You’ve heard it before. No one drinks enough water! Health experts say we should be drinking at least 6 x 8oz glasses of water every day. Water keeps everything working properly – from moderating your temperature to helping protect your joints to ridding your body of waste; water is integral to our body’s proper functioning. If you aren’t drinking enough water, your organ systems are working too hard!

Dehydration, Exercise & Underwriting

Just this week AgencyONE has seen 3 cases with insurance labs (urine testing) come into underwriting with LOW Glomerular Filtration Rate (GFR) numbers. This is NOT because of kidney problems, but more likely because of DEHYDRATION or not drinking enough water. A Home Office underwriter cannot dismiss low kidney function numbers assuming they are the result of simple dehydration, so your clients are asked to provide REPEAT URINE TESTING – sometimes on TWO DIFFERENT DAYS just to provide evidence that they are healthy. Low GFR is one of the most common and PREVENTABLE abnormal urine test findings.

What is GFR?

The Glomerular Filtration Rate is the best overall indicator of kidney function. GFR is not a “measurement”. It is a calculated number based on age, sex, body size, and serum (blood) kidney function values like Creatinine. Low GFR numbers indicate impaired kidney function until proven otherwise. As we get older, GFR naturally falls. You WANT your GFR numbers to be HIGH since that indicates GOOD kidney function.

What is Creatinine?

Creatinine is the residual compound or waste that comes from the body’s energy production. Creatinine also measures how well your kidneys are working and plays a role in GFR. The higher your serum creatinine, the lower your GFR number will calculate. What can you AVOID doing that could elevate your serum creatinine levels? You can AVOID EXERCISE. Conversely, what can you do to LOWER your serum creatinine? Don’t exercise and hydrate well by DRINKING MORE WATER!

Exercise and insurance exams do not MIX. Exercise raises serum creatinine as muscles work hard and create waste. Exercise can bounce the kidneys (jogging, treadmill, even bicycles) which may cause damage to the kidney’s micro blood vessels and make them “leak” protein. This is not a good thing within 48 hours of insurance exam testing. These are simple preparation instructions for your clients before they take their insurance exam: Hydrate well and don’t exercise. If your client DOES have kidney disease, these actions will have little or no effect on their numbers.

What is Proteinuria?

It’s a big word but it just means protein in the urine. You shouldn’t have any normally, but exercise-induced proteinuria does happen. A certain amount of protein is not considered pathologic, so thresholds have been established as “normal”. However, exceeding certain levels of protein in the urine will raise red flags in your clients’ underwriting for life insurance protection. Abnormally high levels of protein in the urine will likely result in the underwriter asking for REPEAT URINES possibly on two different days. This is a painful result for everyone if all you needed to do was advise your client NOT TO EXERCISE before their insurance exam. PROTEIN in the urine is one of the most common and PREVENTABLE abnormal urine test findings.

Case Study – Huge Premium Swings

We could write all day about kidney functions, but MONEY TALKS. Let’s take a look at the implications of a client who has NOT prepared for the exam urinalysis through a real-life example.

Mary is a 50-year-old healthy female with no significant medical history. She has an optimal build, takes no medications, and seemingly meets all best-class criteria. She has applied for $5,000,000 of20-yearTerm life insurance coverage for family protection. Mary completed her life insurance exam, and the results were all within normal limits EXCEPT that her urinalysis revealed the presence of some protein. Although the proteinuria was mild, it was enough to knock Mary out of consideration for preferred classes, including her application for best class. Standard Non-Tobacco was her best-case scenario with the current urinalysis results. This unexpected turn of events led to a discussion with the advisor about the necessity of thorough exam preparation with all clients.

Mary, unfortunately, did not follow the AgencyONE Exam Prep Sheet or watch the AgencyONE Exam Prep Video we created and that her advisor sent to her. Being the active individual that she is, Mary engaged in multiple HIIT workouts in the days leading up to her exam. She also admitted to not drinking nearly enough water the night before and morning of her insurance exam. Knowing that this was not likely to be a chronic kidney disease case but instead simply poor preparation, AgencyONE recommended Mary repeat her urinalysis with her primary physician. This time around, Mary followed all of our tips for proper exam prep and her urinalysis was completely within normal limits with no proteinuria whatsoever! Given the favorable repeat, we were able to negotiate Mary back to BEST CLASS rates and save her literally THOUSANDS OF DOLLARS!

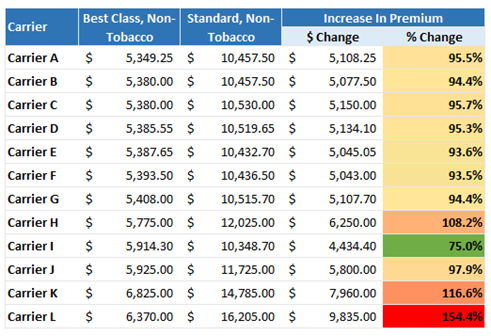

The following table reflects how the top 12 carriers would price Mary’s case (50 yo female, $5M of 20-yr Term) and shows the substantial difference in the premium for a Best Class versus a Standard Non-Tobacco rating.

Bottom Line: Instruct your clients to DRINK MORE WATER and NOT to EXERCISE for 48 hours prior to their Life Insurance exam. INSIST that they prepare for their insurance exams by watching the AgencyONE Exam Prep video. It will help to SAVE SIGNIFICANT time, ELIMINATE potential client FRUSTRATION, and result in a MUCH LOWER life insurance PREMIUM.

AgencyONE’s Underwriters are well-versed in underwriting medical complications and possess deep knowledge on which carriers underwrite and price specific conditions best. We are available to discuss any concerns or issues you and your client might have regarding their underwriting. Please contact the AgencyONE Underwriting Department at 301.803.7500 for more information or to discuss a case!

AgencyONE’s weekly ONE Ideas are designed to discuss a range of industry topics that are linked to current trends in Advanced Markets, Case Design, and Underwriting. Once a month, we will be offering a ONE Idea RECAP that summarizes the most recent articles from the month with links to the full copy. This time, we have also included a list of all of our published ONE Ideas from the last 6 months with a hotlink to each. If you’ve missed anything in the last few months, you will have easy access to them here.

We started the month of February with an Underwriting ONE Idea on February 7 entitled “Reinsurance DIRECT Underwriting – A Strategic New Approach to Challenging Cases”. This piece from Dennis Bartos, PA explored a powerful underwriting opportunity and our selection as a pilot site for testing a NEW DIRECT UNDERWRITING program. In the first 60 days of using this program, we had tremendous success with several of our AgencyONE 100 advisors’ large cases which were granted improved underwriting.

