Our Case Design team worked on an interesting case with one of our AgencyONE 100 advisors. It started out very straightforward, but we soon discovered that finding the right life insurance solution for the clients would require drilling down beyond the initial request from the advisor.

Guaranteed Survivorship Solutions

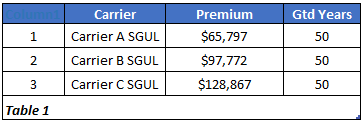

Mr. & Mrs. Smith, both 50 years old, were looking for $10,000,000 of Survivorship Guaranteed Universal Life (SGUL) coverage that would carry them to age 100 and offer full guarantees. AgencyONE presented 3 SGUL options for the clients to consider. Following are the results for this request:

As you can see, Carrier A had the most competitive premium with Carriers B & C coming in significantly higher in cost.

New Survivorship Solutions – Guarantees & Cash Value

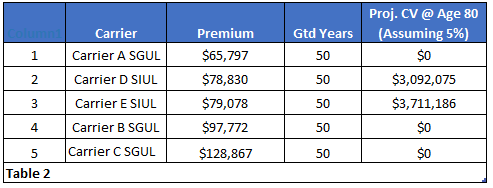

We explained to the advisor that many of the newer survivorship contracts are built on INDEXED chassis which offer GUARANTEES AND projected CASH VALUES that might be of interest to Mr. & Mrs. Smith. Cash value is instrumental when flexibility or an exit strategy is required. However, it is important to note that accessing existing policy cash values will impact the guarantees and possibly hinder long term policy performance. In the next scenario, we added two fully guaranteed Survivor Index Universal Life (SIUL) contracts to the original mix. This offered more options for the clients to consider along with a greater level of flexibility:

Premium To Length Of Guarantee

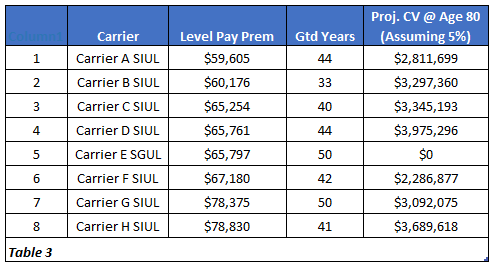

Adding SIUL contracts satisfied the requirement for age 100 guarantees with the bonus of cash values BUT it did not help lower the projected premium. Carrier A’sSGUL premium was still the lowest cost. Including SIUL to the SGUL comparison showed the upside of cash value – which is always a good option to offer clients. Could we show Mr. & Mrs. Smith even more? What could we do to keep a competitive guarantee while also including cash values? The ONLY way to find a lower premium is to forfeit some of the guarantees and rely on cash values to help carry the contract. The key to finding the solution to this case is identifying the right combination of premium-to-length-of-guarantee. After running the solves to age 100, AgencyONE benchmarked the premiums to the guarantee years to see how they compared. The list in Table 3 below shows the NEW top 8 reprice scenarios run to age 100. The IUL assumes a 5% annual return.

Now we are beginning to see a valuable comparison between the cost of the policies, the guarantees, and the cash value benchmarks. If the advisor chooses to go with the SIUL product, we will need to drill down further to see what index options are available and how they will look in ALL years.

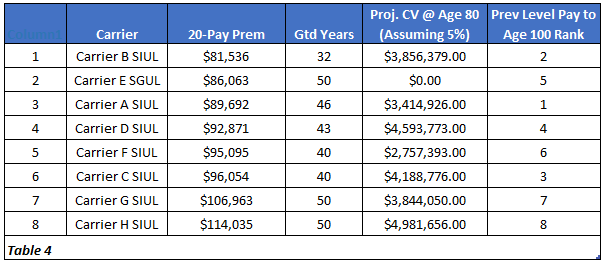

Premium Pay Scenario

In passing, the advisor mentioned that Mr. & Mrs. Smith might just want to pay the premium for 20 years and be done with it. AgencyONE reminded the advisor that the order of the pricing and the length of the guarantee will depend upon the pay scenario. To illustrate, we re-ran the same 8 carriers from Table 3 as a 20-pay scenario to show how the carrier line-up would shift:

As you can see in Table 4, the top carriers moved around quite a bit on premium AND some of the guarantees were impacted. This new order is likely to change which carrier the advisor and clients select to write the coverage.

The advance product design used in this case shows the clients that you possess the ability to understand product nuances, can commit to doing the necessary homework, and, most importantly, are dedicated to their best interests! The AgencyONE Case Design team is committed to making sure that you have ALL the pertinent information so that you and your clients can make the most informed decision relative to obtain the right life insurance their financial and risk management needs.

Most of you are familiar with my personal story but for those of you who are not, please indulge me. This ONEIdea is about insuring minors – yes, “kiddie life insurance”. The press is full of articles about why life insurance for children (a minor child) is a terrible idea, but there are other opinions on this topic such as those expressed in the Forbes article titled Pros and Cons of Life Insurance for Children by Cameron Huddleston and Amy Danise which presents a very balanced and thoughtful commentary.

A Decision By Young Parents

As young parents, my wife and I insured both of our children for $50,000 of Whole Life Insurance shortly after our daughter, the youngest, was born. Our son was about to turn 2. The life insurance was not intended to provide savings with equity type returns, rather it was to hopefully provide a safe and secure investment. The premiums were around $30-$40 per month for each child, which was an affordable investment for us at the time. We also started funding a 529 plan for each child with extra money and hopefully better returns.

A Child’s Unexpected Illness

When our daughter turned 1 she was diagnosed with a benign brain cyst and required a shunt, which is a tube that runs from her brain to her abdominal cavity. Its purpose is to drain the cerebral spinal fluid that is constantly produced by a functioning brain and that is normally naturally flushed. In her case, the natural drainage did not work and left unchecked, the build-up of cerebral spinal fluid caused significant hydrocephalous. At the time, our daughter was not walking, and we did not know if she ever would. The size of the cyst (think of it as a water balloon) was the size of an orange. Her brain (gray) matter was largely non-existent as it had been completely displaced by the cyst. After several surgical procedures and weeks of treatment at Washington, DC’s National Children’s Hospital, our daughter (now 22 months old) finally walked and started doing many of the normal things one would expect of a child that age – a small miracle. Unfortunately, because of scar tissue in her brain from the surgeries or the shunt (it is hard to know), at age 4 she started having seizures and was diagnosed with epilepsy. Our daughter is now 27 years old and continues to suffer from tonic clonic (grand mal) episodes.

My Child’s Life Insurance Today

Now, let’s get back to the life insurance. My wife and I have paid just over $10,000 in premiums at $32 per month for 27 years and the cash value is approximately $15,000, which equals a paltry 2.52% tax free return. However, we really do not care too much about that – it was always “safe money”. The real gain is that, due to paid up additions on my daughter’s policy, the death benefit is now almost $150,000 and will continue to grow as premiums are paid and dividends are earned. While this is not a huge amount of life insurance, I will take an educated guess that it is more coverage than most 27-year-old adults have and more importantly – it is permanent insurance. The insurance is fundamentally “paid up” as the dividends are larger than the premium due each year and the policy should sustain itself or continue to grow (with additional premiums) for the rest of her life. Why is that important?

Complex and Tonic-Clonic Seizures – During the first year since the last seizure, you may be postponed or in some cases be offered standard rates plus an additional 100% markup. In years 2-5 after the last episode, standard rates plus an additional 50% markup will apply. After 5 years, standard rates may be available.

Because our daughter continues to have at least one seizure per year, she will likely be a permanent postpone for additional life insurance coverage unless her seizures stop at some point in the future, and at the very best, she will be highly rated. But the reality is that she may never be able to get life insurance, never mind afford it. Now, for some, that may not be a big deal – she is single, does not have children, has little debt and is fortunate enough to have parents that can help her out. But what about when she wants to get married and have children, and maybe buy a home? There is NO “cheap term insurance” that will solve her problem – she cannot buy it – AT ANY PRICE.

Life Insurance For Children – A Good Decision?

Did my wife and I make a good financial decision? In retrospect, we might have felt that a 2.5% tax free return on an investment of 27 years was downright boring – but it was the best financial decision that we ever made on behalf of our daughter. We do not think of her cashing the policy in for the cash value; we think of the insurance benefit she will be able to leave our (future) grandchildren if something were to happen to her when they needed her the most.

For those of you who are advising young families, or maybe even grandparents who want to help their children and grandchildren, purchasing life insurance for children is a solid financial decision. In today’s crazy, pandemic reality, it has never been more important. You never know when a child will become ill or develop a condition that could impact their life forever.

