End of Term Insurance STICKER SHOCK!

Have you ever had a client who came to the end of their level term insurance period and then got a renewal notice that made them happy? More than likely, they were very upset and called you expressing “End of Term Insurance Period STICKER SHOCK!”

LEVEL TERM PREMIUM TO ANNUAL RENEWABLE TERM

Most carriers change from a level term premium during the term guarantee period to an annual renewable term (ART) rate, considering the insured’s attained age at that time. The problem? Since there is no new underwriting upon renewal, the carrier charges rates that are reflective of a much higher risk profile. This higher risk profile translates to possibly a lot more money AND the “End of Term Insurance Period STICKER SHOCK!” The reality of course, is that most clients who are still healthy enough and need continued coverage, (at the advice of their insurance advisor), will not pay the increased premium and WILL subject themselves to underwriting to obtain “freshly underwritten rates” that are more reflective of their health status for another guaranteed term policy. If they are not healthy, and feel they need life insurance coverage going forward, they will exercise their conversion privilege OR continue to pay an ever-increasing premium at the high (ART) rates.

Since there is no new underwriting upon renewal, the carrier charges rates that are reflective of a much higher risk profile. This higher risk profile translates to possibly a lot more money AND the “End of Term Insurance Period STICKER SHOCK!” The reality of course, is that most clients who are still healthy enough and need continued coverage, (at the advice of their insurance advisor), will not pay the increased premium and WILL subject themselves to underwriting to obtain “freshly underwritten rates” that are more reflective of their health status for another guaranteed term policy. If they are not healthy, and feel they need life insurance coverage going forward, they will exercise their conversion privilege OR continue to pay an ever-increasing premium at the high (ART) rates.

SOCIETY OF ACTUARIES STUDY

A May 2021 study, commissioned by the Society of Actuaries from SCOR Global Life USA Reinsurance Company (SCOR), may provide some answers and shed light on many issues affecting the direct writing carriers today. Of note and the purpose of this ONEIdea is that it may explain many of the pricing and conversion option decisions being made as a result of some of the findings and how you can advise your clients.

A May 2021 study, commissioned by the Society of Actuaries from SCOR Global Life USA Reinsurance Company (SCOR), may provide some answers and shed light on many issues affecting the direct writing carriers today. Of note and the purpose of this ONEIdea is that it may explain many of the pricing and conversion option decisions being made as a result of some of the findings and how you can advise your clients.

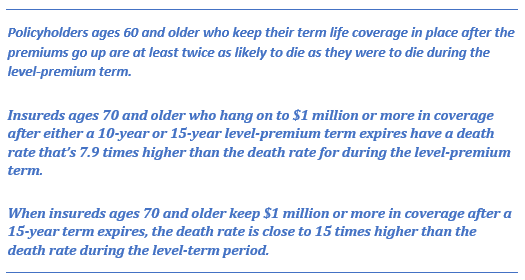

Allison Bell’s June 4th article for Advisor Magazine entitled “When Term Life Policyholders Leave the Level-Premium Bubble” notes two significant statistics from the SCOR study and concludes that “consumers who face a huge premium increase turn out to be good at judging their health”.

Ms. Bell notes that:

Indeed, when a consumer reluctantly pays for “substandard rates on an increasing basis”, they often know the end is near.

A PERSONAL STORY

When my aunt was in hospice some years ago and in her final days of life, it coincided with the expiration of a 20-year term policy that she had purchased. In fact, her 21st year renewal billing statement was sitting in her mailbox when I was visiting her. My uncle asked if he should pay the increased premium, to which I, of course, replied with an emphatic “YES”! The premium was almost 5 times what her level premium had been, but it was the best “investment” my uncle ever made since the company was obliged to pay the death claim a few days later.

statement was sitting in her mailbox when I was visiting her. My uncle asked if he should pay the increased premium, to which I, of course, replied with an emphatic “YES”! The premium was almost 5 times what her level premium had been, but it was the best “investment” my uncle ever made since the company was obliged to pay the death claim a few days later.

