")

PLEASE…DRINK THE WATER Or It’s Going to Cost You!

You’ve heard it before. No one drinks enough water! Health experts say we should be drinking at least 6 x 8oz glasses of water every day. Water keeps everything working properly – from moderating your temperature to helping protect your joints to ridding your body of waste; water is integral to our body’s proper functioning. If you aren’t drinking enough water, your organ systems are working too hard!

You’ve heard it before. No one drinks enough water! Health experts say we should be drinking at least 6 x 8oz glasses of water every day. Water keeps everything working properly – from moderating your temperature to helping protect your joints to ridding your body of waste; water is integral to our body’s proper functioning. If you aren’t drinking enough water, your organ systems are working too hard!

Dehydration, Exercise & Underwriting

Just this week AgencyONE has seen 3 cases with insurance labs (urine testing) come into underwriting with LOW Glomerular Filtration Rate (GFR) numbers. This is NOT because of kidney problems, but more likely because of DEHYDRATION or not drinking enough water. A Home Office underwriter cannot dismiss low kidney function numbers assuming they are the result of simple dehydration, so your clients are asked to provide REPEAT URINE TESTING – sometimes on TWO DIFFERENT DAYS just to provide evidence that they are healthy. Low GFR is one of the most common and PREVENTABLE abnormal urine test findings.

What is GFR?

The Glomerular Filtration Rate is the best overall indicator of kidney function. GFR is not a “measurement”. It is a calculated number based on age, sex, body size, and serum (blood) kidney function values like Creatinine. Low GFR numbers indicate impaired kidney function until proven otherwise. As we get older, GFR naturally falls. You WANT your GFR numbers to be HIGH since that indicates GOOD kidney function.

The Glomerular Filtration Rate is the best overall indicator of kidney function. GFR is not a “measurement”. It is a calculated number based on age, sex, body size, and serum (blood) kidney function values like Creatinine. Low GFR numbers indicate impaired kidney function until proven otherwise. As we get older, GFR naturally falls. You WANT your GFR numbers to be HIGH since that indicates GOOD kidney function.

What is Creatinine?

Creatinine is the residual compound or waste that comes from the body’s energy production. Creatinine also measures how well your kidneys are working and plays a role in GFR. The higher your serum creatinine, the lower your GFR number will calculate. What can you AVOID doing that could elevate your serum creatinine levels? You can AVOID EXERCISE. Conversely, what can you do to LOWER your serum creatinine? Don’t exercise and hydrate well by DRINKING MORE WATER!

Exercise and insurance exams do not MIX. Exercise raises serum creatinine as muscles work hard and create waste. Exercise can bounce the kidneys (jogging, treadmill, even bicycles) which may cause damage to the kidney’s micro blood vessels and make them “leak” protein. This is not a good thing within 48 hours of insurance exam testing. These are simple preparation instructions for your clients before they take their insurance exam: Hydrate well and don’t exercise. If your client DOES have kidney disease, these actions will have little or no effect on their numbers.

Exercise and insurance exams do not MIX. Exercise raises serum creatinine as muscles work hard and create waste. Exercise can bounce the kidneys (jogging, treadmill, even bicycles) which may cause damage to the kidney’s micro blood vessels and make them “leak” protein. This is not a good thing within 48 hours of insurance exam testing. These are simple preparation instructions for your clients before they take their insurance exam: Hydrate well and don’t exercise. If your client DOES have kidney disease, these actions will have little or no effect on their numbers.

What is Proteinuria?

It’s a big word but it just means protein in the urine. You shouldn’t have any normally, but exercise-induced proteinuria does happen. A certain amount of protein is not considered pathologic, so thresholds have been established as “normal”. However, exceeding certain levels of protein in the urine will raise red flags in your clients’ underwriting for life insurance protection. Abnormally high levels of protein in the urine will likely result in the underwriter asking for REPEAT URINES possibly on two different days. This is a painful result for everyone if all you needed to do was advise your client NOT TO EXERCISE before their insurance exam. PROTEIN in the urine is one of the most common and PREVENTABLE abnormal urine test findings.

Case Study – Huge Premium Swings

We could write all day about kidney functions, but MONEY TALKS. Let’s take a look at the implications of a client who has NOT prepared for the exam urinalysis through a real-life example.

Mary is a 50-year-old healthy female with no significant medical history. She has an optimal build, takes no medications, and seemingly meets all best-class criteria. She has applied for $5,000,000 of 20-year Term life insurance coverage for family protection. Mary completed her life insurance exam, and the results were all within normal limits EXCEPT that her urinalysis revealed the presence of some protein. Although the proteinuria was mild, it was enough to knock Mary out of consideration for preferred classes, including her application for best class. Standard Non-Tobacco was her best-case scenario with the current urinalysis results. This unexpected turn of events led to a discussion with the advisor about the necessity of thorough exam preparation with all clients.

Mary, unfortunately, did not follow the AgencyONE Exam Prep Sheet or watch the AgencyONE Exam Prep Video we created and that her advisor sent to her. Being the active individual that she is, Mary engaged in multiple HIIT workouts in the days leading up to her exam. She also admitted to not drinking nearly enough water the night before and morning of her insurance exam. Knowing that this was not likely to be a chronic kidney disease case but instead simply poor preparation, AgencyONE recommended Mary repeat her urinalysis with her primary physician. This time around, Mary followed all of our tips for proper exam prep and her urinalysis was completely within normal limits with no proteinuria whatsoever! Given the favorable repeat, we were able to negotiate Mary back to BEST CLASS rates and save her literally THOUSANDS OF DOLLARS!

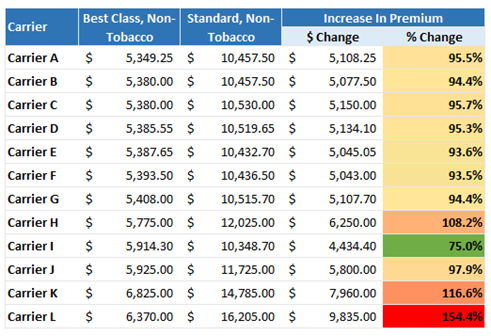

The following table reflects how the top 12 carriers would price Mary’s case (50 yo female, $5M of 20-yr Term) and shows the substantial difference in the premium for a Best Class versus a Standard Non-Tobacco rating.

Bottom Line: Instruct your clients to DRINK MORE WATER and NOT to EXERCISE for 48 hours prior to their Life Insurance exam. INSIST that they prepare for their insurance exams by watching the AgencyONE Exam Prep video. It will help to SAVE SIGNIFICANT time, ELIMINATE potential client FRUSTRATION, and result in a MUCH LOWER life insurance PREMIUM.

AgencyONE’s Underwriters are well-versed in underwriting medical complications and possess deep knowledge on which carriers underwrite and price specific conditions best. We are available to discuss any concerns or issues you and your client might have regarding their underwriting. Please contact the AgencyONE Underwriting Department at 301.803.7500 for more information or to discuss a case!

|

|

")