Life Insurance For Children – Guidelines & Suggestions

With all that said, if you are encouraged to recommend this idea to the right client or prospect – not all insurance companies are child friendly. So, you must do your homework. There are financial underwriting guidelines for insuring minor children that you should be aware of, in addition to medical underwriting guidelines and procedures. Nevertheless, most insurance companies do not require the typical underwriting scrutiny for minors, such as exams and lab work and many will issue policies with very limited underwriting requirements.

Call the AgencyONE underwriting team for clear guidelines on underwriting minors both financially and medically. There are plenty of highly rated and brand recognized insurance companies that offer a variety of products that are very competitive for minors: Mass Mutual, Mutual of Omaha and Securian Financial to name just a few.

And as a final thought, I would like to highlight Securian Financial as a company that issues Preferred underwriting on minors, which is unique in the business. Combined with their Balanced Growth Accumulator Index Universal Life product with a proprietary and low volatility index account, this Securian product is an exceptional choice to recommend for these situations.

AgencyONE is committed to providing product neutral and consumer best interest standards to product and insurance company selection.

“Oops, I did it again…” a song made popular by Britney Spears in 2000 has absolutely NOTHING to do with life insurance protection but focuses on committing the same mistakes over and over. As an advisor to clients seeking life insurance coverage, you HAVE TO ASK THE QUESTIONS – the required medical and non-medical questions over and over again. Failing to procure detailed information – such as marijuana and nondisclosure – limits AgencyONE’s ability to advise accurately and puts your client’s coverage and your sale at RISK.

It Happened Again this Week

The client was NOT asked by his advisor if he uses marijuana. The advisor just ASSUMED that the client did not. While many carriers are NOT testing for THC (the psychoactive compound in marijuana) on insurance exams, they can and will at their discretion.

The case presented to AgencyONE involved a client that was DECLINED for coverage because he was unprepared for the life insurance exam. The decline occurred NOT BECAUSE the client was using marijuana recreationally, BUT BECAUSE HE DID NOT DISCLOSE IT. This carrier tested the urine for THC and the result was obviously positive. This was very bad news for the client AND the advisor.

For the record, recreational marijuana use, up to twice a week, can STILL be underwritten on a PREFERRED NON-SMOKER basis at a handful of carriers.

Insurance companies are combatting fraud every day. When an applicant is not forthcoming with habits, like marijuana use, it ignites suspicion and an underwriter naturally wonders what else is not being disclosed.

This is Not Just About Marijuana Nondisclosure

There’s more to focus on than JUST marijuana and nondisclosure: failing to disclose other pertinent information such as medical histories, doctors’ visits, medical tests, skin checks, colonoscopies, cigar or tobacco use, etc. can cause “hiccups” and significant delays in underwriting. If not admitted to up-front, these nondisclosures may lead to more questions, continued follow-up with clients to obtain additional information, and could potentially require additional medical records causing even further delays. Many times, nondisclosures are unintentional or simply an oversight by the client. Therefore, it is imperative that you thoroughly explain the underwriting process and impress upon your clients the importance of providing full details.

As professional insurance advisors, it is important from a LEGAL perspective that you ASK and thoroughly address ALL questions on insurance applications. If your client is completing a telephone interview or filling out a digital application, he/she needs to understand the importance of providing accurate, complete responses. This information becomes part of the LEGAL CONTRACT with the carrier. A nondisclosure is VERY LIKELY to be discovered by the carrier given the wealth of electronic tools and database information underwriters have at their disposal today such as:

Prescription Database Verification Reports

Medical Claims Information

MIB and Insurance Activity Index

AgencyONE Has the Tools to Help!

AgencyONE has created a library of tools to help you and your clients. Our email taglines now include 5 ICONS with hyperlinks that open various tools designed to assist with the entire underwriting process:

Video: Preparing for the Life Insurance Exam

This video advises clients how to prepare for and what to expect during the insurance exam, including questions the examiner will ask…example: about marijuana and tobacco use!

AgencyONE Informal Inquiry and HIPAA Packet

Complete this form to provide AgencyONE’s underwriters with the pertinent medical and non-medical information needed to advise on case direction. The packet includes additional exam-prep tips and instructions on how to retrieve the insurance exam LAB results.

NEW* Video: Interview Prep

This video is perfect to advise your clients on whow to prepare for and what to expect during the Telephone or Digital Interviews. The corresponding worksheet can be found on our website www.agencyone.net under the underwriting tab.

Video: Preparing for the Senior Supplement

This video explains what to expect during the senior supplement portion of the insurance exam. While some of the questions and activities may seem trivial, the results can have a great impact on insurability. The process MUST be taken seriously and preparing your clients is imperative.

Simply share the necessary linked icon(s) or the entire series with ALL your clients, and please visit our website for additional resources.

We urge you to make these AgencyONE tools an integral part of all your client preparations. You WILL notice a difference (in a positive way) on the underwriting process!

AgencyONE has the underwriting knowledge and necessary resources to help you present a thorough and well-planned case to the carrier best suited to your clients’ needs.

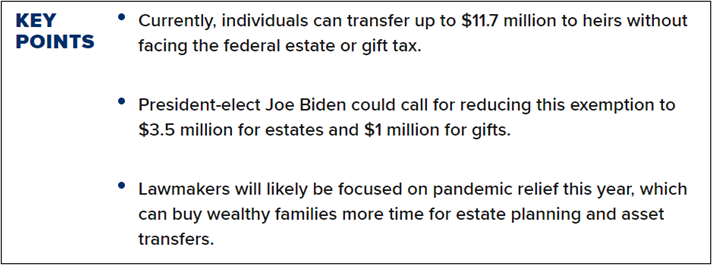

There are many wealthy clients that know that the window to make substantial gifts, and thereby reduce their estate tax liability, is closing due to proposed changes in the estate and gifts tax regimes. In fact, those in estate planning circles having been discussing this for months. There is a simple solution to the Estate and Gift Tax quandary that your wealthy clients need to know. Before we explore the solution, let’s look at the reasons taxpayers may not have acted in 2020:

Their attorney was too busy doing the same planning work for other clients and could not get to them before year end;

They did not believe that Joe Biden would win the election;

They thought that there would be a divided Congress and there would be continued gridlock in Washington; or

They simply kicked the can down the road for some other reason.

The Estate & Gift Tax Quandary

The BIG quandary now, for those taxpayers that did not take action, is that if meaningful gifts are made in 2021, will the law be retroactive to January 1, 2021, potentially causing a massive gift tax due in 2022? In the linked article by Bob Dietz and Tom Pauloski titled Could a Change to the Gift and Estate Tax Exclusion Be Retroactive, the authors discuss this problem. They address the issue of a change in the Basic Exclusion Amount going from the current level of $11.7MM per taxpayer down to $3.5MM per taxpayer under the Biden Proposal. What they do not mention however, as it relates specifically to the gift tax exclusion, is that under the proposal the Biden administration would de-couple the estate and gift tax regimes and REDUCE the Gift Tax Exemption to $1.0MM, while the Estate Tax Exemption would be REDUCED to $3.5MM. This of course would cause a bigger gift tax problem still. See CNBC article dated January 22, 2021 titled Here’s How Wealthy Families Will Save on Estate Taxes in the Biden Presidency.

We Have A Solution

To provide the intended result of gifting over $1MM without the risk of being subjected to a gift tax should the law become retroactive to January 1, 2021; we have a solution.

With the current Biden tax proposal being a reduction in the gift tax exemption to $1 million with an estate tax exemption of $3.5 million it seems as though prudent planning would be to make immediate gifts to take advantage of the current $11.7 million gift tax exemption. However, with even the possibility of such a tax bill being retroactive, as unlikely as many advisors consider that possibility, is it wise to pursue that course of action?

To Gift or Not

Imagine the following scenario: A taxpayer makes a gift of $3,500,000 to a trust in March of 2021. The “Biden Tax Act” is passed sometime later in 2021 and is made retroactive to January 1, 2021 with a $1MM gift tax exemption. The taxpayer\grantor is now in a situation of potentially having to pay $1,000,000 in gift taxes on the difference between the $1,000,000 gift exemption and the $3,500,000 gift made. ($3,500,000 – $1,000,000 = $2,500,000 at a 40% gift tax rate equals $1,000,000 gift tax).

Of course, on the other hand, not making gifts in the current environment will almost certainly be a wasted planning opportunity. Why? Because it is difficult to imagine that a tax bill lowering the exemptions to at least the $5 million (with indexing to about $5.9 million) level is not a near certainty before the 2022 elections when a closely divided Congress could once again change hands, thereby making tax legislation for the Biden Administration much more difficult.