Our second ONE Idea for February came From the Desk of Gonzalo Garcia, CLU on February 17 and is entitled “A Look Back & A Look Ahead”. This article is a reflection on the industry in 2022 and what we might expect this year. Gonzalo discusses his concerns in both the carrier/ manufacturer and distribution sides of the business and what that could mean for our industry moving forward. Interest rates have affected carrier product line-ups and the direction many of their businesses have taken. These changes in distribution have been gearing up for a while and many M&As and consolidations have already happened. Gonzalo also reflects on the excellent year that our AgencyONE 100 Advisors had in 2022 and the exciting things we are all looking forward to this year. Our AgencyONE 2023 Annual Advisor Conference took place from April 30 through May 2 2023, and was immediately followed by a second meeting called the High-Performance Collaborative Teams on May 3. Click HEREfor MORE information on both meetings, which took place in Washington, DC at the Dupont Circle Hotel. We hope you enjoyed your time at the meeting, and if you weren’t able to make it, we hope to see you at next year’s meeting!

ONE Idea number three for the month came From the Desk of Ed Stark, CLU, ChFC on February 27 and is entitled “What’s for Sale in 2023 & Product Success Stories”. This article offers a refresher on current product availability and new opportunities that have brought recent success for our AgencyONE 100 Advisors and their clients. Ed outlines the specific products and the steps AgencyONE took to help the advisor achieve the financial planning goals of the client.

Please note that you can always find our most recent ONE Ideas listed under “Updates” on our website homepage. Additionally, a full library exists on your personal Dashboard on our website under the Sales/Marketing tab (you are required to have a website login for access to the complete library).

Following is a list of all our ONE Ideas from the last 6 months:

We are pleased to provide these ONE Ideas to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciate the opportunity to serve you and your clients.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information

It is hard to believe that we are more than 8 weeks into 2023 and that March starts this week! January and February flew by and were extremely busy for everyone at AgencyONE, which means that our AgencyONE 100 Advisors are busy, and that is GOOD for all of us! Historically, the first two months of the year were a time to finish up the business that did not place at the previous year-end, but this year we have received a higher number of new case opportunities than in years past!

I thought that a great way to begin my ONE Ideas for 2023 would be a refresher on current product availability, the carrier partners that AgencyONE works with, and new opportunities that have brought recent success for our advisors.

Term Insurance Options

The full range of typical Term options are 10, 15, 20, 25, and 30 years. However, there are a few outliers such as:

ART or One Year Term (not many carriers have this option)

Return of Premium Term

A few options for 35-40 yr. Term (depending on client age)

When considering Term, it is extremely important to look at the carrier’s current conversion period or whether a conversion option is available. In some cases, you can lock in more favorable conversion terms for only a small increase in premium. We have had terrific success with our Accelerated Underwriting options. The turnaround times and ease of issue have really helped with smaller transactional cases. While not everyone will qualify through one of these programs, when it works, it works very well.

Success Story: One of our carrier partners had an Accelerated Underwriting case applied for, issued, and approved all in less than an hour!

Whole Life Options

Whole Life (WL) is still a popular quote option for AgencyONE. Whole Life comes in Single Pay, 10, 15, 20, Age 65, A100 and A121 varieties. There are also a few non-par WL options that look like a guaranteed cash value GUL. A popular design we see often is using 10-pay WL. Many advisors are selling a Life Insurance Retirement Plan design which is a shorter pay strategy designed to grow cash value and provide future income. This is run in comparison with an Accumulation IUL.

Success Story:AgencyONE was in competition with an IUL income design. The client felt they already had too much equity exposure and liked the Whole Life accumulation strategy as an alternative. The client ended up purchasing a 15-pay Whole Life policy to guarantee the pay period, then showed competitive distributions from ages 70-85. This product also had an available LTC option, which the client declined adding.

Universal Life Options

Universal Life (UL) is still hanging in there and shows in a couple different versions. There is Current Assumption UL and a Guaranteed UL. When you think of Current Assumption UL there is a flagship option which is still the low-cost leader. It is extremely competitive in cost and flexible in design and even offers a true Long Term Care rider. Did I mention that this product has actually RAISED their crediting rate 2 times over the last year? On the Guaranteed UL side we still have 10 products available. (That number drops to 4 in NY). GUL products can be:

designed with specific guarantee periods

paired with refund of premium options and/or LTC – Chronic riders

funded on a level pay basis

Success Story: We had a client who wanted to guarantee coverage only to age 80 but wanted options to extend coverage down the road, if needed. We showed him a Guaranteed UL product that offered the option to continue the coverage with future stepped premiums FULLY GUARANTEED. We provided level premiums to age 80, and then stepped the premiums to age 85,90, and finally to age 100.

Indexed Universal Life Options

This is the product line most of you have probably been waiting to hear about. Indexed UL has been one of the top product lines for the last few years. Carriers have carved out their niches with both Protection and Accumulation products to best meet your clients’ needs. Doing a quick product count – there are over 22 Accumulation IUL options and over 16 Protection IUL products! While the majority of available IUL is on the protection side, we have seen a large uptick in the accumulation side of this business.

Protection Indexed Universal Life

AgencyONE has access to Protection IUL that can be fully guaranteed, guaranteed to a specific age and others that have life expectancy based guarantees. It is important to have some amount of built-in guarantee in these products. These are also the products most likely designed with either a LTC or Chronic Illness rider as an added benefit. When running these scenarios, always consider a crediting rate lower than the current AG49A rate.

Accumulation Index Universal Life

In order to design the most efficient Accumulation IUL policy, you need to use a minimum non-mec death benefit. Using the lowest death benefit possible helps keep policy charges down while accumulating cash values. Many offer the option to add LTC/Chronic Riders but be aware that this will cause extra drag on the cash accumulation. Also, remember that you cannot take Income and LTC benefit from a contract at the same time. Finally, when choosing a product, it is advisable to review the available index fund list so you are aware of the options you can pivot to down the road. When choosing a specific fund, spend time learning about the index credits (participation rate and cap rate) and the current and guaranteed rates. Always consider a crediting rate lower than the current AG49A rate to compare projections. AgencyONE can help you sort through the options and find one that will best address your client’s needs.

