Executive Bonus Plans CONTINUED

Last month’s One Idea from AgencyONE’s Case Design department discussed a planning option for businesses that is currently experiencing a resurgence in popularity – the Executive Bonus Plan. Executive Bonus Plans are an effective way to help retain key employees by using overfunded life insurance. November’s ONE Idea prompted calls from advisors who wanted to discuss designs and ideas for prospective cases using an Executive Bonus Plan.

EXECUTIVE BONUS PLAN – POLICY & AN LTC RIDER?

One of our AgencyONE 100 Advisors was quick to point out that I had not mentioned the inclusion of a Long-Term Care (LTC) rider on the underlying life policy. I opted NOT to add an LTC rider primarily because it would increase policy costs, and these increased costs would affect future cash values AND projected income amounts. Future benefits/values are impacted when taking income and LTC benefits from the policy at the same time. After talking with the advisor about her case, I checked to see how the addition of an LTC rider would impact the initial sale. It would be worth adding if the numbers made sense. LTC coverage is an extremely valuable benefit to many people right now. The client would receive a policy that provides death benefit, cash values AND/OR possible LTC benefits – MORE options and MORE value for the business owner client to offer the key employee.

EXECUTIVE BONUS PLAN – 2 CASES TO CONSIDER

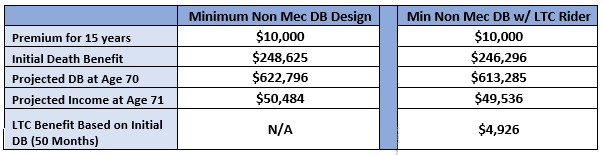

Let’s look at two cases that use the same premium and solve for a minimum non mec death benefit (DB). One is designed for maximum cash value and income while the other includes the LTC rider.

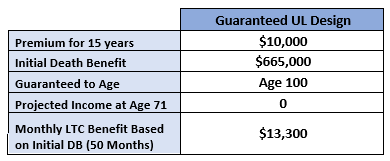

Looking at the values in the table above, I was surprised that they did not significantly drop with the addition of the LTC rider. It is assumed that cash value and income are still the main requirements, but what if we go a step further and design a plan using the same $10,000 premium but make it focused on death benefit as opposed to cash value and income. The higher DB will provide a larger pool of potential LTC benefits.

The above GUL design will provide the key employee with a fully paid-up policy after 15 years and has the option to accelerate the death benefit for LTC if needed in the future. This option is different than the original design from last month’s ONE Idea which used the restriction of cash value to help incentivize the key employee to stay with the company. The DB design does not have cash value but requires the payment of 15 premiums to become fully paid up. If the key employee wants the policy with ALL of its benefits, he/she will need to remain employed or continue to make the premium payments themselves upon departure from the company.

EXECUTIVE BONUS PLAN DESIGN – A PERSONAL CHOICE

EXECUTIVE BONUS PLAN DESIGN – A PERSONAL CHOICE

Selecting a plan focus is a very personal choice so, it is important to include the key employee in the decision process and allow him/her to determine which plan works best. As mentioned earlier, more options translate into more value for the key employee with the goal of increasing employee retention. Not everyone has the same planning goals.

AgencyONE works to collaborate with you and your clients to design the best possible solution to fit your clients financial and insurance planning goals.

Tis the season of STRESS!!! The hustle and bustle of the holiday season is upon us, and this time of year can cause increased anxiety and even depression. Both are common diagnoses and are not just considered seasonal. As with any condition, there are varying levels of severity. In this ONE Idea, we will discuss the differences between anxiety and depression and how they are viewed during underwriting.

Tis the season of STRESS!!! The hustle and bustle of the holiday season is upon us, and this time of year can cause increased anxiety and even depression. Both are common diagnoses and are not just considered seasonal. As with any condition, there are varying levels of severity. In this ONE Idea, we will discuss the differences between anxiety and depression and how they are viewed during underwriting.

As the most common group of mental illnesses in the country, anxiety is treatable by safe and available medications. Surprisingly, less than 50% of Americans seek the necessary treatment. Anxiety by itself, if considered “controlled” with mild medications, is a LESSER underwriting concern. However, many times it is paired with a second diagnosis of depression which can be a GREATER underwriting concern.