What To Tell Your Client

So, what should a prudent advisor tell his or her affluent clients? Well, for affluent clients, it seems clear that making a gift of $1 million is safe. A husband and wife, age 60 and 55, can purchase about $5 million of second to die insurance for $1 million. That is very powerful leverage!

However, what about those clients with very large estates – a simple $1 million gift strategy will do little to reduce the estate tax exposure and create liquidity for payment of taxes. What the possibility of a retroactive tax bill is likely to do is slow down the planning for those clients that really should be planning. When Congress eventually does get taxes on the table – it could happen quickly. In fact, many in Washington feel like a tax increase could be tacked onto another bill to offset costs for purposes of avoiding filibuster in the Senate. Could a tax bill be tacked onto an infrastructure bill?

Take Action Now

Whether the tax bill that is surely coming down the pike is retroactive or NOT, one thing is certain. Your clients should take action NOW, because they risk either not having time to do planning before a retroactive tax bill takes effect or suffering the effects of a new tax bill again, without having the appropriate planning in place. And the action that your client can take NOW is to get his/her plan teed up via loan strategies. Let’s look at a case study.

Estate & Gift Tax Planning Using Loan Strategies

Maggie May is 75 years old. She is recently widowed. Maggie and her husband were successful real estate developers. She has a mostly illiquid estate valued at approximately $40 million. The properties are growing at about 8% a year, including cash flow of about $2 million. Maggie’s estate planning attorney has suggested that her real estate holdings be transferred into one or more limited liability companies (LLCs). These LLCs would restrict transfer in such a way that her attorney suspects a valuation firm will discount minority ownership interests by about 40%. The attorney is then suggesting that Maggie sell a substantial portion of these interests to an irrevocable trust that is ignored for income tax purposes (what some people might unfortunately call an “IDIT” or “defective trust”). If Maggie transfers her property into LLCs and gets a qualified appraisal with a 40% discount – she will have reduced the value of her estate considerably. For the sake of discussion, we can now assume the value of the estate for estate tax purposes would be about $24 million.

Gift, Sale, Cash for Life Insurance

If Maggie makes a $1 million gift to her LLC and then sells another $9 million of this property to her trust, she will have reduced her taxable estate to $14 million. Her cash flow from the retained assets would still be $1.167 million in year one and increasing. The sale of the LLC interests would be at the current Applicable Federal Rate (AFR) which is 1.6% — generating another $144,000 in potential cash flow to Maggie (if needed). But, even after the trust pays interest (which is not income taxable) to Maggie, it will have cash flow of about $689,500 (5% of the underlying trust assets valued at $16.67 million before transfer to the LLC and discounted less the $144,000 loan interest). This cash flow within the trust could be used to purchase life insurance on Maggie’s life. Depending on the product and underwriting class – $689,500 could purchase about $17,500,000 of death benefit on a tax-free basis outside of Maggie’s estate. And, by potentially using a premium financing strategy to reduce out of pocket cost, additional leverage could be created and additional insurance purchased by the trust.

Importance of Pre-Planning

If the gift and estate tax exemptions are not reduced, at some point Maggie could forgive the note and use her lifetime exemption. But, most importantly, this will be especially important if legislation is introduced that is not retroactive but has a very short window. What is more likely than retroactive legislation is a tax bill that becomes effective immediately upon passage. And, if tax law is added to other legislation as part of reconciliation, this window would be only days. Having the property already in the LLC, appraised and transferred to the irrevocable trust, puts Maggie and her advisor in a position where they can literally complete the gift immediately by simply forgiving the note from the trust to Maggie. Those clients that wait until they see the introduction of what is likely a certain tax bill will be in a queue with their advisors that will very possibly prevent them from meeting what could be a very short timeline.

Interest Rates & Trusts

With today’s low interest rates, selling assets out of a taxable estate and into an irrevocable trust outside of the estate tax is prudent planning! If a client can earn even a modest return on the assets sold, the client and their family will be able to move the appreciation out of the estate tax system. With a 1.6% AFR – assets earning 6.6% will grow by 5% (after loan interest payment) outside of the estate. The trust can use this appreciation to purchase life insurance or to reinvest. But, given the uncertain tax environment we find ourselves in today, this type of planning seems an almost necessity for affluent clients.

As mentioned in the beginning of this article, many wealthy individuals and families had intentions of taking advantage of the incredible opportunity to move assets out of their estates in 2020 but did not, or could not, act. The environment has changed adding some risk that was not there prior to a Democratically controlled White House and Congress. Flexibility and nimbleness IS the name of the game today.

Life insurance products and underwriting requirements have undergone tremendous changes in the last year (2020-2021) and historically low interest rates and COVID-19 have played a primary role. Every other week it seems we are getting another notice about a price increase, a product discontinuation, or an underwriting modification. It can be very confusing and has some asking, “what is left to sell”? The answer? There is still a wealth of life insurance product options available for your clients AND there are multiple carriers offering each.

In this ONEIdea, we are going to breakdown general characteristics according to product type. We will not discuss top pricing or carriers since these are based on age, underwriting class, and face amount. Please note that some of the products available may be different in New York.

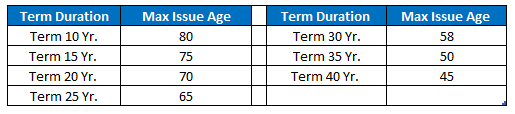

Term Insurance

Our carrier partners offer a variety of individual Term options. When running a Term comparison, it is important to carefully consider all options and look beyond just the spreadsheet cost to find the appropriate product for your client. Following are important things to consider:

ease of application (E-apps);

possible accelerated underwriting options; and

available riders and future conversion options.

By looking beyond the lowest cost, you may find something that offers more options for your client to consider for a minimal increase in premium. The table below lists the max issue ages for each term duration (NY carriers may not have the same issue ages or product durations).

Current Assumption Universal Life

Current Assumption UL (CAUL) is a product that is primarily death benefit focused. Lower crediting rates have diminished the product’s competitiveness for cash value accumulation sales. Death benefit products use crediting rates set by the carrier which can be modified monthly. One of the benefits AgencyONE sees with these contracts is that they are typically built with longer LE type guarantees. A few of these products offer LTC or Chronic riders that can add important coverage for the client. While CAUL has been a common option in the past, currently only 5 of our carrier partners offer this product. One carrier’s product has an issue age up to 89, assuming the client qualifies, and one offers a Current Assumption Survivorship (CASUL) option.

Guaranteed Universal Life

Guaranteed UL (GUL) has been extremely popular over the last 20 years. AgencyONE has seen carriers go from offering multiple versions of GUL products to pulling the product line all together. Given the current market you may be thinking GUL is no longer an option for your clients. Fortunately, 8 of our carrier partners still offer Guaranteed UL products (these do not count VUL or IUL products with lifetime guarantees). These GUL options can guarantee coverage up to age 121. They can also be run with shorter guarantee periods, short pay designs and some even have refund options. If you are considering a survivorship GUL option, 3 of those 8 carriers offer joint GUL coverage.

Indexed Universal Life

The most popular product type in the marketplace is Indexed Universal Life (IUL). When IUL was first introduced, the product was primarily designed for cash accumulation with limited guarantees. Over time, carriers broke up their product lines into two types:

Accumulation IUL which worked best with minimum non mec face amounts and max funded premiums

Death benefit IUL products that had a set level death benefit and used solved premiums usually to age 100 or 121

These products also had longer guarantees and, in some cases, could be guaranteed up to lifetime. Many carriers have also introduced an Indexed SIUL product. A few of these are very competitive in price and can also be guaranteed to age 121! The “best” product for your case depends on the funding period, goal, and riders needed.

Whole Life

AgencyONE has seen quite a few requests for whole life recently. This product is still strong and offers many guaranteed pay options. The guaranteed cash values can be attractive to clients who are more conservative. Many of our carrier partners (some are still Mutual) offer strong Whole Life products with various pay options: 10-pay, 12-pay, 15-pay, 20-pay, pay to 65, level-pay to age 100, and level pay to age 121.

Variable Life

Variable Universal Life (VUL) insurance continues to be popular with our agents and their clients. There are two types of variable products that are currently available in the marketplace. One version can be used to accumulate cash value. These accumulation VUL’s are used on younger clients and are meant to grow cash value for future income needs. The newer accumulation VUL products include indexed account options which may be beneficial during the income years. The second version is a Guaranteed VUL product. This option provides a guarantee up to lifetime and the option to accumulate cash value (if the expected performance is achieved). The guaranteed versions work well with 1035’s and short pay designs. There are also a few Survivorship VUL contracts to consider and two of them can be guaranteed, if necessary.