Success Story:We had a case with a client who wanted to purchase a large, overfunded accumulation policy and add in a large 1035 from a prior contract. The advisor did a great job explaining the product, index options, and added riders that were available. The client asked about adding a LTC coverage rider. Because the client would not be able to take income and a LTC benefit at the same time with this particular design, we pivoted to another carrier that would allow the 1035 to be split into two available product solutions – Accumulation IUL for the cash accumulation and a hybrid LTC product to cover the LTC requirement.

Survivorship UL/IUL

There are still plenty of good options for survivorship coverage with products built on a UL, IUL and VUL chassis. Most of these are still sold with full guarantees but some of the indexed options have the possibility of cash value growth in exchange for guarantees. One specific carrier partner offers LTC on both clients if they qualify through underwriting and each client can obtain ½ of the death benefit for LTC, if needed.

Success Story:We started a large survivorship case with full guarantees to age 121. Upon review of the IRR’s, the advisor asked if we could improve them. We came back with a lower premium solving to the client’s life expectancy and then added in “catch ups”. The original IRR in yr. 20 was 11.45%. The new projected IRR increased to 17.71% with a guarantee to age 93 on this particular case!

Variable Life Options

VUL business has picked up at AgencyONE in a big way. VUL products can be designed for income or death benefit guarantees, depending on the need. They tend to be more competitive in short pay or large dump in scenarios. There are also Survivorship VUL options that are competitive for either Guarantees or Cash Accumulation. Some of the available riders on VUL contracts are:

1. LTC or Chronic riders

2. Critical Illness riders

3. Return of Premium Death Benefit options

4. Indexed Accounts

Success Story:(an illustration success story): An advisor and client wanted a Guaranteed Survivorship option funded on a single pay basis. Using a $1,000,000 single premium, they were able to buy $2,010,000 of guaranteed coverage to age 110. While the client and advisor liked the guarantees, they were concerned about the lack of cash values. AgencyONE alternatively ran an Accumulation SVUL at a 5% ROR. We solved for DB to age 110 and received $2,525,000 of DB! While this had the projected cash values, they wanted the guarantee dropped to age 84 assuming 0%. The decision on this case is still pending.

Hybrid LTC Products

The AgencyONE team has definitely increased our hybrid case quoting. These products can be challenging to illustrate and compare since age-of-client may impact pay or benefit periods. These are great options to show your clients if they are afraid of a “use it or lose it” scenario. They also provide a fully guaranteed solution. Our most popular designs are single-pay and 10-pay currently.

Success Story:We placed a policy on a 56-year-old client through an Accelerated UW Process which was applied for electronically and approved in 4 days!

AgencyONE is happy to schedule a call with you to discuss sales ideas or product options in more detail. Please reach out to the Case Design Department at 301-803-7500 for more information or to discuss a case.

I am certain that many of you are happy that 2022 is over and that we are now 8 weeks into 2023, but, and this is a big but …. Is this year really going to be any different or will it present any fewer challenges than 2022?

Last year, most people were thinking about the economy and its impact on inflation and the equities market. Consumers watched their portfolio values go down, the prices of goods and services go up, and the supply chain present serious challenges. On top of this, the Russian invasion of Ukraine had a massive impact on fuel prices and created unease for global peace combined with China’s ongoing aggressiveness in the Pacific. This continues to create anxiety around financial security for many.

Notice that I did not mention the January 6th investigation, the mid-term elections, or the most recent House Majority vote. The US, despite the divisiveness and our ongoing political challenges, is still the US. Like all others, the US economy is cyclical and market forces are always at work, but it is still the most stable economy in the world.

Economic forecasts for 2023 were all over the place. On June 1, 2022, Jamie Dimon, JP Morgan Chase CEO, said on CNBC:

‘brace yourself’ for an economic hurricane caused by the Fed and Ukraine war.

Then months later Barron’s Daily reported:

Take heart from JPMorgan Chase CEO Jamie Dimon. He clarified Tuesday that maybe he shouldn’t have said last year that an “economic hurricane” is coming. There are clouds for sure, but he didn’t mean to predict widespread collapse. His bank is still hiring.

That notwithstanding, the direction of the market is either up or down, right? Maybe flat? But should that change the way comprehensive financial advice is provided to consumers relative to their financial security and retirement planning?

On the “good news” front, 2022 saw the COVID pandemic begin to wane, although new strains of the virus continue to emerge. We will see what the depths of the 2023 winter season brings but the death toll is WAY down and, not to minimize the impact, most people are breathing a little easier – no pun intended. During the COVID pandemic we saw a large increase in the demand for individual life insurance, but as 2022 rolled toward the end, the mortality “scare” began to fall off and Q3 sales were down year-over-year by 5%, according to LIMRA. Regardless, results through nine months were up 6%. Overall policy sales were down 12% in Q3 and 10% year-to-date (2022). The only product that experienced growth was Index Universal Life (IUL). It will be interesting to see how the year ended as the numbers are gathered and reported.

There are a FEW things, however, about the insurance industry that worry me both on the carrier\manufacturer side and on the distribution side.

CARRIERS

One would think that an increase in the 10-Year Treasury rate, which is a bellwether indicator for insurance investment portfolios, would be welcome news and to a certain extent it was. 10-Year Treasury rates increased from a bottom of around .52% in mid-2020 to its current level of 3.5% with a peak in late 2022 of 4.25%. It makes sense that new premiums received are invested in higher-yielding instruments and that the interest rate, passed onto policyholders in the form of interest or dividends, would go up. We certainly saw this in the annuity space, with its massive sales in 2022 and no end in sight as interest rates continued to increase.

On the life insurance side, it was a very different story. There was ONE company that I can think of that announced interest rate increases on their current assumption life product, and they did it twice during the year – that was John Hancock. To my knowledge, only one of the big mutual carriers increased dividends and this was Guardian, who increased dividends by .10% from 5.65% to 5.75%, while all the others held steady.

Life insurance portfolios do NOT move as fast as current interest rates. These portfolios are massive and the return drag due to years of low-interest rates will stay with us for some time. Think of the Titanic – you get it.

The bigger story is the impact that guaranteed products, such as GUL and certain annuity-guaranteed benefits, had on some insurers – notably Lincoln Financial who reported a $2.6BB loss on their Q3 earnings call.

“The loss was due mainly to a $2.2 billion increase in life insurance reserves, based on data showing that people ages 75 and older are more likely to keep guaranteed universal life insurance policies than the company had expected, and to a $634 million reduction in life insurance unit goodwill, according to the company’searnings announcement.