As the most common group of mental illnesses in the country, anxiety is treatable by safe and available medications. Surprisingly, less than 50% of Americans seek the necessary treatment. Anxiety by itself, if considered “controlled” with mild medications, is a LESSER underwriting concern. However, many times it is paired with a second diagnosis of depression which can be a GREATER underwriting concern. include irritability, anxiety, disinterest, fatigue, insomnia, change in appetite, avoiding people, feelings of worthlessness or guilt, difficulty thinking, concentrating, or making decisions, and excessive crying. The most concerning is when the patient has recurrent thoughts of death or suicide, or a suicide attempt.

include irritability, anxiety, disinterest, fatigue, insomnia, change in appetite, avoiding people, feelings of worthlessness or guilt, difficulty thinking, concentrating, or making decisions, and excessive crying. The most concerning is when the patient has recurrent thoughts of death or suicide, or a suicide attempt. Depression can be influenced by many factors such as environment, genetics, hormones, or simply changes in how our brains function over time. Along with anxiety, depression has varying levels of severity from mild and situational (like a grief reaction), to major and recurrent. Treatment strategies for anxiety and depression can range from psychotherapy, diet, exercise, brain stimulation therapies or prescription medications. Depressive/anxiety conditions may require multiple medications, dosage adjustments, and for some it can be an ongoing challenge to manage.

Depression can be influenced by many factors such as environment, genetics, hormones, or simply changes in how our brains function over time. Along with anxiety, depression has varying levels of severity from mild and situational (like a grief reaction), to major and recurrent. Treatment strategies for anxiety and depression can range from psychotherapy, diet, exercise, brain stimulation therapies or prescription medications. Depressive/anxiety conditions may require multiple medications, dosage adjustments, and for some it can be an ongoing challenge to manage.

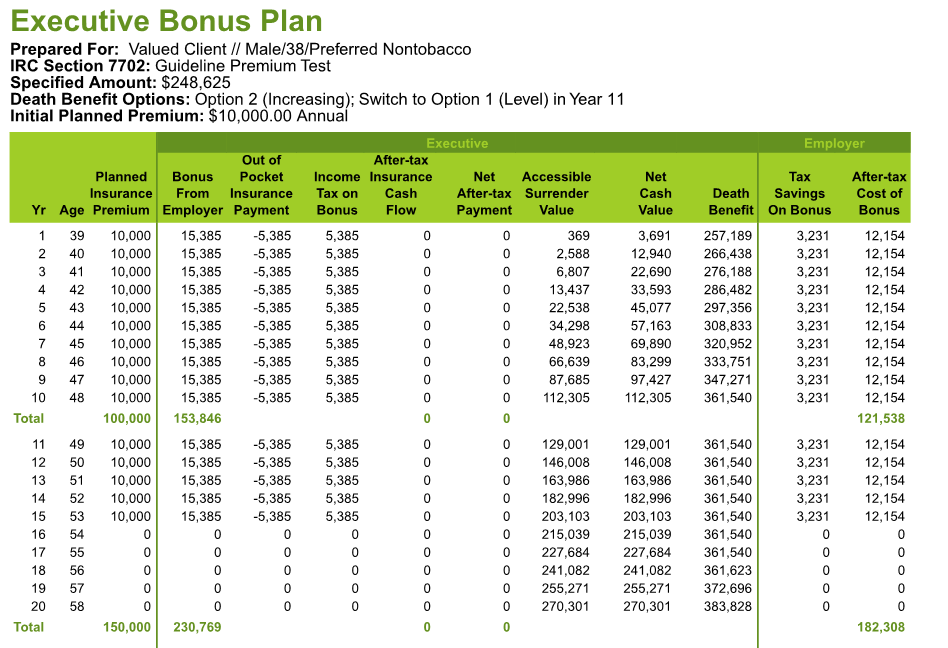

A 162 Bonus Plan aka Executive Bonus Plan

A 162 Bonus Plan aka Executive Bonus Plan

Let’s review one of the recent cases I mentioned above. The owner of a small company has been concerned with employee retention. All of the press regarding the “Great Resignation” has been worrying and he wanted to make sure that two of his most key executives were incentivized to stay with the company (male executive age 38 and female executive age 42). The owner was willing to bonus each employee $10,000 per year for 15 years and also wanted to “gross up” the bonus to cover the taxes due. Assuming the executives were in a 35% tax bracket, that would result in a total bonus of $15,385 per year.