TERM CONVERSION PREDICAMENT

This same predicament is being felt by insurance companies, and has been for some time, on conversions. Most clients who know that they are not healthy and can still convert their policies will do so, to avoid the uncertainty of an increasingly burdensome premium requirement at the end of the term period.

Claims experience from many, if not most, insurance companies has not been favorable on term conversions for many of the same reasons….consumers are good at judging their own health and often know something is “not right” with their health.

Claims experience from many, if not most, insurance companies has not been favorable on term conversions for many of the same reasons….consumers are good at judging their own health and often know something is “not right” with their health.

It is no wonder that carriers DO NOT WANT customers to do what the industry calls “late term conversion” and have taken steps to change their conversion period or limit the products available for conversion. More and more we are seeing long term durations limit the years in which a client can convert a policy or, alternatively, limit the product options available to a client for conversion. Most often, the product limitations are very expensive and take into consideration impaired mortality.

In a recent conversation with a carrier who will remained unnamed, I was told point blank that they favored early conversions, but “late term conversions” were a real problem for them.

It is also no wonder why life settlement companies are so interested in buying policies from consumers just prior to the term expiration period and converting them to a permanent policy. Settlement companies are investors, and they are looking for returns – BIG returns. So, much to the insurance company community’s chagrin, it makes sense that life settlement companies are looking for clients who do not want their old term policies and are NOT in good health.

LOOK BEYOND PRICE

Today more than ever, advisors should look beyond price when making recommendations for term insurance to their clients. I cannot tell you how many times I have received telephone calls from advisors asking if I can help them get an exception for a client whose guaranteed term period or conversion privilege has expired, and the client is not in good health, maybe completely uninsurable. The answer is “NO”. Insurance companies know that these cases are claims waiting to happen well before they priced for them.

Term conversion privileges vary greatly from company to company. When making term recommendations, look for the following:

- How long the conversion period is relative to the term period. Most carriers do not allow conversion for the full-term duration, in fact many carriers limit this option rather dramatically.

- Carriers that offer term products that allow conversion to ANY product they offer. Beware of a carrier who offers a conversion period but only allows that the client convert to a “conversion product”. These products are generally priced significantly higher than a fully underwritten product, often as high as 200% more in mortality charges.

- The availability of a conversion extension rider. If a carrier offers this rider, consider recommending it to your client with the understanding that it comes at an additional cost. This will offer your client options should they find themselves in impaired health as they near the end of their term guarantee period.

AgencyONE’s sales support team monitors and tracks carrier conversion data and can help you advise your clients and direct them to the best carriers and products according to their financial and insurance needs.

Please contact AgencyONE’s Marketing Department at 301-803-7500 for more information or to discuss a case.

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the  ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

greater depth of knowledge while ENGAGING your clients in the underwriting process. In this ONE Idea, we are going to take a closer look at what goes into a preferred offer and WHAT AND HOW you need to communicate with your clients.

greater depth of knowledge while ENGAGING your clients in the underwriting process. In this ONE Idea, we are going to take a closer look at what goes into a preferred offer and WHAT AND HOW you need to communicate with your clients. The COVID pandemic has kept a lot of us away from the gym and possibly snacking a bit more than usual, and the result may have been unwanted weight gain. A 10-to-15-pound weight INCREASE can result in a rate class DOWNGRADE! Did you know, for any recent and significant weight LOSS, most carriers will add half of the weight BACK until the weight loss has been maintained for an entire year? Each carrier has MULTIPLE build charts. In addition to preferred build criteria, carriers may have DIFFERENT parameters for males and females, Accelerated Underwriting Programs, Long Term Care Riders, TERM, UL, and Hybrid products. Many carriers underwrite by your Body Mass Index (BMI) which you can

The COVID pandemic has kept a lot of us away from the gym and possibly snacking a bit more than usual, and the result may have been unwanted weight gain. A 10-to-15-pound weight INCREASE can result in a rate class DOWNGRADE! Did you know, for any recent and significant weight LOSS, most carriers will add half of the weight BACK until the weight loss has been maintained for an entire year? Each carrier has MULTIPLE build charts. In addition to preferred build criteria, carriers may have DIFFERENT parameters for males and females, Accelerated Underwriting Programs, Long Term Care Riders, TERM, UL, and Hybrid products. Many carriers underwrite by your Body Mass Index (BMI) which you can  for each carrier, each rate class, the age of the client, and in some cases, if the clients are treated for hypertension. Many carriers will average 12 months of blood pressures to determine your client’s class qualification.