The net loss will have no effect on Lincoln’s cash flow, but it will cut the company’s statutory capital by about $550 million in the fourth quarter, the company said.”

READ – Lincoln sold a lot of underpriced GUL policies to older-age clients and did not expect persistency to be as high as it is. Clearly there are other factors, but this is the ”nuts and bolts” of the challenge.

Prudential reported a similar write-down of over $1.4BB in Q2. Their announcement states that “This decrease includes an unfavorable comparative impact from our annual assumption update and other refinements of $1.408 billion, primarily driven by updated policyholder behavior and mortality assumptions in the current quarter. Excluding this item, current quarter results primarily reflect lower net investment spread results and higher expenses, partially offset by more favorable underwriting results.”

READ – they sold a lot of underpriced GUL policies to older-age clients and did not expect persistency to be as high as it is. Clearly there are other factors, but this is the “nuts and bolts” of this challenge.

There are other notable challenges related to these guaranteed benefits in the recent past, such as Ohio National, which was ultimately sold to Constellation Insurance, a Canadian insurance holding company for $1BB with money from public pension plans. Their problem was primarily driven by Guaranteed Withdrawal and Income benefits resulting from their legacy Variable Annuity book, among other things.

Principal Financial Group exited the individual life business and are focused on the business owner market. American National recently exited the term business market …. I could go on and on.

The market is challenging for insurance companies, but not really because of current economic conditions. They are shoring up financial reserves due to past mistakes in pricing and persistency assumptions and trying to find a balance in an increasing interest rate environment after years of decreasing portfolio returns. Remember that the value of bonds purchased in the last years are meaningfully impacted due to a sharply rising interest rate environment. As a wise industry analyst once said to me “the insurance business is a LOOOOOONG business and mistakes from 10, 20 or even 30 years ago can come back to bite you in the behind”.

This is not to say that the industry is facing existential challenges. Statutory capital for the industry is generally strong and contractual guarantees are safe – they are just not profitable for the issuing carriers. Stock companies care about this more than mutual companies.

I expect to see more exits from the guaranteed benefits space, including long duration term insurance, or at a minimum, continued price increases. I also expect to see a tightening in underwriting offers.

One last comment, which is pure speculation on my part, is that while the insurance industry is trying to find a way to expedite underwriting through algorithmic processes and big data, the longer-term impact on mortality is yet to be determined. It is just too soon to tell what the impact of these algorithms and all this automation will be. They can afford to make some mistakes if they can cut significant expenses through automation, but only time will tell.

DISTRIBUTION

This is likely the biggest story of 2022. It is no secret that the advisor community is aging, as is the ownership of Brokerage General Agencies (BGAs) and Independent Marketing Organizations (IMOs). Private equity has fueled a ton of Merger & Acquisition (M&A) activity in many areas of our profession, including the retail Investment\Wealth Management space. In this space, advisors are seeking independence from career insurance platforms such as Northwestern, Mass Mutual, New York Life, etc. and also from the large wires such as Wells, UBS, and so on.

Similarly, the insurance distribution arena has seen massive consolidation, specifically in the aggregator space. Companies like Integrity,Simplicity, AmeriLife and others, fueled by private equity firms such as Aquiline, Silver Lake, Harvest Partners, Lee Equity Partners and Genstar Capital are buying everything in sight. Of particular note, in 2022 alone, Integrity Marketing acquired notable firms in the insurance space such as Ash Brokerage, One Resource Group, Lion Street and Annexus.

Firms such as Gallagher, Acrisure, HUB and others like them have also entered the wholesale distribution of individual life and health insurance, primarily through their presence in the Employee Benefits and Property\Casualty space.

Even the association space has experienced consolidation, as we saw Finseca merging with the Forum 400 and the National Association of Life Brokerage Agencies (NAILBA), to add to their previous merger with the General Agents and Managers Association (GAMA). Finseca now stands as the preeminent representative of the financial security profession. If you are not a member, you should be.

Finally, consolidation of the IMO has also occurred. AgencyONE is privileged to be a partner of LIBRA Insurance Partners, an organization of which I am on the Board. During the last two years, LIBRA has successfully merged with two other IMOs, Brokerage Resources of America (BRAMCO) and Insurance Designers of America (IDA), forming the largest independently owned insurance distribution company in the United States with $600MM of life insurance premium production and close to 100 firms.

Consolidation is happening right in front of our eyes. Having been through a wave of this before in the late 90s and early 2000s, I have witnessed the good, the bad and the ugly of this sort of market dynamic. While it is an exciting time for many, the consolidation of insurance distribution is here to stay and will create both challenges and opportunities.

TECHNOLOGY

This is another area where we saw great strides in 2022 as we came out of the COVID pandemic. As many of you know, the pandemic created an environment where meeting with clients and taking applications in person, never mind getting people examined for insurance, was problematic. In spite of this, applications and premiums during 2021 increased due to the high demand for life insurance caused by the pandemic. As mentioned before, while business was down industry-wide, carriers committed to getting on the technology bandwagon.

Insurance companies accelerated their technology spend and projects in a massive way, as did many providers in the big data space, specifically around prescription checks and electronic health records. 2022 was, in a sense, a frustrating year as the launching and “de-bugging” of a lot of this technology happened. The digital end-to-end process for insurance is here – from application to delivery; the so-called pain points of applying for life insurance are being substantially removed and there is no going back.

Similarly, massive amounts of spending have occurred on the in-force policy servicing side with many carriers creating a much more robust process for client service. While still not great, some companies are shining while others are struggling to get on board. This will further differentiate who you should consider doing business with going forward.

AgencyONE

AgencyONE had a great year in 2022 and we would like to thank all of you who supported our growth and selected us as a partner to help serve the financial security needs of your clients. We have a lot of plans for 2023 but will continue to focus on “serving a small group of insurance advisors in a very big way” as is our mission.

As I look at our profession, I see an inflection point. A lot of it driven by the demographic changes and the massive wealth transfer happening right before our eyes. The financial services and financial security profession will either continue to jockey for position or finally come together to serve the American consumer more holistically. If we are not careful, however, the risk of commoditization will continue to impact our livelihood. We cannot measure ourselves by the cheapest price, the lowest fees, or the highest investment returns.

Consumers want a financial guide or coach and don’t want to have multiple people advising them in different lanes. Collaboration amongst advisors (Accountants, Attorneys, Investment Advisors and Risk Management Advisors) will be key, allowing each to play their specific and very important role. AgencyONE wants to be at the forefront of this collaborative effort.