Hybrid LTC Products

Hybrids LTCs are great options to consider and compare to stand alone LTC products. While they have limited funding options (1 pay, 5 pay, pay to 65, and at some ages, a life pay is available), they can be written up to age 75. One of our carrier partners also offers a joint product for two lives with a lifetime benefit period.

As you can see, there are still a variety of available products to suit almost any case scenario. The many riders and product features can help enhance and customize the product design for your clients.

AgencyONE’s Case Design Department is known for its product intelligence, diligently monitoring product changes and updates, and being readily available to help you answer specific questions and find the most appropriate product to meet your clients’ financial and insurance needs.

Let us start with the obvious – he or she would NOT consider No Load/ Low Load VULs because without a FINRA registration and a Broker Dealer, the Fee Only RIA is not licensed to sell a VUL – it is, after-all, a registered product. With a Fee Based or “Hybrid” Advisor, that is a different conversation and I will discuss this later.

WHAT IF I TOLD YOU THAT YOU COULD RECOMMEND A VUL?

AND what if I told you that you could construct the portfolio (within the available fund options), manage the portfolio, aggregate values for reporting purposes AND continue to charge your client per your customary fee agreement (whether you are Fee Only or Fee Based), all the while eliminating taxes on reinvested dividends and capital gains for the life of the client? What if I also told you that you could add Alpha to your client’s Variable Universal Life policy portfolio? And finally, what if I told you that existing life insurance policy cash values (of any kind), not managed by you, could be brought into your AUM via a tax-free transfer while preserving the cost basis? Does this sound impossible? Please keep reading.

The immediate objection to Variable Universal Life from a Registered Investment Advisor’s perspective is that those assets (the cash value) fall outside of the control of the RIA. If it cannot be reported in the aggregate statement, it may not be considered part of the AUM fee agreement. Which means that the fee, let’s call it 1%, cannot be billed to the client. We have solved that problem.

ISN’T LIFE INSURANCE IS TOO EXPENSIVE?

The next objection is that life insurance is expensive – that it has too high of an expense drag. Let me do the math for you because that could not be further from the truth. In fact, in a managed portfolio, I hope that you will agree that the largest expense to a client’s portfolio is taxes on reinvested dividends and capital gains, not always fund management expenses, even if you only invest in a low-cost index fund such as an S&P Index (Vanguard as an example, has a .04% expense ratio). Clearly, in an actively managed or traded portfolio, the tax bite could be even greater due to capital gains, but so are the management fees.

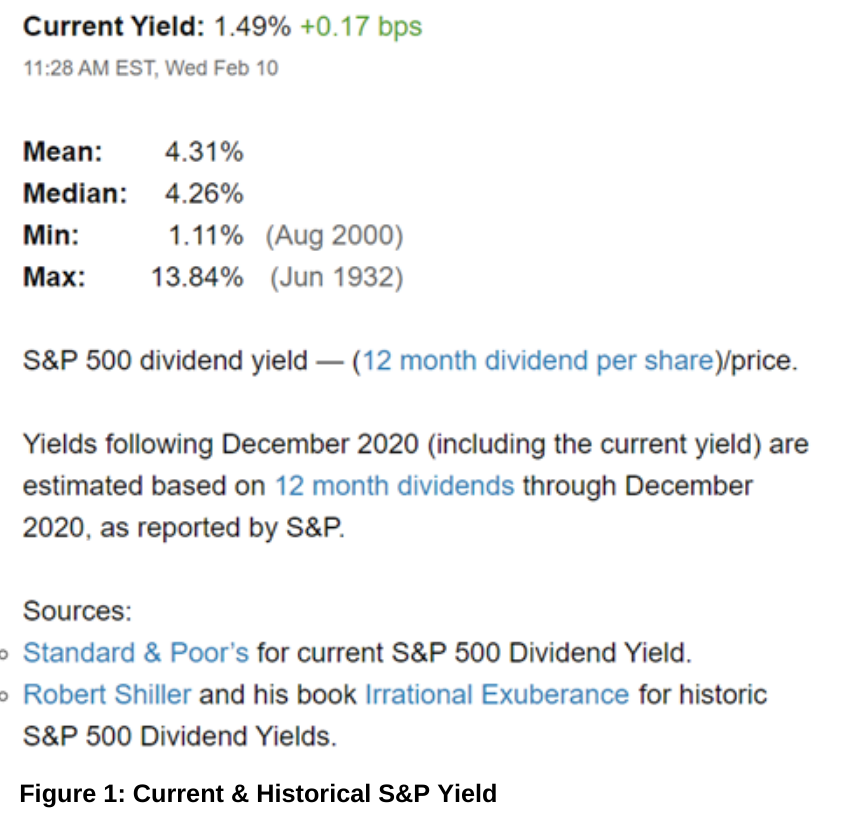

Dividends are generally taxed at ordinary income tax rates that can be as high as 37% for federal taxes in 2021 under current law plus any applicable state taxes.

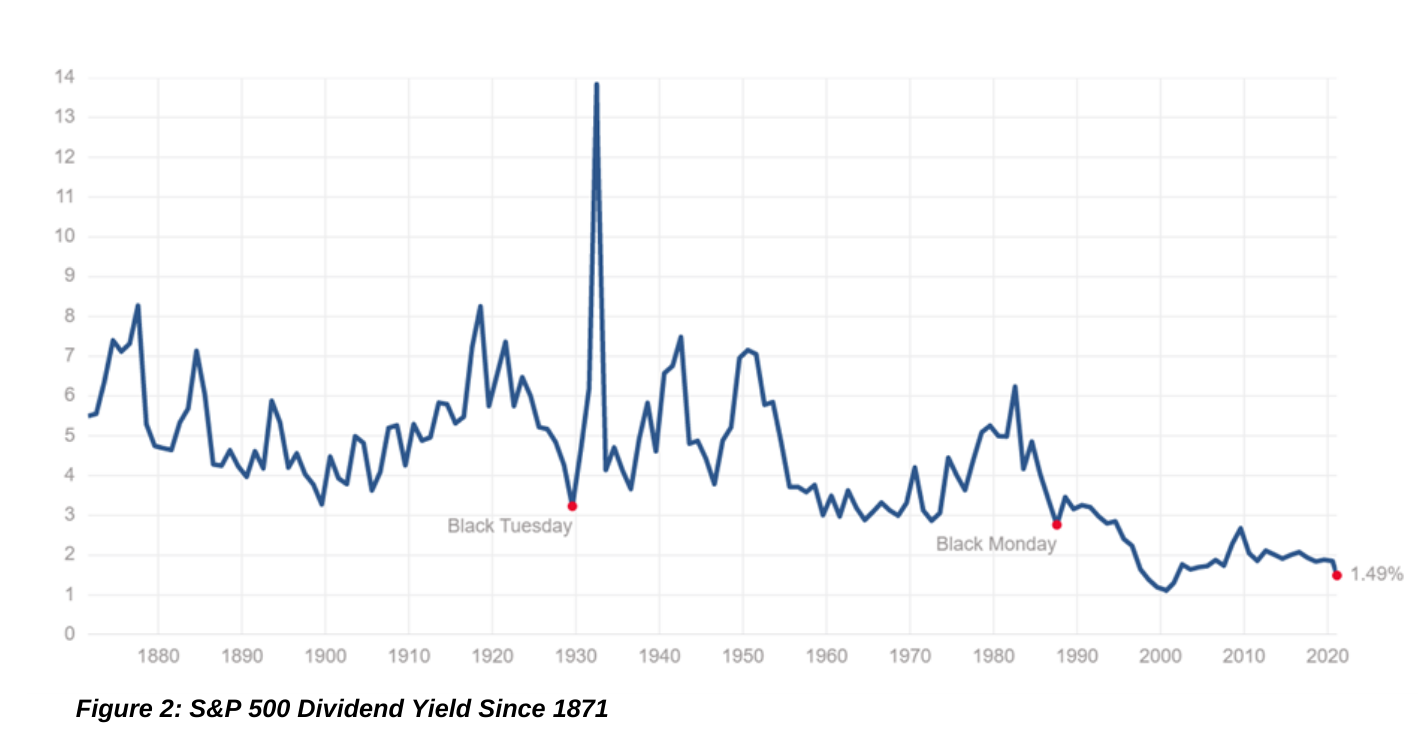

The S&P Index Yield, from 1871 to 2020, has averaged (mean) 4.31% with a median of 4.26%. As of the date of this writing, it is currently yielding around 1.5%, which is historically low.

So, for example, on a $1,000,000 account balance for a high income\high net worth client, in an S&P 500 Index account, the historical average dividend would be $43,100 and at a 35% tax rate “the cost” is just under $15,100 in taxes. Then add the .04% fund level fee of $400 at Vanguard for a total of 1.55% or $15,500. If you then add a fee for the advisor, suddenly it gets very expensive to own a Vanguard Index Fund. Take a zero off the account balance and the math works just the same.