for each carrier, each rate class, the age of the client, and in some cases, if the clients are treated for hypertension. Many carriers will average 12 months of blood pressures to determine your client’s class qualification. If your client used to smoke cigarettes and has quit, it can take anywhere from 1 to 5 YEARS to qualify for a preferred or best class offer depending on the carrier. There are differing parameters around cigars, dip, chew, Nicorette Gum…. even marijuana smoking.

If your client used to smoke cigarettes and has quit, it can take anywhere from 1 to 5 YEARS to qualify for a preferred or best class offer depending on the carrier. There are differing parameters around cigars, dip, chew, Nicorette Gum…. even marijuana smoking. classes if he or she has ONE parent that passed away prior to age 60 to 65 from cancer or heart disease. There are carriers that ignore family cancer histories all together, some that will offset family cardiac histories if the applicant has had certain medical testing, and other carriers that will consider a preferred offer if ONLY ONE parent died before age 60. Some carriers throw these parameters out of risk assessment entirely once the applicant reaches” insurance age” 59, while others never do. The guidelines are “all over the place” with family history!

classes if he or she has ONE parent that passed away prior to age 60 to 65 from cancer or heart disease. There are carriers that ignore family cancer histories all together, some that will offset family cardiac histories if the applicant has had certain medical testing, and other carriers that will consider a preferred offer if ONLY ONE parent died before age 60. Some carriers throw these parameters out of risk assessment entirely once the applicant reaches” insurance age” 59, while others never do. The guidelines are “all over the place” with family history!

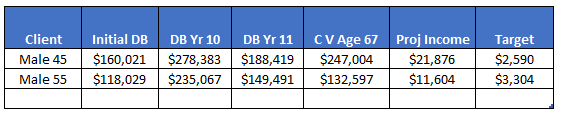

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

a Long-Term Care claim, the applicant must demonstrate an inability to perform two of six activities of daily living (bathing, continence, dressing, eating, toileting, transferring), or have a severe cognitive impairment. As such, when underwriting MORBIDITY, we are looking at conditions that could result in a long-term need for different levels of convalescent care. There is a greater focus on an applicant’s OVERALL state of HEALTH and FUNCTIONALITY, and how it could impact their ability to care for themselves.

a Long-Term Care claim, the applicant must demonstrate an inability to perform two of six activities of daily living (bathing, continence, dressing, eating, toileting, transferring), or have a severe cognitive impairment. As such, when underwriting MORBIDITY, we are looking at conditions that could result in a long-term need for different levels of convalescent care. There is a greater focus on an applicant’s OVERALL state of HEALTH and FUNCTIONALITY, and how it could impact their ability to care for themselves.

is also obese may have a more difficult time controlling his/her blood sugar and cholesterol, is less likely to be exercising, and could be considered a less favorable risk. Underwriters like long-term stability when it comes to ANY chronic condition. When your clients present with comorbid conditions, the “big picture” is scrutinized more closely. Greater attention is paid to the individual’s:

is also obese may have a more difficult time controlling his/her blood sugar and cholesterol, is less likely to be exercising, and could be considered a less favorable risk. Underwriters like long-term stability when it comes to ANY chronic condition. When your clients present with comorbid conditions, the “big picture” is scrutinized more closely. Greater attention is paid to the individual’s:

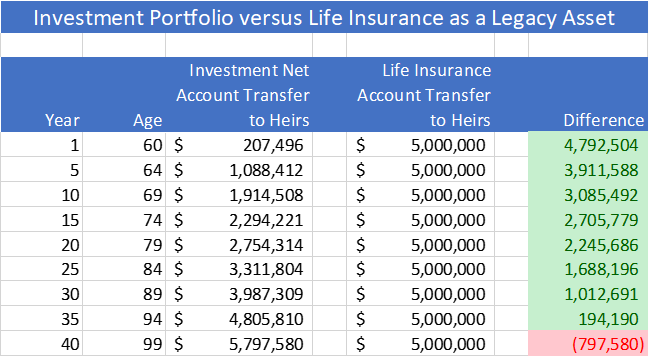

estate if properly owned. Let’s ignore that for just a second.

estate if properly owned. Let’s ignore that for just a second.