Our Annual Advanced Markets and Underwriting conference took place on April 30 through May 2 at the iconic Dupont Circle Hotel in Washington DC. At all of our conference events, you can expect to see what we have delivered for many years – excellent speakers and topics, great networking with some of the best insurance professionals in the country and a little bit of fun along the way. The event was well received, and we look forward to hosting another successful conference in 2024!

To further our objective of collaborative planning, in November 2022 we experimented with a High-Performance Collaborative Teams meeting in Boston. We made mistakes, we learned a lot, and the meeting validated our belief that collaborative planning is good for the client and produces more and better referrals for the life insurance advisor. We will continue with this one-day training in San Diego on March 1 and have another event after our Annual Conference on May 3 in Washington, DC.

Finally, during 2022, AgencyONE launched our Insurance Network for Fiduciary Advisors (www.in4fa.net). This is a collective of carefully selected insurance-only advisors who will work with the RIA\CFP Fiduciary market to assist them with the risk management needs of their clients. Again, collaboration.

Thank you again for your continued support and friendship. We look forward to a successful 2023.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

Our AgencyONE 100 Advisors are veterans of the life insurance business and understand the importance of reinsurance in the placement of their larger cases. That said, we are pleased to announce a new and powerful underwriting opportunity that will help to shift some of your more difficult cases into the PAID column! AgencyONE has been selected as a PILOT site for testing a NEW DIRECT UNDERWRITING program with a highly rated company that has approximately $3.5T of life reinsurance in force. AgencyONE has had remarkable success in the first 60 days of working with this reinsurer as several of our advisor’s large cases were granted IMPROVED underwriting status by their underwriting team. This allowed our carrier partners to assign their RISK component to our reinsurer and issue policies that were otherwise NOT going to be placed! This is a WIN for the Carrier, Reinsurer, and your Clients!

A Selective Tool for Certain Cases

This underwriting tool is for selective use and NOT for every case situation. However, when carrier underwriting is short of the mark, you now have a new and powerful underwriting option to consider. This ONE Idea examines 4 case studies and the very important role the Reinsurance Direct Underwriting program had in the placement of problematic and difficult cases.

As you know, AgencyONE does NOT SHOTGUN business into the marketplace. If a case is sent shotgun to 15 different companies, that means that 14 companies will be left without a case, if the case even places at all. AgencyONE has a reputation for DIRECTING business and TARGETING the RIGHT PRODUCT solution while GUIDING the case towards the expected underwriting result. Our very high placement ratios on Informal Inquiry business reflects our professional underwriting philosophy and respect for the home office underwriter’s time. Generally speaking, any company we have directed a case to has about a 1 in 3 chance to “win” the case.

Having a direct reinsurance relationship gives AgencyONE the ability to send your larger cases DIRECTLY into reinsurance underwriting UPFRONT! This program is the KEY to matching our negotiated reinsurance underwriting to life insurance carriers – who have a treaty with this reinsurer – and their products that satisfy your clients’ needs!

Additionally, in a situation where a carrier decides to rate, postpone, or otherwise provide an underwriting decision that does not match up with our expectations, we can take the case DIRECTLY to our reinsurance underwriting team for a second opinion!

Case Study #1

Survivorship policy AND Individual policy on male needed

Individual male policy required guarantees and a 10-35 situation

AgencyONE preliminary underwriting opinion: male and female risks – PREFERRED NT

The survivorship policy was placed inforce without a hiccup. However, the individual male case was targeted to two specific carrier partners as “best product” selections for a Variable Life contract with guarantees. This part of the case involved an $844,000 10-35 possibility. AgencyONE expected Preferred ratings but did not get them from either carrier, upfront OR on appeal. AgencyONE then took the case for a Second Opinion to our reinsurance underwriting team and they agreed that the client COULD be considered on a PREFERRED basis. We chose SECURIAN as the carrier to align with this case because of superior product performance under these specific circumstances. Securian was now able to ISSUE the coverage at PREFERRED with full reinsurance support of the risk! $2.7 million in coverage for the client at Preferred Rates and the rescue of $844,000 in 10-35 funds! A win for everyone!

Case Study #2

Kidney transplant client

$5 million of protection needed

The advisor submitted formal applications and an AgencyONE HIPAA targeting a specific carrier for the case without first discussing it with the AgencyONE underwriting team. The advisor chose the wrong carrier which resulted in a Table 8 offer. The carrier would not budge in negotiations. AgencyONE ran a series of “what if” illustration scenarios for other carrier selections but opted to go to our reinsurance underwriting team UPFRONT. The risk was negotiated with reinsurance FIRST and resulted in a Table 4 offer which allowed placement with a Cincinnati Life product matchup. The premium was nearly $60,000. Another win for everyone!

Case Study #3

TYPE I Diabetic since age 13 with a high substandard rating

$3 million of protection needed

AgencyONE received a formal submission and an AgencyONE HIPAA for $3 million of protection. While it is not unusual for a Type I diabetic early onset to be declined outright by many carriers, the selected carrier made an offer. However, the offer was a high substandard rating and the numbers did not fit the case or the client’s budget.

Knowing we needed a better underwriting offer to make this case work, an informal submission to our reinsurance partner was the next best step. The file was submitted directly to our reinsurance partner’s underwriting team who, given the client’s excellent diabetic control and renal functions, was able to provide a tentative Table 4 offer. With an offer in place, AgencyONE’s underwriting team was able to “match” the reinsurance offer with participating carriers. This case matched with Protective Life products. The client was so pleased with “the numbers” that this term case turned into a split case with both PERMANENT protection and an additional TERM sale. Another win for everyone!

Case Study #4

Cash accumulation needed

$50,000 annual premium budget

Advisor – Targeted Nationwide product, Standard risk expected

If you send a case to 3 companies, it is not unusual to get 3 different opinions. In this final case example, the advisor targeted NATIONWIDE for a $50,000 PREMIUM cash accumulation sale for the NEW HEIGHTS Index Accumulator product. A STANDARD underwriting assessment was expected, but a substandard offer came back that was not placeable. AgencyONE took the case directly to our reinsurance underwriting team and negotiated a possible STANDARD offer. Nationwide IS a participating carrier with our Reinsurance Direct Underwriting program. We went back to Nationwide and aligned the reinsurance support which allowed us to ISSUE the Nationwide Product at the desired STANDARD rate class!! Another win for all parties!