Let’s review one of the recent cases I mentioned above. The owner of a small company has been concerned with employee retention. All of the press regarding the “Great Resignation” has been worrying and he wanted to make sure that two of his most key executives were incentivized to stay with the company (male executive age 38 and female executive age 42). The owner was willing to bonus each employee $10,000 per year for 15 years and also wanted to “gross up” the bonus to cover the taxes due. Assuming the executives were in a 35% tax bracket, that would result in a total bonus of $15,385 per year. arrangement. A Restrictive Endorsement is created between the employer and the key executive. This agreement requires the employer’s consent for the executive to have access to the policy values, which provides enticement for the executive to remain employed for a specific length of time. The agreement may also stipulate a vesting and repayment schedule in the event the executive does not fulfill the employment time frame set forth in the agreement. AgencyONE’s plan was designed to allow the executive 10% access to the cash value in year one and this will increase by 10% each year through year 10. In year 10 the Executive will be fully vested in the plan and will have 100% access to the cash value. Our carrier partner on this case has the administrative processes in place to help implement and monitor the terms of the Restrictive Endorsement.

arrangement. A Restrictive Endorsement is created between the employer and the key executive. This agreement requires the employer’s consent for the executive to have access to the policy values, which provides enticement for the executive to remain employed for a specific length of time. The agreement may also stipulate a vesting and repayment schedule in the event the executive does not fulfill the employment time frame set forth in the agreement. AgencyONE’s plan was designed to allow the executive 10% access to the cash value in year one and this will increase by 10% each year through year 10. In year 10 the Executive will be fully vested in the plan and will have 100% access to the cash value. Our carrier partner on this case has the administrative processes in place to help implement and monitor the terms of the Restrictive Endorsement.

Accelerated Underwriting (AUW) which could result in a quick turn-around assuming he qualifies. The details of this case tend to be right in the “sweet spot” for AUW solutions which are run with a minimum non mec death benefit to maximize the cash value over time. You can find an up-to-date Accelerated Underwriting spreadsheet on your personal AgencyONE Advisor Dashboard in the Underwriting dropdown tab. The sheet outlines all of our carrier partners’ AUW programs. Please note that you will need to be authorized to use our website to access this tool.

Accelerated Underwriting (AUW) which could result in a quick turn-around assuming he qualifies. The details of this case tend to be right in the “sweet spot” for AUW solutions which are run with a minimum non mec death benefit to maximize the cash value over time. You can find an up-to-date Accelerated Underwriting spreadsheet on your personal AgencyONE Advisor Dashboard in the Underwriting dropdown tab. The sheet outlines all of our carrier partners’ AUW programs. Please note that you will need to be authorized to use our website to access this tool.

Finding Tax Efficiencies

Finding Tax Efficiencies

How to Improve an IRR

How to Improve an IRR few design and underwriting rules:

few design and underwriting rules:

Another Competitive Option – Survivorship

Another Competitive Option – Survivorship

protection against risk, properly structured temporary and permanent life insurance coverage can help mitigate the risks to which HNWFN are exposed – including generational wealth transfer and taxation on their worldwide income and assets.

protection against risk, properly structured temporary and permanent life insurance coverage can help mitigate the risks to which HNWFN are exposed – including generational wealth transfer and taxation on their worldwide income and assets. Taxation issues may arise for couples when one partner is NOT a US citizen and become problematic upon the death of one spouse. Most clients are NOT aware that taxes will be due …until the IRS letter arrives! The solutions to this problem lie in strategic estate planning and the necessary life insurance protection.

Taxation issues may arise for couples when one partner is NOT a US citizen and become problematic upon the death of one spouse. Most clients are NOT aware that taxes will be due …until the IRS letter arrives! The solutions to this problem lie in strategic estate planning and the necessary life insurance protection.

We often say at AgencyONE that the details will make or break a case. The HNWFN market is exciting, challenging and rewarding. Term and permanent coverage are available from many carriers, but it is CRITICAL to understand the carrier NUANCES – there are MANY. The HNWFN platforms that the carriers offer are unique in that they are even MORE competitive than the products offered. Securing coverage is the key and AgencyONE has the KNOWLEDGE and RELATIONSHIPS to direct your client to the right carrier!