If you move into a more actively managed account that generates meaningful capital gains taxed at 20% for federal tax purposes (but the tax could be almost double depending on whether they are short term or long-term capital gains) and may also be subject to state taxes, the dynamics change even further. You get it.

Objection number two has been solved. Life insurance is NOT expensive compared to a non-qualified investment account. BUT WHAT ABOUT THE INSURANCE COSTS? More on this shortly – I promise.

VARIABLE LIFE INSURANCE POLICIES PROVIDE A “TAX WRAPPER”

Fundamentally, any dividends and capital gains are protected from taxation to the owner of the policy much like in a qualified plan (401K, IRA or Roth), taking the cost of taxes out of the equation. Furthermore, life insurance enjoys a special regulatory tax treatment under the law during the distribution phase in that it allows the policy owner to take basis (sum of premiums\contributions invested in the policy) from the policy FIRST, and then borrow any gains from the policy TAX FREE. Finally, should the client die, the death benefit is paid INCOME TAX FREE without regard to basis – in effect, a guaranteed step up in basis. Double finally, if the client is in a wealth transfer tax (yes, “death tax”) situation, properly structured, the death benefit can be free of any estate taxes.

Let me say that again …. the policy owner enjoys:

Tax free dividends

No taxes due on capital gains

First in, first out (FIFO) taxation treatment\ access to the account values

Income tax free loans at a very low or no cost

No pre-59 ½ penalties on withdrawals

A guaranteed step up in basis, not on the account value but on the death benefit at death

Possible exclusion from wealth transfer taxes.

I don’t know about you, but that sounds fairly attractive to me.

THE COST OF LIFE INSURANCE & AGENT/ REGISTERED REPRESENTATIVE COMMISSIONS

Now, let’s discuss the big white elephant in the room – the cost of the life insurance AND agent\ registered representative commissions.

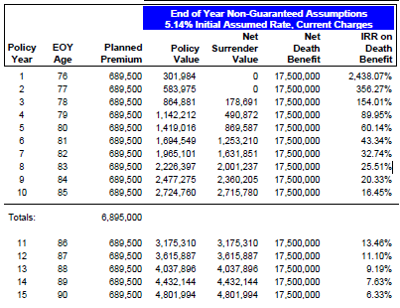

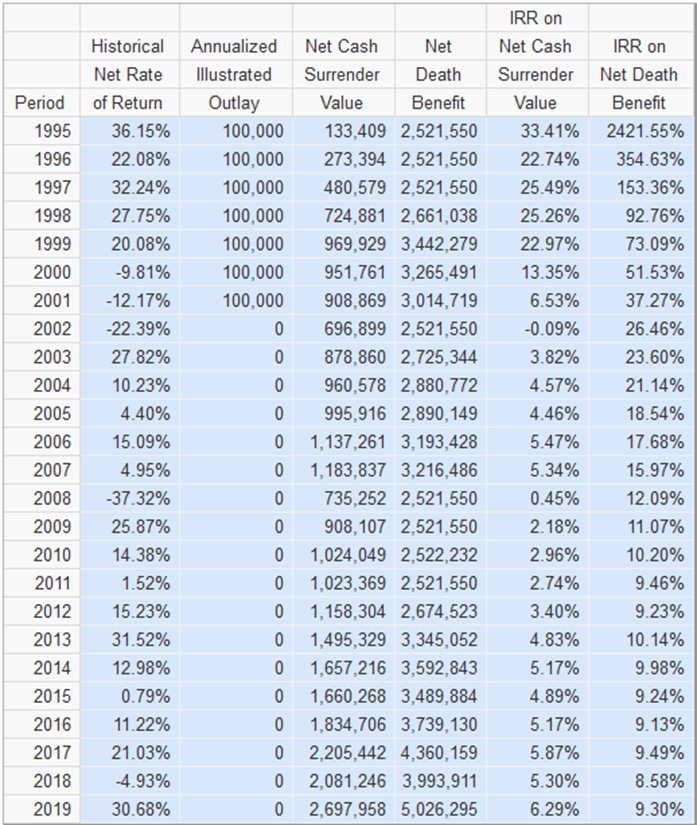

I have prepared a variable life illustration and have shown the historical performance of the policy assuming that it had been invested in the S&P Index Sub-Account of this policy since 1995 through the end of 2019. Notice the first-year cash surrender value and how it does not reflect any surrender charges and captures almost the full amount of the return of the S&P in that year.

The illustrated policy is for a 45-year-old male, healthy non-tobacco user and is designed for maximum accumulation and minimum cost of insurance to avoid becoming a Modified Endowment Contract; thereby maintaining its favorable tax status.

The objective of the policy design is to maximize efficiency within the constraints of the tax law and to minimize expense drag.

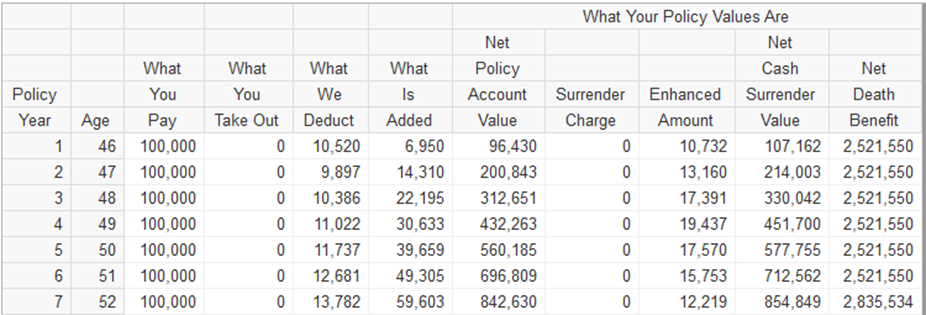

In the table below, I have added a summary expense page (a detailed one is also available and is also disclosed in the full illustration). Clearly there are deductions; it is life insurance first and foremost. In the “What We Deduct” column, these charges are for premium taxes, administrative charges, cost of insurance and any riders, acquisition costs, and underwriting costs. There is also an “Enhanced Amount” column that fundamentally reimburses the client for these charges should they surrender the contract and is added back to the Net Cash Surrender Value. The column titled “What is Added” shows the illustrated returns net of any sub-account expenses, and as previously mentioned are not taxable annually to the client, and potentially are NEVER taxable.

A SPECIAL VARIABLE UNIVERSAL LIFE PRODUCT

The product that I am introducing to you can be designed with ZERO agent commissions. It does, however, pay a modest wholesale dealer concession to a Broker Dealer of the designated registered representative. A registered representative is required to sell a Variable Universal Life policy. AgencyONE has a wholesale broker dealer who has agreed to register these accounts and allow our registered principal, who is also insurance licensed, to act as the servicing agent. AgencyONE also has a network of insurance advisors who can act in this capacity nationally if you so choose. AgencyONE, and its licensed representatives, does not manage money and we would be required to sign non-solicitation and non-circumvention agreements with the referring Investment Advisor.

If you are an advisor who accepts securities commissions through your broker dealer, the product has the flexibility to accommodate this scenario, with comparable efficiencies. All that would be needed is for your broker dealer to have a selling agreement with the insurance company.

I mentioned at the beginning of this article that fee-only advisors do not have the ability (nor the desire) to receive commissions on securities. There are products in the market, such as the one illustrated, that DO NOT pay a commission to the advisor. These products, however, allow the advisor to treat life insurance cash value as any other asset in a client’s portfolio and provide advisory services and charge a fee for doing so.

A Variable Universal Life policy prior to today was often a “set it and forget it” asset. Many registered representatives who are also licensed to sell insurance would establish an initial asset allocation strategy for the VUL portfolio and rarely manage them, often leaving clients to their own worst tendencies. Additionally, I cannot tell you how many VUL policies I have reviewed that after years of being issued, the portfolio was still in the fixed account or the money market equivalent account. Why and how did this happen? Because it was set up as a holding place for the investment until the portfolio could be determined …. and it never was. A Registered Investment Advisor can add tremendous value to a client’s tax deferred (cash value) portfolio.

As a financial advisor to your clients, it would be your responsibility to establish the portfolio allocation, manage it, report on it and aggregate values in the overall portfolio that you manage for your clients. Technology has been built to allow daily values reporting through a portal, much like you would find in a qualified plan offering or on any other technology platform with which you may be familiar.

This institutionally priced Variable Universal Life product does have some minimums, but unlike Private Placement Variable Life, it is generally available to most mass affluent or high net worth clients. The important issue is that YOU are in control of the asset and YOU are in control of the client.