AgencyONE has chosen to work with a small group of advisors – our AgencyONE 100 – in a very big way! This small group approach allows us to provide unmatched, personalized service. AgencyONE’s close working relationships with our strategic partners in the carrier space and in the reinsurance arena means we can offer YOU the highest level solutions and access to the most specialized programs.

As professional advisors, you are free to choose with whom you do business. When you are thinking about WHERE to direct your business in 2023, we sincerely hope you will consider the AgencyONE team.

Please contact AgencyONE’s Underwriting Department at 301.803.7500 for more information or to discuss a case.

With the new year, many advisors are thinking about ways to work more efficiently and increase their business. Annual client policy reviews are a great practice to evaluate and update your clients’ financial plans and also to further nurture your client relationships. Whether performed at the end of the year or at the beginning, policy reviews are well worth the time spent. They get you “in front” of your clients, help to increase client trust in you, and may potentially mean more business for your practice.

This ONE Idea provides carrier product information to use during policy reviews – or at any time – with your clients who have term policies and might be interested in converting to permanent OR supplementing their existing term policies with a permanent policy as well.

Depending on certain qualifications and state availability, your clients with term policies may be able to qualify for one of two carrier programs. Please note that each carrier has specific requirements, so it is important to familiarize yourself with qualifications and state availability. AgencyONE can provide you with this information.

Term Conversion Option – Term to Perm

Carrier partner A offers a program for a term conversion to a permanent product only. Policyowners who have purchased a fully underwritten single life term insurance policy from a select group of carriers within the last five years may be eligible to convert that external term policy to a permanent Carrier A life insurance policy. Available conversion solutions include Accumulation, Protection, and Current Assumption UL products. The minimum face amount is $100,000 and the maximum face amount is $1,000,000. Following are Carrier A’s current underwriting guidelines for their program:

Minimum age for new policy is insured age 18

Maximum issue age for new policy is insured age 65

New policy is limited to the Level Death Benefit option

Underwriting of the original term policy must have occurred within the last five years based on the issue date and the risk must be classified as standard or better

New policy will be issued at either a preferred or standard rate class

Nicotine status for the new policy will be the same nicotine status as the original policy

Your AgencyONE case designer is available to discuss this program along with Carrier A’s list of eligibility requirements and accepted carriers. We are also happy to provide sample conversion illustrations if needed.

Supplemental Perm with Existing Term Option – NEW Permanent Coverage with ZERO Underwriting Required

Carrier partner B’s program offers clients, who have existing term life insurance policies with other carriers the opportunity to purchase a permanent life insurance policy from Carrier B without the requirement of additional underwriting! (Subject to a list of Term policy stipulations and underwriting and policy issue requirements). Carrier B’s program was designed to offer additional, rather than replacement, coverage. If a replacement becomes part of the transaction, normal replacement rules apply.

Additional Carrier B program benefits include:

A streamlined life insurance buying process

A client with an eligible term policy issued in the last 3 years can buy a new permanent life insurance policy from Carrier B with no additional underwriting requirements

Policy face amounts up to $5 million

Ages 18 to 50 – $100,000 to $5 million face amount

Ages 51 to 60 – $100,000 to $1 million face amount (equal to or less than the existing policy down to $100,000)

Option to add cash indemnity Long-Term Care Rider

Simply complete the Long-Term Care Supplement Form, no receipts required once a claim has been established

Clients can choose to keep their existing term life coverage in place

Policyholders can get a separate permanent policy and are not required to replace their term life insurance for permanent coverage

This program also has quite a few policy qualifications and requirements. Please contact a member of your AgencyONE case design team for more specifics about this program.

AgencyONE’sCase Design Department is pleased to continue to provide our AgencyONE 100 Advisors with carrier solutions and product intelligence that addresses their client’s current and changing financial and insurance needs throughout the year.

Please contact the AgencyONE Case Design Department at 301.803.7500 for more information or to discuss a case.

I regularly read financial articles before I start my workday, or late at night when I can’t sleep, which occurs more and more as I grow older. And why not? Is there a better remedy for insomnia than a boring financial advice article?

What is disappointing is when I see an article that I feel that I absolutely must call out, not as much for the inaccuracy, but for the oversight. The most recent example of this is an article titled “6 Types of Retirement Income That Aren’t Taxable”by John Csiszar which appeared on GOBankingRates.com on December 10, 2022. Mr. Csiszar is both a Certified Financial Planner (CFP) and a Registered Investment Advisor (RIA), and according to his bio in the article, is also a licensed life agent with experience in a Wall Street wire house and has his own investment advisory firm. He manages over $100 million of client assets “while providing individualized investment plans for hundreds of clients”.

The author’s intentions and, frankly his guidance, are great as he spells out and discusses his list of tax-free retirement income options as follows:

Roth Withdrawals;

Inheritances;

Municipal Bond Income;

HSA Withdrawals;

Social Security Payments, with explanation; and

Life Insurance proceeds.

In item number 6, Mr. Csiszar states that “like an inheritance, waiting for a life insurance [death benefit] payout isn’t an ideal strategy for funding a retirement plan” and I could not agree with him more. HOWEVER, using tax-free distributions from life insurance policy account values is NOT even mentioned as an option in the above list!

Why is it so hard for financial advisors to recognize:

That cash values in a life insurance policy can be allocated to equities, bonds, cash, and alternative investment asset classes inside of the tax-deferred wrapper that is life insurance (assuming that the policy is a variable life solution).

That cash values in a life insurance policy can be bought and sold without capital gains or taxation thereof.

That dividends from the equities and interest payments from the bonds and other fixed-income assets are NOT taxable as ordinary income.

That the sum of all contributions made to life insurance (the basis) can be withdrawn income tax-free BEFORE any gains.

That ALL gains can be borrowed against at a ZERO or very low-interest rate.

That distributions from life insurance are NOT considered earnings toward the income test for the taxation of Social Security Benefits (as Mr. Csiszar mentions in point number 5).

That ALL or MOST of the Death Benefit can be accessed, income tax-free, as a living benefit through a Long-Term Care or Chronic Illness Rider, if elected, in the event the need arises.

That, in many states, cash value of life insurance is protected from creditors.

That cash value of life insurance is not considered for Federal Student Aid in the FAFSA forms.

That death benefits are income tax-free to the beneficiaries and are 100% liquid exactly when needed by the beneficiaries, regardless of financial market cycles.

There is no other asset like life insurance as part of a well-thought-out financial plan and yet, many financial advisors, such as the author of the aforementioned article are loath to mention it. Why?!