CONVERSION OPPORTUNITIES

CONVERSION OPPORTUNITIES

CARRIER PRODUCTS CONSTANTLY CHANGE

CARRIER PRODUCTS CONSTANTLY CHANGE

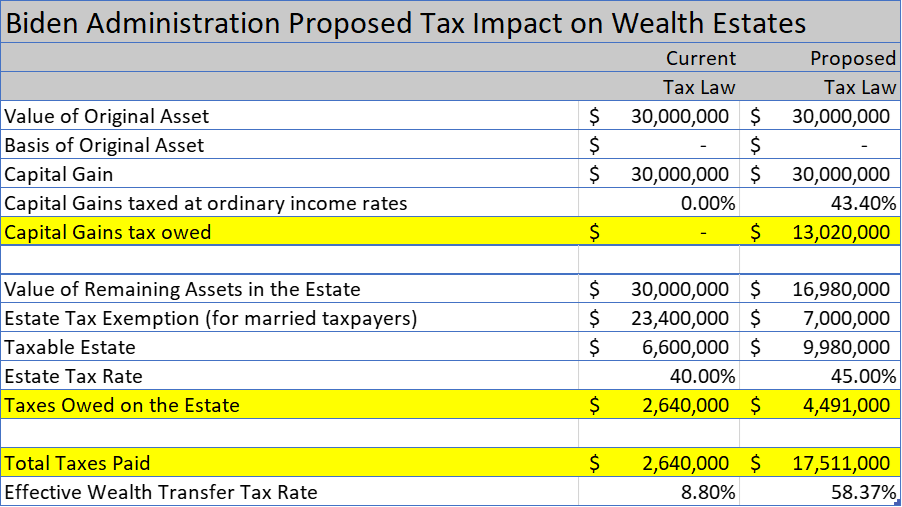

couple) in place and left by the Obama administration (subject to annual cost of living adjustments). The current (2021) limits have increased to $11.7MM per individual and $23.4MM per couple. As a result of these very high limits, less than 1% of U.S. estates are subject to an estate tax. Individual and joint taxpayers can give these amounts over their lifetime to trusts or directly to descendants without a gift tax due.

couple) in place and left by the Obama administration (subject to annual cost of living adjustments). The current (2021) limits have increased to $11.7MM per individual and $23.4MM per couple. As a result of these very high limits, less than 1% of U.S. estates are subject to an estate tax. Individual and joint taxpayers can give these amounts over their lifetime to trusts or directly to descendants without a gift tax due. The simplest estate planning strategy for most wealthy clients, assuming they have other assets available to live on, has been to simply move (gift) large amounts of money (up to $23.4MM) downline generationally (children\grandchildren) or to make gifts to trusts. Life insurance owned by a trust (outside of the client’s taxable estate) has typically been part of the financial equation, depending on the composition of the estate and the need for liquidity or leverage. Additionally, clients can make annual gifts based on the annual exclusion amount per beneficiary of $15K ($30K per couple) without any gift tax due or informational IRS filing requirements.

The simplest estate planning strategy for most wealthy clients, assuming they have other assets available to live on, has been to simply move (gift) large amounts of money (up to $23.4MM) downline generationally (children\grandchildren) or to make gifts to trusts. Life insurance owned by a trust (outside of the client’s taxable estate) has typically been part of the financial equation, depending on the composition of the estate and the need for liquidity or leverage. Additionally, clients can make annual gifts based on the annual exclusion amount per beneficiary of $15K ($30K per couple) without any gift tax due or informational IRS filing requirements. In fact,

