Conversations that financial planners have with their clients can be tricky. Most financial advisors only talk about “the money” and hope that the recommended planning is put in place so that future generations can continue to reap financial rewards. Other financial advisors, who tend to retain clients for multi generations, expand the conversation and go deeper, talking about other aspects of their clients lives and value systems which may be equal to or more important than “the money”. But what could be more important than “the money”? When asked, your clients will often tell you that there are a lot of things that are more important than ”the money”, such as family and health, relationships and education, or time and attention. These non-financial aspects to your clients lives truly reveal what is important to them today and the values that they would like to impart on future generations. And these conversations and the planning that results from them will determine whether your clients are leaving or living a legacy.

This ONE Idea, from October 2021, presents an article authored by AgencyONE Partner, Gonzalo Garcia, CLU, and published in the September 2021 issue of Broker World Magazine. Gonzalo’s article, entitled Leaving or Living A Legacy – What’s Your Story?, while well over a year old, still resonates. It focuses on the conversations that financial advisors who want to retain their clients for multiple generations SHOULD be having with them NOW so these clients can optimize multi-generational true wealth and be LIVING their legacies as opposed to LEAVING their legacies.

We invite you to read this article through the Broker World link and hope it assists you in reframing the conversations you have with your clients.

High Net Worth Foreign Nationals (HNWFN), aka Global Citizens, are a GROWING market of individuals who typically possess assets and interests across the world and find particular financial safety and security in US domiciled businesses and properties. The growth of this market has expanded BEYOND the traditional US markets we’ve come to expect and includes both US citizens living abroad (typically for more than 12 weeks per year) and non-US citizens living in the US. The HNWFN market offers more OPPORTUNITY than EVER to write US based Life Insurance protection for your applicable clients. Foreign National Underwriting for High Net Worth Global Citizens is a growing and lucrative market.

This ONE Idea will provide an understanding of this HNWFN market and also provide information on our upcoming webinar titled, High Net Worth Global Citizens & Foreign National Underwriting. AgencyONE will be hosting this webinar in October and specifically dedicating it to this market and its opportunities.

What Qualifies A HNWFN?

HNWFNs typically have a net worth of $5M or more and possess global business interests and property and other assets that TIE them to the US. Because these assets and interests require protection against risk, properly structured temporary and permanent life insurance coverage can help mitigate the risks to which HNWFN are exposed – including generational wealth transfer and taxation on their worldwide income and assets.

Benefits of Life Insurance for HNWFN

Taxation issues may arise for couples when one partner is NOT a US citizen and become problematic upon the death of one spouse. Most clients are NOT aware that taxes will be due …until the IRS letter arrives! The solutions to this problem lie in strategic estate planning and the necessary life insurance protection.

US life insurance offers many benefits to the HNWFN:

Asset diversification in global markets

Assets that are held in US dollars

Possibly less restrictions than life insurance from their home country

Increasing number of carriers available

Better pricing and more coverage availability

Industry regulation offering security and privacy

Underwriting for the HNWFN is NOT uniform from carrier to carrier. It varies and depends upon many factors such as:

Country of current residence

Citizenship

Connection/ Nexus to United States

Travel schedule

Green Card/ VISA status – an area of confusion for many advisors and clients.

Green Card Holder – someone who is a permanent resident alien (Foreign National non-US citizen). Underwriting for a green card holder is treated like the underwriting of a US citizen and is routine for the most part.

A VISA is issued to a citizen of a foreign country wishing to come to the US. They are more complicated because there are so MANY types (student, tourist, temporary worker, long-term worker, etc., etc., etc.), limitations depending upon country of origin, residency minimums, and rating limits.

Ability to provide applicable medical and financial requirements

Solicitation requirements

Every High Net Worth Foreign National Case is Different

As always, each case is different, but AgencyONE’s extensive knowledge about this market and our carrier partner relationships will help you identify the RIGHT CARRIER for your client and get your CASE PLACED. Following are some examples of cases that were recently placed:

$5M Key Person Term Coverage – Japanese Citizen

A 44-year-old standard NT female came to the US to live and work as a CEO of an advertising firm. She needed $5M of term insurance for Key-Person coverage. AgencyONE identified a number of carriers that would have been ideal for this client, but as we got further into the underwriting process, we discovered that the client still owned property in Japan. This ownership had the client falling into the HNWFN classification as opposed to a resident alien. This was a problem because most carriers will not provide coverage to Japanese citizens. (Japan has regulations that do not allow citizens to buy insurance coverage outside of their home country.) AgencyONE worked with one of our carrier partners who was willing to write this case and provide the client with the key person term coverage needed despite her status as a resident alien.