I could pontificate and make a whole list of objections such as:

That life insurance is too expensive – it’s not;

That life insurance agents get paid a BIG commission – they don’t;

That, as a result of the alleged BIG commission, life insurance agents don’t have the client’s best interest in mind – disagree, you need to work with the right insurance agent\ agency;

That insurance policies are rarely managed correctly – historically true, but there are many technology solutions for that today, so let’s get past that;

That life insurance is hard to qualify for – not true; and

That life insurance underwriting is an onerous task – again, historically true, but if you work with the right agent\ agency, it doesn’t have to be that way.

Let’s get over these objections, because at the end of the day, as highlighted in the Ernst and Young (EY) study from October 2022, life insurance, as part of a holistic financial plan can provide meaningful benefits to young families, mid-career men and women, pre-retirees and retirees. The earlier that individuals start with their planning to include life insurance, the more effective their plans will be.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

A quick policy review might be just the gift that your clients (and you!) are looking for this holiday season. Take just a couple minutes to read how a brief inforce policy review turned into two applications for over $250,000 of premium for our AgencyONE 100 Advisor.

Case Study – Mr. & Mrs. Snow❄️

Mr. and Mrs. Snow both had indexed annuity contracts crediting a fixed rate of 1% for the upcoming policy year with an S&P 500 cap rate of 1%. In other words, policies that are not competitive in today’s marketplace. With fixed annuity rates more competitive than they have been in many years, there is no reason for your clients to be missing market upside with a policy that credits only guaranteed minimum rates. The AgencyONE 100 Advisor presented two alternative options for his clients to consider:

Option one– a similar indexed annuity offering an S&P 500 point-to-point account with a cap rate 1,200% higher than that of the current policy

Option two- a 5-year multiyear guaranteed annuity with a 5.4% guaranteed rate –540% higherthan the fixed account rate in the current policy

Mr. and Mrs. Snow ultimately chose option two and submitted applications for policies that will significantly improve their position heading into the new year. Because they are still in the accumulation phase of their retirement journey, a new 5-year surrender period was an acceptable tradeoff for moving to a more competitive policy; the decision to 1035 exchange their current policies was an easy decision to make and the ultimate gift to themselves!

Bottom Line

If you have clients with inforce annuity contracts, (old Genworth policies or maybe those with a carrier who has pulled out of the market in past years) take this opportunity to contact them now. If you do not, you may be leaving money on the table, and more importantly, leaving your clients in contracts that are not competitive. Give your clients – and yourself – a gift this holiday with this easy annuity replacement opportunity.

Please contact AgencyONE’s Annuity Department at 301.803.7500 for more information or to discuss a case.

Did you know that AgencyONE can help you with your life settlement cases? As a result of a strategic relationship AgencyONE has with a premier life settlement broker, AgencyONE is uniquely positioned to help underwrite your client’s medical file and help the life settlement broker build the case to try and achieve the most value for your client. This ONE Idea will discuss what is happening in the life settlement market and how AgencyONE can provide value.

Life Settlement – Market Evolution

The early years of the Life Settlement markets were plagued with inefficiencies and poor regulatory oversight which resulted in a Wild Wild West environment of pricing and manipulation. State insurance departments stepped in to institute the much-needed regulation which has helped to increase transparency and the ethical handling of such transactions. As the industry has matured, so has its efficiency and its reputation. In fact, insurance commissions nationwide now believe that a financial advisor should consider a life settlement option as part of the due diligence process before a replacement, lapse or surrender. It is in the client’s best interest to consider all options!

That being said, the Capital Markets have taken notice of the improved efficiencies and tighter regulatory oversight. The investment community has embraced life insurance settlements with fixed premiums and guaranteed death benefits as a non-correlated asset that we know will ultimately pay a claim. While the stock markets may go up and down, the life insurance policy is a stable asset within any investment portfolio. More investment capital sources have realized the true value of a non-correlated asset block so demand for policies remains high. This in turn translates to a customer service value proposition.

Life Settlement – Some Interesting Statistics

The Life Insurance Settlement Association (LISA) provides an important market summary of transactions from 2021:

Consumers were paid over $750M by LISA Members for the sale of their unwanted life insurance policies, instead of receiving only $96M had they chosen to lapse or surrender their policy.

Consumers received an average of 7.8 times more than their Cash Surrender Value when they sold their life policy, translating into over $660M more in American seniors’ pockets than what they would have received from life insurance carriers.

More than 3000 transactions were conducted by LISA members totaling over $4B in Face Value. These figures represent just a tiny fraction of the 9 million plus policies & $642B that are lapsed or surrendered annually by life insurance consumers.

The average policy size, or amount of Net Death Benefit, per transaction was $1.33M.

Life Settlement – Policies That Qualify

Clients over age 65 with face amounts of $150,000 or more generally fit into the basic guide for life settlement consideration. The INFORCE illustration guidelines should be shown to “run” to age 105 with low-level premium payments. This structure helps the Provider/ Buyer (the guys with the checkbook) determine cash flow needs and expected returns on their investment in the contract.

Possible Clients for Life Settlement Consideration:

1. Policy premiums are too expensive and/or contract not performing

2. Policy is no longer needed

3. Liquidity needs

4. Revisions in tax laws or ultimate purpose of the protection have changed

5. Business Insurance needs changed

6. Existing Term is approaching maturity and conversion is too expensive

7. A 10-35 replacement is being considered and trustee is obligated to consider life settlement exchange option as a fiduciary of the trust value

The reality is that if you do not talk to your clients about life settlement, he or she may find someone else, possibly through a basic internet search or TV commercial, that is marketing directly to consumers. Please note that in this situation the policy buyers’ interest is rarely aligned with your client’s.

Through AgencyONE’s strategic life settlement relationship, we are able to work on behalf of the advisor and client to find the RIGHT buyer offering the best possible price for the policy. In this case, the policy buyers’ interest is in direct alignment with the client or the seller of the policy.

The full-service life settlement brokerage firm that AgencyONE has a strategic relationship with has over 20+ years of industry experience and delivers innovative planning solutions and unparalleled value to your clients. This firm understands that clients’ needs evolve over time and that an exit strategy using a life settlement is a very valuable tool to use when warranted. They also maintain important ties with the nation’s largest and most reputable life settlement funds and are considered experts in the field.

Lets look at a few life settlement case studies and the extraordinary value that has been provided to AgencyONE’s advisors and their clients recently:

Case Study #1:

The client was a 95-year-old male in perfect health with a Second-to-Die contract and a wife who predeceased him. The policy was a $1M UL with a cash value of $139K and a $286K cost basis. The policy was initially funded with a lump sum 10-35 and was only expected to last another 2 years.