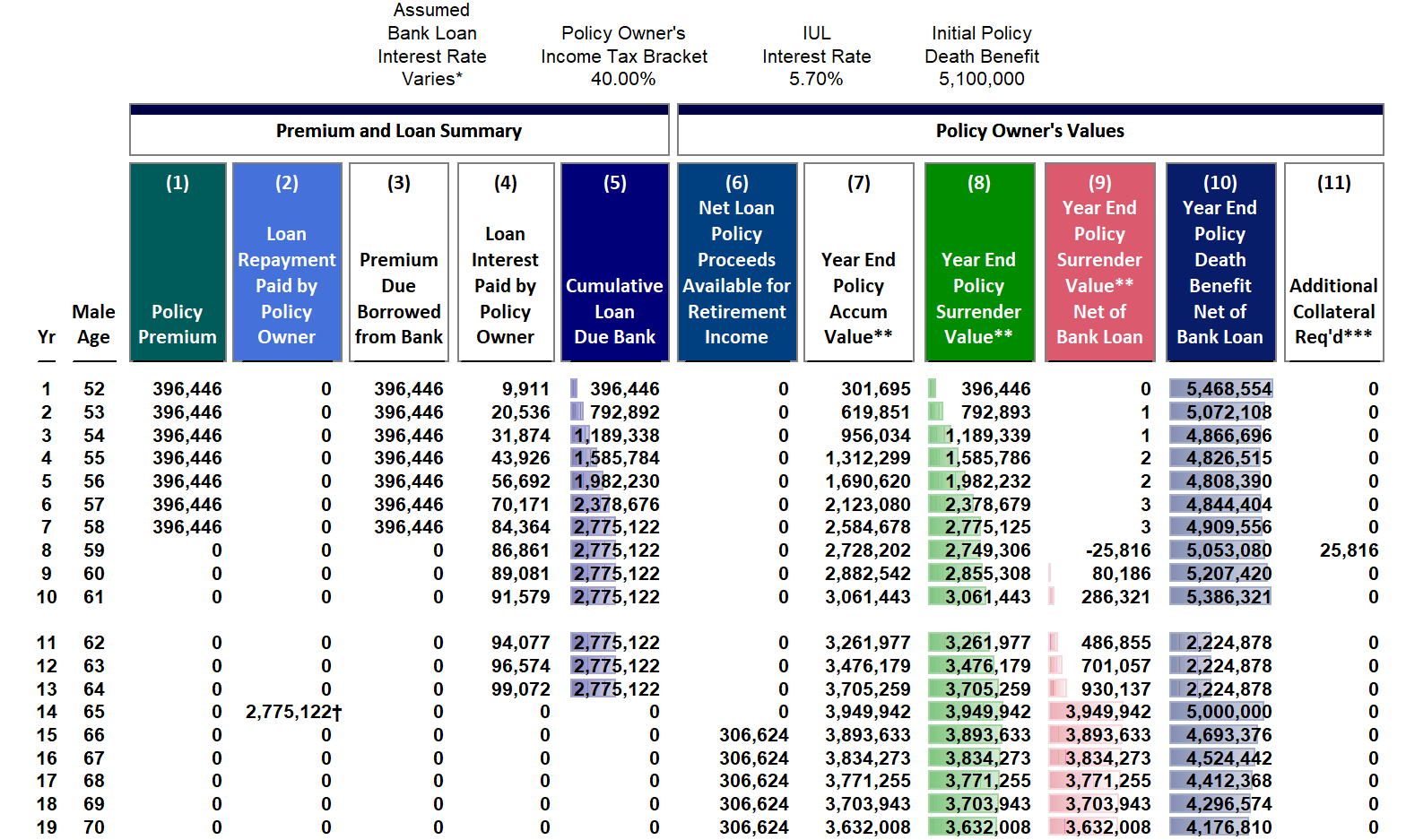

In fact,  This involves banks and other financial institutions that lend money to families or trusts for the acquisition of permanent life insurance to cover estate tax or other liquidity needs. The primary reason for this is if a client’s assets are earning more returns than the cost of financing. This creates a positive spread or arbitrage. Another very important reason to consider is if highly appreciated assets need to be liquidated to pay life insurance premiums. A capital gains tax would be created at the time of sale.

