Managing Insurance Policy Conversions During the Covid Crisis

The Covid-19 shutdown has had a profound effect on HOW advisors do business and WHAT TYPE of business they do. At AgencyONE, we are seeing these differences in the insurance we are quoting and the way in which business is being placed. The use of accelerated underwriting platforms (AUP) have taken off and we have seen a HUGE increase in submissions over the last few months. Advisor quote requests and applications for permanent coverage have increased as clients are more motivated in the current environment to obtain the necessary coverage to protect their families and businesses. We have also received notice that carrier pricing is increasing on Guaranteed UL (GUL) products due to the low interest rate environment and the reserve requirements needed for long dated guarantees. Finally, conversion requests have almost TRIPLED over the last few months!

TO CONVERT OR NOT?

It makes sense that term conversion requests have dramatically increased during the Covid crisis since they are an EASY NO-CONTACT way to obtain PERMANENT coverage. Each conversion request must be carefully reviewed to make sure the requested carrier is appropriate, the products are available, and that the client in question is still INSURABLE. You may ask “Why does the client have to be “insurable” if we are converting?” The answer is that the carrier’s conversion product MAY NOT be the best fit or the lowest cost option for your client. Some carriers have options that are competitive in price, but do not offer a Chronic/LTC rider without additional underwriting. Other carriers have conversion-only products with higher costs and limited flexibility. So, if your client is considered insurable, AgencyONE will direct you to alternative products and carriers that may be better suited to your client’s current needs.

CASE STUDY – Conversion or New Policy Option

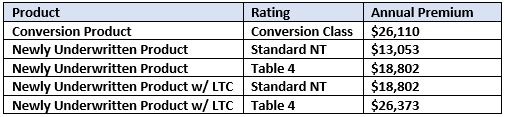

Let’s look at the pricing for a conversion-only product compared to a fully underwritten NEW option for Mr. Smith who is 50 years of age, considered Standard Non-Tobacco (NT), and would like $1,000,000 in coverage:

Assuming Mr. Smith is insurable and qualifies at standard or better, he could apply for the newly Underwritten Product with an LTC option through an accelerated underwriting program (AUP). Note that, even at a Table 4 rating, Mr. Smith would be able to obtain NEW coverage at almost the same price as the Conversion Product!

The numbers in the table above show how important it is to review the client’s insurability when considering a conversion. You DO NOT want to MISS the chance to write a policy for a new product that will better serve the needs of your client. If your client is truly uninsurable, they will still have the conversion option to fall back on.

CONVERSION MARKETING

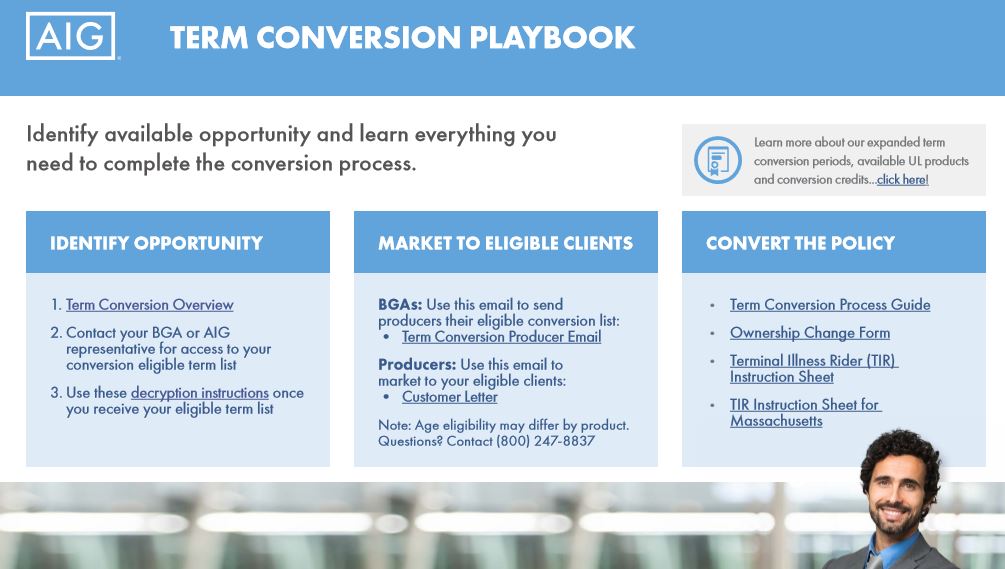

To help find and market conversion options in your book of business, one of our carrier partners has created a very helpful micro site called the Term Conversion Playbook.

This fully functional site will, among other things, help you identify term conversion opportunities, provide template marketing and email to reach your clients, and information and details about the conversion process. We hope you will take the time to explore the possibilities it offers.

AgencyONE can provide a list of ALL term policies written by our AgencyONE 100 advisors through our office. If you would like to obtain a list of your term business or discuss a case, please contact our Illustrations Department at (301) 803-7500.