The gross offer for the policy was $545K and it was ultimately sold using a fund that did not require life expectancies. The expectations of the client and the advisor were well exceeded.

Case Study #2:

The client was a 65-year-old male with 3 policies that totaled a $6M death benefit. The client intended on surrendering the contracts until his advisor explained that a better and more profitable way to dispose of the policies might exist. AgencyONE confirmed that the client “fit the box” and met the basic criteria for a life settlement consideration.

The case required a complete medical file which was quickly gathered by AgencyONE and included HAPI records (those gathered using Human API). Life expectancy reports were ordered by our strategic life settlement partner in Philadelphia on a rush basis and the bidding war began.

The initial $1.6M offer was ultimately negotiated UP to $2.52M gross and the proceeds were transferred to the client within 7 days of signing the closing documents. This case took a little less than 3 months from start to finish and again, the client and the advisor expectations were far exceeded!

The Life Settlement Value Proposition

The VALUE (what the policy is worth) is based on a number of factors, but client Life Expectancy calculations are the most important. A shorter life expectancy translates to less premium payment outlay for the buyer and a shorter-term investment in the policy overall. For the most part, the investment community is primarily interested in life expectancies of less than 15 years. Basic math would tell you that if the client is currently age 75 with a normal life expectancy of age 90, then a 15-year premium payment period should be expected before the maturity (the death claim) might occur. This is a long time period to tie up investment capital so shorter life expectancies generate higher interest and more competitive bids. It is extremely important to realize that PREMIUM PAYMENTS must continue to be made by the BUYER of the contract. From the CLIENT perspective, this policy remains INFORCE and must be reported by the client on any future life insurance application.

Whether the case involves building medical files or working closely with our strategic life settlement relationship to negotiate a maximum settlement price, AgencyONE is uniquely positioned to help you with your life settlement cases. We are also happy to host webinars or team calls to discuss life expectancy importance and how life settlements work.

Pick up the phone…give us a call….and please remember, a life settlement today can offer a RETAINED death benefit component instead of a 100% sale of the death benefit protection. It’s allabout theprice!

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

As interest rates continue to rise, so do the rates offered by annuity carriers. If you haven’t looked at annuities in a while, take this opportunity to get up-to-date on the most current offerings to help your clients prosper.

The Annuity Highlights

Consider a 5-Year Multi-Year Guarantee Annuity (MYGA) crediting 5.20% OR choose an A+ rated carrier for 5.15% OR capture MARKET UPSIDE while enjoying the principal protection of a 0% floor. ADDITIONALLY, S&P 500 point-to-point accounts have caps as HIGH as 11.0%!

Click HERE for a snapshot of AgencyONE’s top fixed annuity rates and payouts.

Fixed Indexed Annuity & Blended Allocation – Case Study

How can a fixed annuity with a blended allocation help your client prosper across a wide variety of market conditions?

One of AgencyONE’s core annuity carrier partners offers a Fixed Indexed Annuity (FIA) with a 7-year surrender period that currently credits 5.05% to the fixed account and has a current performance trigger rate of 9.55%.

What does that mean?

The policy’s Fixed Account credits an interest rate that is guaranteed for one year (in this case 5.05%), specified at each policy anniversary.

A Performance Triggered Account credits a specified rate (in this case 9.55%) if there is ANY positive growth in the S&P 500.

Let’s take a look at how a few different scenarios would play out given a 50% allocation to the policy’s fixed account and 50% to the performance triggered account, using today’s rates.

In a flat or positive year, the blended allocation returns 7.3%.

In a negative year, the blended allocation returns 2.525%.

But how often is the S&P 500 negative? According to Morningstar Direct, the S&P 500 has had positive returns 81% of the time over the last 20 years! With that in mind, let’s look at how a policy would perform over a hypothetical 5-year period:

Annuity solutions should be considered as a part of your holistic financial planning strategy for your clients. If you don’t talk about annuities, perhaps your competition will. Call AgencyONE today to see how we can help!

Please contact AgencyONE’s Annuities Department at 301.803.7500 for more information or to discuss a case.

")

You’ve heard it before. No one drinks enough water! Health experts say we should be drinking at least 6 x 8oz glasses of water every day. Water keeps everything working properly – from moderating your temperature to helping protect your joints to ridding your body of waste; water is integral to our body’s proper functioning. If you aren’t drinking enough water, your organ systems are working too hard!

You’ve heard it before. No one drinks enough water! Health experts say we should be drinking at least 6 x 8oz glasses of water every day. Water keeps everything working properly – from moderating your temperature to helping protect your joints to ridding your body of waste; water is integral to our body’s proper functioning. If you aren’t drinking enough water, your organ systems are working too hard! The Glomerular Filtration Rate is the best overall indicator of kidney function. GFR is not a “measurement”. It is a calculated number based on age, sex, body size, and serum (blood) kidney function values like Creatinine. Low GFR numbers indicate impaired kidney function until proven otherwise. As we get older, GFR naturally falls. You WANT your GFR numbers to be HIGH since that indicates GOOD kidney function.

The Glomerular Filtration Rate is the best overall indicator of kidney function. GFR is not a “measurement”. It is a calculated number based on age, sex, body size, and serum (blood) kidney function values like Creatinine. Low GFR numbers indicate impaired kidney function until proven otherwise. As we get older, GFR naturally falls. You WANT your GFR numbers to be HIGH since that indicates GOOD kidney function. Exercise and insurance exams do not MIX. Exercise raises serum creatinine as muscles work hard and create waste. Exercise can bounce the kidneys (jogging, treadmill, even bicycles) which may cause damage to the kidney’s micro blood vessels and make them “leak” protein. This is not a good thing within 48 hours of insurance exam testing. These are simple preparation instructions for your clients before they take their insurance exam: Hydrate well and don’t exercise. If your client DOES have kidney disease, these actions will have little or no effect on their numbers.

Exercise and insurance exams do not MIX. Exercise raises serum creatinine as muscles work hard and create waste. Exercise can bounce the kidneys (jogging, treadmill, even bicycles) which may cause damage to the kidney’s micro blood vessels and make them “leak” protein. This is not a good thing within 48 hours of insurance exam testing. These are simple preparation instructions for your clients before they take their insurance exam: Hydrate well and don’t exercise. If your client DOES have kidney disease, these actions will have little or no effect on their numbers.

")

")

")

")