This involves banks and other financial institutions that lend money to families or trusts for the acquisition of permanent life insurance to cover estate tax or other liquidity needs. The primary reason for this is if a client’s assets are earning more returns than the cost of financing. This creates a positive spread or arbitrage. Another very important reason to consider is if highly appreciated assets need to be liquidated to pay life insurance premiums. A capital gains tax would be created at the time of sale. for a short term loan of 3 years or less the prescribed interest rate by the IRS is .12%, for a mid-term loan of 9 years or less the rate is .89%, and for a long-term loan of greater than 9 years the rate is 1.98% (

for a short term loan of 3 years or less the prescribed interest rate by the IRS is .12%, for a mid-term loan of 9 years or less the rate is .89%, and for a long-term loan of greater than 9 years the rate is 1.98% (

The

The

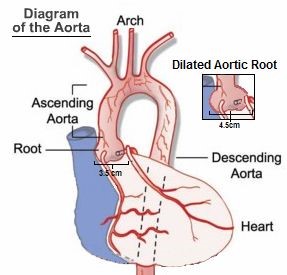

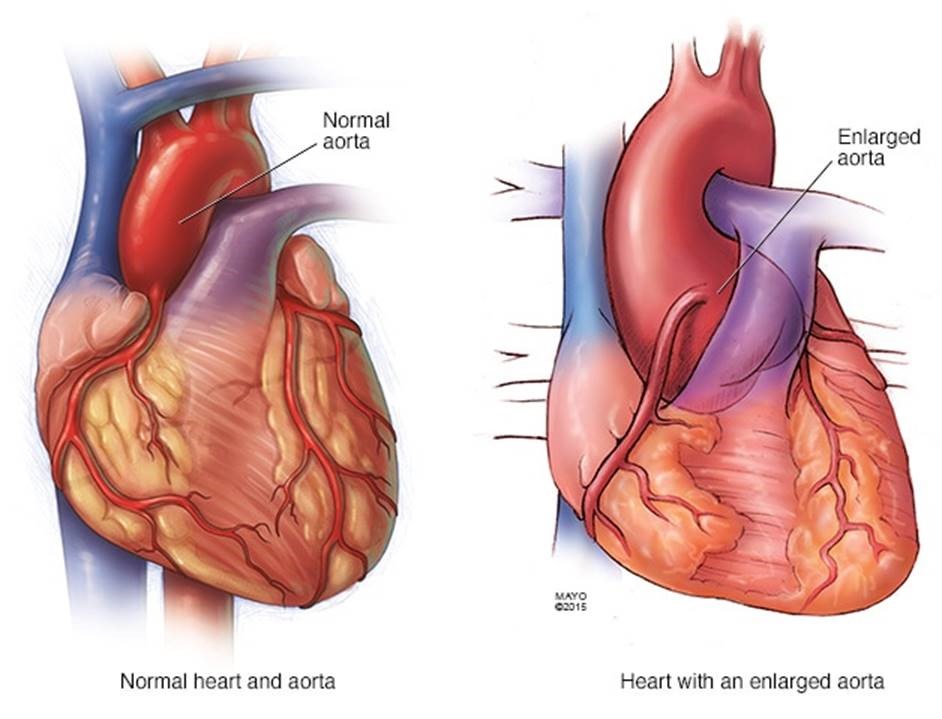

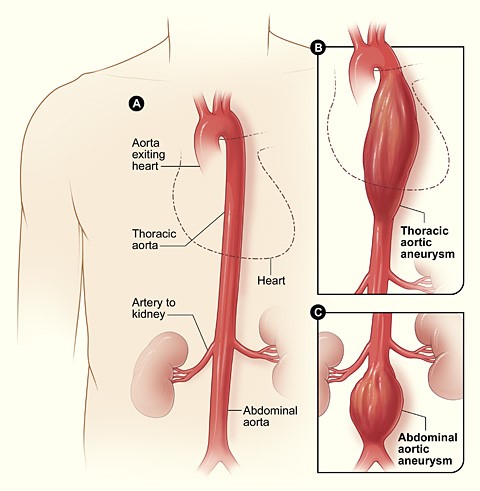

Screening Tests & Aortic Aneurysms

Screening Tests & Aortic Aneurysms

FAMILY-OWNED BUSINESS CASE STUDY

FAMILY-OWNED BUSINESS CASE STUDY