Want to learn more? Do you have a case that you would like to discuss? Contact AgencyONE’s Marketing Department at (301) 803-7500.

In 2015, John Hancock introduced VITALITY – the industry’s first revolutionary post-issue program which allowed their policy holders to earn rewards for staying healthy. In 2019, they added the ASPIRE platform, which is specifically designed for individuals living with diabetes. ASPIRE for diabetic clients has become a great way to stay connected with customers, support wellness, and reward healthy habits with PREMIUM SAVINGS, and has become even more relevant in the wake of the COVID 19 pandemic.

Diabetes & Covid

Individuals living with diabetes are some of the most vulnerable IF they have been infected with COVID-19. In large part, the insurance industry has responded to heightened mortality and morbidity concerns by implementing strict underwriting guidelines, limiting “credits” for good diabetic management (which equates to cost savings) and postponing coverage for some clients who fall into higher rating classes altogether.

For clients living with diabetes, this is arguably the most important time to secure life insurance protection. ASPIRE makes insuring your diabetic, health-conscious clients MORE AFFORDABLE.

ASPIRE Program Details

John Hancock WANTS TO INSURE your diabetic clients! The ASPIRE for diabetic clients platform personalizes the post-issue journey for clients living with diabetes and provides a point system tailored to this health condition. Clients will receive updates on the latest diabetic treatment. John Hancock has also teamed with the company Onduo which provides individuals living with Type 2 diabetes DAILY support in managing their unique healthcare needs through blood glucose monitoring, online tools and coaching from nutritionists and medical professionals. While this DOES NOT replace traditional medical care, it DOES offer clients meaningful guidance and accountability in between doctors’ appointments. ASPIRE also offers a custom pathway in which clients can accrue points and be REWARDED with up to 25% in PREMIUM SAVINGS and more!

How Your Clients Can Save In Premiums with Vitality

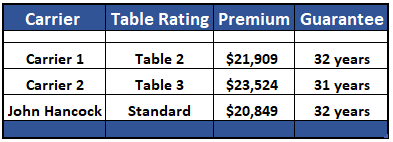

Mr. Jones is a 48-year-old, non-smoking male diagnosed with type 2 diabetes who is treated with oral medications. He has been taking his medications regularly, monitoring his diet, and his A1C levels have remained between 6.8% and 7.0%. He has no noted complications, exercises several times per week, and his build is favorable.

The client’s younger age is the main issue in this scenario. In theory, Mr. Jones has more time for complications to develop so many carriers will start with a Table 2 to 3 rating. He is applying for an IUL policy with a $2MM death benefit run as a lifetime solve assuming a 5% interest rate.

John Hancock’s competitive underwriting offer and strong guarantees make them the clear winner in this case. BUT, Mr. Jones can SAVE EVEN MORE on the $20,849 annual premium if he also participates in John Hancock’s Vitality Plus program. Depending on which John Hancock Vitality level he achieves, the savings can be very meaningful throughout the life of the policy:

Vitality Silver Level: $20,151 annual premium payment for all years – $698 savings per year

Vitality Gold Level: $18,717 annual premium payment for all years – $2,132 savings per year

Vitality Platinum Level: $18,317 annual premium payment for all years – $2,532 savings per year

Protection for Those NOT Diagnosed with Diabetes…. YET

The Vitality Plus program offers ALL applicants an opportunity to save on premiums by rewarding healthy habits. Clients who have added the Vitality rider to their John Hancock policy complete an annual Vitality Health Review (VHR). If your client is diagnosed with diabetes at ANY TIME the policy is in-force, they can update the VHR and automatically gain access to ASPIRE and all its benefits. Since Vitality’s 2015 inception, John Hancock has reportedmeaningful positive heath results including:

weight reduction in nearly 50% of participants

improved cholesterol levels in 25% of participants

$8.4M in rewards have been earned by Vitality customers

Click here to find out how your clients can earn points with Vitality.

While the COVID 19 vaccine offers us some hope, clients living with diabetes and other chronic conditions still pose a greater risk from a mortality perspective. NOW is the time to have conversations with your clients about the importance of planning. AgencyONE’s underwriters are experts with impaired risk cases and can help your clients find the ideal home for their coverage.

Section 205 of the Consolidated Appropriations Act, 2021 (H.R. 133) signed by President Trump on December 27th, 2020 made changes to Internal Revenue Code Section 7702 providing for the use of a more dynamic interest rate methodology when calculating the “Definition of Life Insurance” (or DOLI) that dates to the 1984 Deficit Reduction Act, also known as DEFRA, where Section 7702 was first introduced. The new methodology will allow changes over time in line with market interest rates, versus the traditional fixed rate that was established in a very high interest rate environment.

Section7702 Defined

A discussion of U.S. Code Section 7702 where “the definition of life insurance” is described can be found in a variety of places, including the Internal Revenue Code, but I have provided the following (more simple, if that is even possible) information from Cornell Law School’s Legal Information Institute. A full discussion of Section 7702 goes beyond the purpose of this article, but the aforementioned link provides a suitable framework to understand where this is going.

Simply stated, Section 7702 was enacted under DEFRA in response to the abuses created by single premium life insurance contracts (a tax shelter\haven) in the early 1980s thereby limiting the funding pattern of life insurance, discouraging single premiums, and discouraging further abuses. This was also around the time when Universal Life was just coming to market with illustrated rates in excess of 10%. I started in the insurance industry in 1982 and remember these “glory” days, I am sure many of you do as well.

As interest rates have steadily decreased for 35 plus years, since 1984, the funding limitations for life insurance (the maximum allowable premiums as defined under Section 7702) were limited by either a 4% or 6% interest rate test depending on which methodology was chosen. These rates were fixed in the codification of Section 7702 and hence artificially high in today’s interest rate environment.

While H.R. 133 was really intended to solve some very significant challenges that Whole Life was experiencing due to the current interest rate environment, it may also present some unintended consequences for Universal Life that the law did not anticipate. As a result of H.R. 133, the maximum Guideline Premiums under DEFRA and, by consequence, the maximum non-MEC (Modified Endowment Contract) premiums introduced subsequently by TAMRA in 1987, are going up substantially, potentially doubling at certain ages.

Designing an Efficient Contract Within the Tax Code

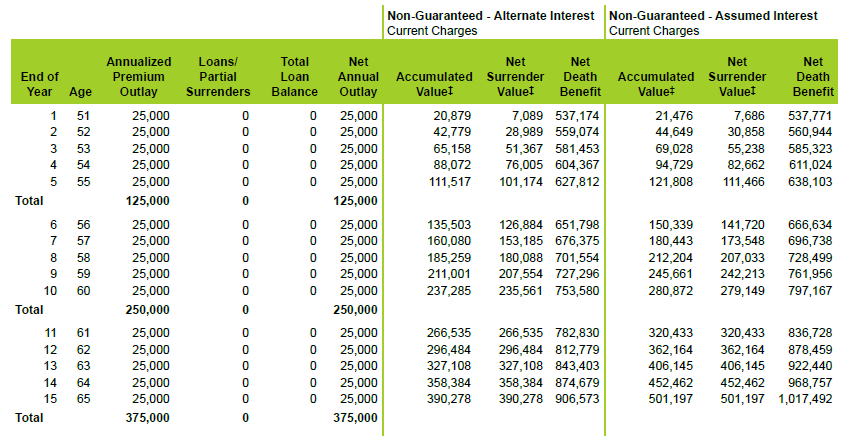

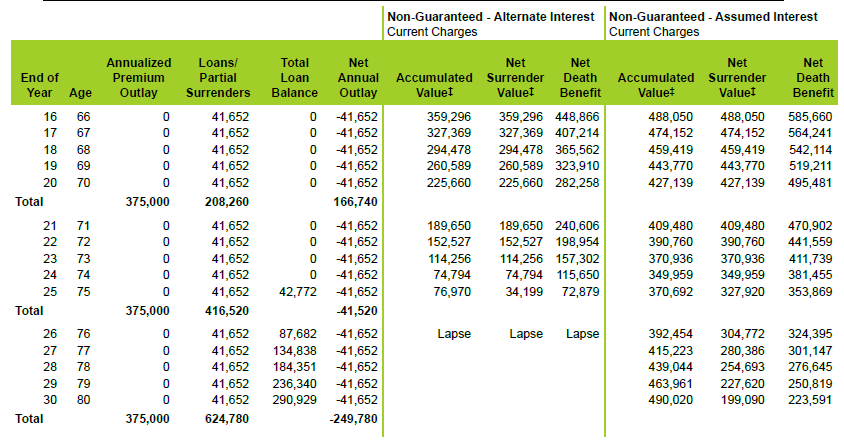

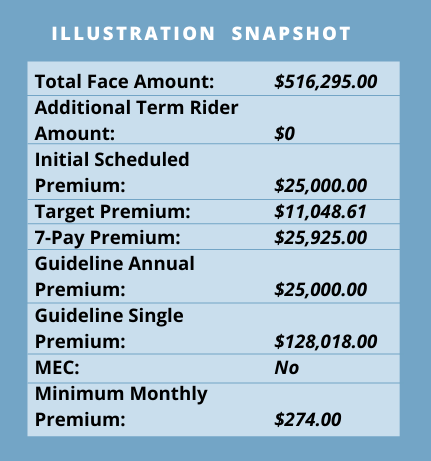

Now to the actual subject matter of this article because this is where things really get interesting. By way of example, let us use a 50-year-old male, Preferred Non-Tobacco class, in a supplemental retirement accumulation scenario. The goal of this proposal design is to make the life insurance contract as efficient as possible without violating the tax code, meaning, contributing the maximum premium allowable under DEFRA and TAMRA, as previously afforded under the law, for the minimum death benefit.

