she needs to take her retirement planning more seriously. Recent market fluctuations have caught her attention. As her planned retirement nears, she and her advisor decide that now may be a good time to de-risk part of her portfolio and purchase a policy to create a guaranteed income stream for life. She has several relatives that have lived well into their 90s and is quite concerned about the possibility of outliving her money – especially after learning that someone her age has a 1 in 5 chance of living to 93 and a 1 in 10 chance of living to age 96!

Jennifer is a 60-year-old female who is at a point in her life where she needs to take her retirement planning more seriously. Recent market fluctuations have caught her attention. As her planned retirement nears, she and her advisor decide that now may be a good time to de-risk part of her portfolio and purchase a policy to create a guaranteed income stream for life. She has several relatives that have lived well into their 90s and is quite concerned about the possibility of outliving her money – especially after learning that someone her age has a 1 in 5 chance of living to 93 and a 1 in 10 chance of living to age 96!

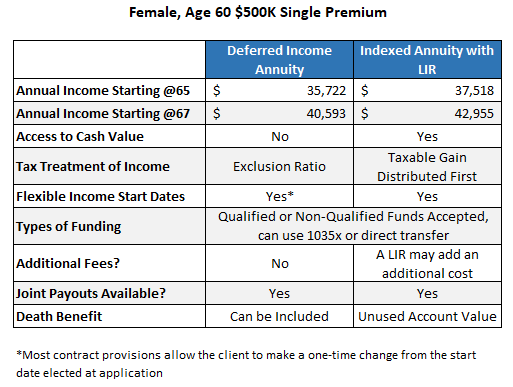

For several reasons, she likes the idea of a policy that generates a deferred income stream, and her advisor helps to explain the key differences between the 2 options:

Tell your clients not to wait! Purchasing a policy at a younger age, with a longer deferral period means that their money can go further in retirement.

Before You Take That App…Are You Up to Date On Your Compliance Requirements?

Many states have now adopted the 2020 NAIC best interest standard. If your state has adopted the new model, you must complete either a refresher course or a new compliant course in order to sell fixed annuities. Even if your state has not YET adopted the new model, you can still take the updated course to get ahead of the curve.

If you haven’t looked at annuities in a while, call AgencyONE! Rising interest rates have already had a positive effect on the annuity market, making them a more attractive option now and in the future.

")