We often say at AgencyONE that the details will make or break a case. The HNWFN market is exciting, challenging and rewarding. Term and permanent coverage are available from many carriers, but it is CRITICAL to understand the carrier NUANCES – there are MANY. The HNWFN platforms that the carriers offer are unique in that they are even MORE competitive than the products offered. Securing coverage is the key and AgencyONE has the KNOWLEDGE and RELATIONSHIPS to direct your client to the right carrier!

the SAME mortality risk as a non-pilot, meaning they would be underwritten at the top Preferred class in which they qualify. Some licensed pilots also fly PRIVATE, which CHANGES the risk perception for insurance companies.

the SAME mortality risk as a non-pilot, meaning they would be underwritten at the top Preferred class in which they qualify. Some licensed pilots also fly PRIVATE, which CHANGES the risk perception for insurance companies. VISUAL FLIGHT RULES (VFR) mean that the aircraft is intended to operate in Visual Meteorological Conditions (VMC), i.e., clear skies, nice weather, ideal visibility. Fog, heavy precipitation, low visibility, and otherwise adverse weather conditions are supposed to be avoided (which is why these “rules” were a big topic of discussion surrounding Kobe Bryant’s death, as the helicopter was flying under MODIFIED VFR rules).

VISUAL FLIGHT RULES (VFR) mean that the aircraft is intended to operate in Visual Meteorological Conditions (VMC), i.e., clear skies, nice weather, ideal visibility. Fog, heavy precipitation, low visibility, and otherwise adverse weather conditions are supposed to be avoided (which is why these “rules” were a big topic of discussion surrounding Kobe Bryant’s death, as the helicopter was flying under MODIFIED VFR rules). a bit of cost to your client’s life insurance premiums. As in medical underwriting, carriers can view the same information very differently. If your client answers “yes” to any of these questions, it is very important to request and complete the specific avocation questionnaire(s) that apply. To find these questionnaires, log into the

a bit of cost to your client’s life insurance premiums. As in medical underwriting, carriers can view the same information very differently. If your client answers “yes” to any of these questions, it is very important to request and complete the specific avocation questionnaire(s) that apply. To find these questionnaires, log into the Harry Daredevil is a 35-year-old executive with no significant medical history. He has a student pilot license and has logged only 12 hours of flight time over the last year. He intends to fly an additional 30 hours over the next year and complete the requirements to get a Private Pilot certificate. Mr. Daredevil is applying for $10M of TERM coverage and does not want to exclude aviation from the risk.

Harry Daredevil is a 35-year-old executive with no significant medical history. He has a student pilot license and has logged only 12 hours of flight time over the last year. He intends to fly an additional 30 hours over the next year and complete the requirements to get a Private Pilot certificate. Mr. Daredevil is applying for $10M of TERM coverage and does not want to exclude aviation from the risk.

their reinsurance treaties. They are audited regularly. Like it or not, all underwriters are REQUIRED to ascertain specific information to assess mortality accurately and approve the desired death benefit.

their reinsurance treaties. They are audited regularly. Like it or not, all underwriters are REQUIRED to ascertain specific information to assess mortality accurately and approve the desired death benefit.

During COVID, getting an insurance exam became extremely challenging. Carriers had to pivot to get business placed. Those who had been piloting alternative data sources like patient portals, electronic health records, lab data, etc. had to quickly incorporate these tools into their underwriting. We also saw carriers temporarily modify their established AUW guidelines. These modifications allowed cases to be approved at higher ages and face amounts WITHOUT an insurance exam IF the carrier could procure enough recent medical information to satisfy the exam requirements (labs, build, blood pressure, smoking status, etc.) through these alternative data sources. In many instances, particularly with the

During COVID, getting an insurance exam became extremely challenging. Carriers had to pivot to get business placed. Those who had been piloting alternative data sources like patient portals, electronic health records, lab data, etc. had to quickly incorporate these tools into their underwriting. We also saw carriers temporarily modify their established AUW guidelines. These modifications allowed cases to be approved at higher ages and face amounts WITHOUT an insurance exam IF the carrier could procure enough recent medical information to satisfy the exam requirements (labs, build, blood pressure, smoking status, etc.) through these alternative data sources. In many instances, particularly with the

Our second ONE Idea for the month came From the Desk of Gonzalo Garcia, CLU on June 11th and is entitled

Our second ONE Idea for the month came From the Desk of Gonzalo Garcia, CLU on June 11th and is entitled

Each of these ONE Ideas is meant to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciated the opportunity to serve you and your clients.

Each of these ONE Ideas is meant to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciated the opportunity to serve you and your clients.