In this case you will see the following:

An initial premium contribution of $25,000 per year for 15 years (to the client’s age 65)

An initial minimum non-modified endowment death benefit of $516,295

An increasing death benefit option during the premium payment period (death benefit PLUS accumulation account)

When premiums cease (age 65), a lowering AND leveling of the death benefit option to maintain the DEFRA and TAMRA compliance corridor

Tax-free withdrawals to basis starting at age 66 and tax-free loans after the basis has been withdrawn for the balance of 20 years (to age 85)

Pre-Retirement (funding period)

Post-Retirement (distribution period)

A snapshot of the various premium limits is seen to the left. As you can see, the $25,000 scheduled premium meets the Guideline Annual Premium and is below the 7-Pay (Non-MEC) Premium by a small amount, maintaining Non-MEC status. The target premium is also listed as $11,048.61.

For those of you that are not familiar with the concept of a target premium, it is the premium for which the writing agent is compensated on at the first-year rate and anything over that ($25,000 minus $11,048.61) is compensated at the “excess rate”, which is a fraction of the first-year rate.

If we go back to what was said earlier about the Guideline Premium essentially doubling, under the new rules a client would be able to contribute $50,000 to this same policy with a $516,295 death benefit.

The target premium is a per thousand rate that is face amount driven. If you do that math, then you will conclude, as I have, that while doubling the premium contribution on the part of the client, the target premium would stay the same. The impact of this is that there is a LOT more excess premium with no expense\load for first year commission.

NOT doubling (or increasing) the target commissionable premium would have the impact of:

Making the contract much more efficient and benefitting the client from an accumulation standpoint, AND

Reducing the compensation to the agent per dollar of actual premium collected on the sale by half (approximately).

The question is …. will the carriers, when they start re-designing their products to comply with H.R. 133, double (or increase) the target premium or will they expect insurance agents to receive half of their previous compensation for the “same sale”?

Increased Insurance Sales Under Section 7702?

If the insurance community expects that the tax-deferred efficiency of life insurance along with lower-loads on premiums will lead to more sales of life insurance, then it can make up the difference in more sales to tax savvy clients. If not, then the carriers will have to decide who wants to play the game of chicken by not increasing target premiums while other carriers do and risk that some advisors will not sell their product and pivot to the carrier that has a product with a more compelling target premium instead.

Let us be mindful that the industry has been under a lot of pressure from regulators and fee-based pundits that commission-based life insurance is a “bad investment as a retirement vehicle”. Before this 7702 change we know that was an erroneous allegation; post 7702, it will still be wrong, but just by a matter of degrees. How much will the industry put on the table to provide a much more cost-efficient product for consumers and hopefully gain more customers? Or will the “new insurance advisor” be more wealth management driven as is the fee-based\ fiduciary advisor community?

It is up to the insurance company executives and actuaries to figure out how this will play out. Will the solution be “on target”?

Again, please join AgencyONE tomorrow (January 28, 2020), at 4:00 p.m. EST for a complete discussion about the changes to IRC Section 7702 and how these changes are likely to impact your sales practices.

The reality of COVID-19 has affected us profoundly – personally and professionally. As a result, many of your clients may be re-evaluating their insurance and protection needs and asking what they should be doing to better protect their families and/or businesses. Is their current and/or proposed life insurance coverage enough considering the current health threats and economic conditions? It may be a good time to discuss policy servicing.

Opportunities During Covid

COVID has been devastating to many but it has also presented an opportunity for insurance advisors to check-in with existing clients on their health and well-being and suggest a review of their inforce policies and protection needs. Now is an excellent time to review older policies since NEW benefits, riders, and products exist that can prove very VALUABLE to your clients. Just in the last year, AgencyONE has experienced about 2-3 times more cases to review as compared to previous years. Following are a few examples worth sharing:

Opportunity: A minimum funded plan that was originally designed to provide income to the client during retirement. A plan review revealed that no money would be available and that the contract would lapse at age 70. Result: An informal was submitted for a new plan.

Opportunity: An older inforce IUL policy that was underfunded and had numerous cap reductions. After review, AgencyONE determined the original goals could not be met without the client paying additional premiums or dropping the death benefit. Result: An informal was submitted for a new plan.

Opportunity: A client with 4 poorly managed whole life policies with loans, incorrect dividend options, and the mistaken belief that the policies were paid up. After AgencyONE’s review the client adjusted the policies’ dividend options to pay premiums and paid off the existing loans. As a result, the contracts are back on solid ground. Result: No additional sale but a very happy client whose advisor clearly has his/her best financial interests at heart.

Opportunity: A 20-year old contract that the client could not identify. With AgencyONE’s help, the advisor determined the policy was a VUL contract with cash sitting in a fixed account. Result: Client decided to 1035 the cash into a new contract with an LTC rider that would better suit his current needs.

Opportunity: An existing term contract with a few years remaining. After reviewing for a conversion, AgencyONE and the advisor determined the existing carrier’s conversion products were not competitive in cost and, since the client WAS insurable, new coverage was recommended. Result: A new term sale occurred to lock in more competitive coverage.

The cases above are a small sample of the cases that we reviewed. Every case is different and while some only need a few tweaks to fix any issues, others are in drastic need of help and possible replacement. The important point is that a policy review WILL help your clients and possibly get you an additional sale.

Requirements for Policy Review

You may be asking, “What information do I need to start a policy review for my clients?” Along with a generic policy review package, following are some additional items required to initiate a review for your clients who have existing policies:

A current annual or policy value statement. This item will provide the death benefit, current cash and surrender values along with any loan on the policy (loans may be handled more efficiently in a newer IUL contract but a review is required to make a determination). A statement will also show any subaccounts that apply and any monthly charges.

Two current inforce ledgers. The first should be run “as is” which will show the premium being paid and the current rate of return of the contract. (A UL policy illustration will show at the current interest rate. A VUL or IUL contract should be run at a level rate of 5% as a baseline). This first ledger will show us if the contract is performing according to expectations or not. The second illustration should be run at a current rate (or choose a 5% rate of return) solving to age 100. Additional scenarios may also be needed, but the first two can tell us quite a bit about the current contract. Please note: If you are not the agent of record, it is possible to obtain information on policies but the client/policy owner will be required to assist.

Essential client information including date of birth, state of residence, and possible underwriting class. We do not need a full underwriting file yet but we do need enough information to ascertain whether the client will qualify for new coverage, if it is needed.

Gathering the information above helps us identify the type of policy, determine if any riders are included, establish if the contract is holding its own or additional premium is required, and identify the existence of any guarantees. If an inforce illustration shows that additional premium is required, we consider replacing the existing contract with a new product and, in some cases, adding a chronic or LTC rider. Again, this is the first step in determining whether maintaining the existing contract is the best decision.

A Better Way to Service Policies

If you have legacy business, we suggest you have a look at an inforce policy management platform – called Proformex – that has streamlined and automated policy servicing needs.

Half of all existing insurance policies require some form of corrective action to ensure their protection reflects the clients’ needs. Under normal circumstances, servicing policies can require a significant and ongoing commitment of time. Proformex’s automated platform has significantly reduced the time it takes to manage your policies down to minutes rather than hours.

The Proformex system aggregates and consolidates all policy data into one location. It actively monitors individual policy performance and identifies at-risk policies thereby uncovering new sales opportunities. Advisors, agents, banks, and brokers who use Proformex have “generated up to 40x ROI through more meaningful client engagements and new policy sales.” Contact AgencyONE if you would like a demo of the Proformex platform.

The value and importance of regularly reviewing your clients’ policies and proposed coverage cannot be understated. AgencyONE possesses the tools and resources to help you initiate important conversations with your clients and analyze their inforce business.

The most meaningful impact of 2020 on the insurance industry was, very likely, the dramatic drop of interest rates. They have had a much greater effect than most people imagine. The bell weather indicator for interest rates in the insurance industry is the 10-year Treasury, as it constitutes a large portion of an insurance company’s portfolio. In 2018 yields were already low (sub-3%) but rising slowly, giving some insurance company executives a slightly more optimistic view on the financial pressure they had been experiencing. On November 8th, 2018, the 10-year rate peaked at 3.24%, then began to drop again …. and then COVID hit. Between January 1, 2020 and April 21, 2020 the yield plummeted from 1.92% to .58% – a 70% drop. As I write this, the rate is 1.10%.

10-Year Treasury

When the yield on new money investments (premiums coming into an insurance company) drops 70% and as older bonds mature and you must reinvest the proceeds at .58% – that hurts! Why? Because this reinvestment begins to bring down your overall portfolio yield spread (the money the insurance company earns on a portfolio versus the money they credit on interest bearing products). This spread accounts for a fair portion of the profits of an insurance company.

Life Insurance Operational Challenges

2020 was a year of significant changes for insurance companies and most were as a result of the low interest rate environment. Did you wonder why so many senior people at your favorite insurance company retired last year or were laid off? Did you wonder why service levels at the insurance companies, despite heroic efforts and hard work, was terrible? Did you wonder why dividends dropped almost across the board on Whole Life insurance? Did you wonder why insurance companies did not want to take a check from that wealthy client of yours for $1,000,000? Did you wonder why products were pulled off the market or got more expensive? Did you wonder why underwriting decisions tightened? Did you wonder why insurance companies were pushing their Variable Life portfolios over their fixed product lines? There is one fundamental answer to all these questions – persistent low interest rates.

To compound these problems, some companies saw increases in business, as measured by application counts, in the high double digits. The carriers were understaffed, over-committed and operating on smaller margins. Meanwhile, most companies were rolling out not fully tested underwriting technology to handle this increased application count with mixed results. It sounds like a terrible situation – and it was.

And let us not forget the uncertainty that was prevalent around the election results impacting the very high estate and gift tax exemptions. If you were in the ultra-high net worth market, taxpayers, on the advice of their very smart lawyers, were moving large amounts of money into trusts and buying (or financing) life insurance. Did I mention that insurance companies did not really want big premiums?

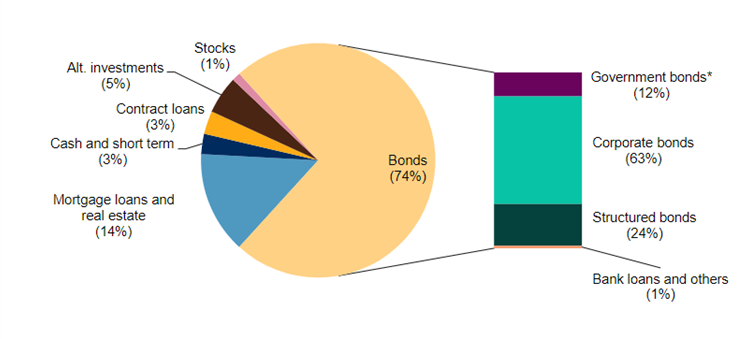

Breakdown of U.S. Life Insurers’ Investment Portfolio

With all of that said, the life insurance industry has weathered many storms and is remarkably resilient and frankly, very integral to the overall wellbeing of the U.S. economy. S&P Global reported, in an article on September 16th, 2020, that at the end of 2019 the life insurance industry held $4.5 trillion in portfolio values with over 70%, or $3.1 trillion, in fixed-income securities. They will come out of this generally unscathed, but it will be a long hard road.

2021 & Insurance Industry Expectations

So, welcome 2021. What headwinds and opportunities do we see for 2021 after what could be called a disastrous year for the industry?

I am a “glass half full” kind of guy and I see a ton of upside in our industry for years to come and there are certainly things that will emerge in 2021 despite a continuing difficult situation with COVID, interest rates, and uncertainty around the economic and regulatory environment.

What to watch for in 2021:

Product pricing, changes and introductions – I listened to the Finseca (the merger of AALU and GAMA) webcast on January 13th with Bobby Samuelson and he said one thing that really struck me … it was something along the lines of “if you thought product changes were crazy in 2020, just wait, it will be even crazier this year”.

We have already seen some product discontinuance announcements in terms of Guaranteed Single Life and 2nd to Die Universal Life from some major carriers. The price of long dated guarantees (age 100+) is going to continue to get more expensive in the Universal Life market if they are even available by the end of the year.

Bobby also discussed the recent changes in IRC Code Section 7702 which deals with the Guideline Premium Test (GPT), the Cash Value Accumulation Test (CVAT) that came out of the 1984 Tax Act (DEFRA) and consequently the Modified Endowment Contract (MEC) Test, that came of the 1987 Tax Act (TAMRA). While this will have an impact particularly on Whole Life, it will also increase the MEC limits for Universal Life (Fixed, Index and Variable) allowing clients to put more money into these contracts per dollar of face amount. This is a complex area and worthy of a ONEIdea and further discussion as carriers discontinue products and introduce new ones throughout the year.

No-Loan or Low Load life insurance for distribution in the wealth management space as a tax deferred accumulation strategy will begin to emerge. I have been privy to and involved with some development efforts from a variety of companies already with plans to launch these products in 2021.

Changes in Income, Gift and Estate Tax Rates – The Biden administration’s view on taxes will likely create higher income taxes (likely for higher income earners) and a change in the estate and gift tax regimes (likely lower exemptions and the possibility of changes in the step up in basis). These will create opportunities for financial professionals to discuss planning opportunities using several different tools/strategies:

Irrevocable Life Insurance Trusts may become a tool that more of the population may need if and when the estate tax exemption is reduced.

The low interest rate environment will continue to be very attractive for

Grantor Retained Annuity Trusts

Intra-family loans or asset sales in exchange for notes

With higher income taxes, tax deferred accumulation using life insurance will be more attractive as Roth IRAs may not generally be available to those taxpayers impacted by the higher rates.

Technology – Underwriting technology will continue to develop and grow. The insurance industry had to accelerate years of R&D in technology advances to facilitate underwriting during COVID for contactless and “no fluids” underwriting. Algorithmic underwriting (with little or no human intervention) will continue to play a huge role in the smaller transactional business while electronic health records (EHRs) and other ways to collect needed underwriting data will rule the day for larger risks. Full underwriting will continue to occur, just in a non-traditional way.

Continued merger and acquisition activity in life distribution – There was a meaningful amount of M&A activity in the distribution of life insurance starting with the merger between LifeMark Partners and BRAMCO last year. Industry associations such as AALU and GAMA merged. Finally, large firms (public and private) such as Gallagher, Acrisure and Private Equity firms acquired large producer organizations and brokerage general agencies.

2021 looks bright but as I said before, it will not be for the faint of heart. AgencyONE will be covering many of these opportunities over the course of our 2021 Webinar series starting on January 21. Please be on the lookout for invitations and registration information.

A Decision By Young Parents

A Decision By Young Parents

Life Insurance For Children – A Good Decision?

Life Insurance For Children – A Good Decision? financial underwriting guidelines for insuring minor children that you should be aware of, in addition to medical underwriting guidelines and procedures. Nevertheless, most insurance companies do not require the typical underwriting scrutiny for minors, such as exams and lab work and many will issue policies with very limited underwriting requirements.

financial underwriting guidelines for insuring minor children that you should be aware of, in addition to medical underwriting guidelines and procedures. Nevertheless, most insurance companies do not require the typical underwriting scrutiny for minors, such as exams and lab work and many will issue policies with very limited underwriting requirements.")

The client was NOT asked by his advisor if he uses marijuana. The advisor just ASSUMED that the client did not. While many carriers are NOT testing for THC (the psychoactive compound in marijuana) on insurance exams, they can and will at their discretion.

The client was NOT asked by his advisor if he uses marijuana. The advisor just ASSUMED that the client did not. While many carriers are NOT testing for THC (the psychoactive compound in marijuana) on insurance exams, they can and will at their discretion.

Diabetes & Covid

Diabetes & Covid

they should be doing to better protect their families and/or businesses. Is their current and/or proposed life insurance coverage enough considering the current health threats and economic conditions? It may be a good time to discuss policy servicing.

they should be doing to better protect their families and/or businesses. Is their current and/or proposed life insurance coverage enough considering the current health threats and economic conditions? It may be a good time to discuss policy servicing.