$7M Permanent Coverage – Canadian Citizen

A 54-year-old preferred NT male who is a Canadian citizen spends the majority of his time in Russia. His advisor approached AgencyONE looking for $7M of permanent coverage and asked if we had any carriers that would accept this risk. This client had ties to the United States in the form of real estate interests and brokerage accounts. The challenge with this case was the amount of time the client spends in Russia. Many carriers who write HNWFN business have Anti Money Laundering (AML) concerns with the country of Russia. AgencyONE again identified the RIGHT carrier for this client and was able to secure the permanent coverage requested despite the fact that the client spent the majority of his time in Russia. A great outcome for all involved. (Cheers – vashe zdorov’ye)

$9.8M Permanent Coverage – Chilean Citizen

A very wealthy 48-year-old Chilean citizen who was an impaired risk had relocated to the US. He was in the US on a specific visa. This VISA, an investor visa, qualified the client as a HNWFN. This required that he be underwritten as a HNWFN rather than as a domestic client. Since the client had a medical risk that would have bumped him out of allowable coverage through a HNWFN program but not a domestic program, AgencyONE needed to manage the case with “the right” carrier partner to view the client domestically. The coverage was needed to offset future taxes. With the Investor visa, the client would eventually be a permanent US resident and citizen or green card holder exposing his global net worth to US taxes.

Details Make or Break a Case

We often say at AgencyONE that the details will make or break a case. The HNWFN market is exciting, challenging and rewarding. Term and permanent coverage are available from many carriers, but it is CRITICAL to understand the carrier NUANCES – there are MANY. The HNWFN platforms that the carriers offer are unique in that they are even MORE competitive than the products offered. Securing coverage is the key and AgencyONE has the KNOWLEDGE and RELATIONSHIPS to direct your client to the right carrier!

Medical Impairments are not the only circumstances that threaten mortality and your client’s underwriting success. Hobbies and occupations offer their own type of risk (just ask Jeff Bezos and Richard Branson). With the advent of PRIVATE space travel, we are sure the Life Insurance companies are already considering the risk and how to charge EXTRA for it! In this ONE Idea we will discuss how aviation and other avocations affect underwriting for life insurance.

AVIATION & UNDERWRITING

Licensed Commercial Airline Pilots employed by registered airlines are subjected to intense training and certification. Assuming they are transporting passengers or freight, these pilots carry the SAME mortality risk as a non-pilot, meaning they would be underwritten at the top Preferred class in which they qualify. Some licensed pilots also fly PRIVATE, which CHANGES the risk perception for insurance companies.

Civil Aviation (private pilots) present different risks to the life insurance underwriter. There are multiple levels of licensure: Student Pilot Certificate, Private Pilot Certificate, and Instrument Flight Rating (IFR).

The following factors can affect the underwriting rate class:

Type of license earned

Type of aircraft flown

Number of solo flying hours and hours flown annually

A student pilot with little flight experience is considered a risk because they have a higher probability of accident (and death) than an experienced pilot. And newly licensed pilots with less than 100 hours of solo time also pose a greater risk because they are not yet considered experienced – 100 hours of solo flight time logged is considered experienced.

Underwriters will further dissect these risks by assessing the individual’s PROFICIENCY and the type of aircraft they fly. Is the pilot flying ENOUGH each year (about 25 hours) to maintain expertise but not more than 200 hours, which places the pilot in a higher risk class statistically for an accident?

VFR versus IFR

VISUAL FLIGHT RULES (VFR) mean that the aircraft is intended to operate in Visual Meteorological Conditions (VMC), i.e., clear skies, nice weather, ideal visibility. Fog, heavy precipitation, low visibility, and otherwise adverse weather conditions are supposed to be avoided (which is why these “rules” were a big topic of discussion surrounding Kobe Bryant’s death, as the helicopter was flying under MODIFIED VFR rules).

INSTRUMENT FLIGHT RULES (IFR) mean the flight/aircraft may operate under Instrument Meteorological Conditions (IMC), i.e., cloudy, or adverse weather conditions. A pilot who has earned his or her Instrument Rating (IR) has gone through intensive training focused on flying solely by using the airplane instruments – technically, the pilot does not even need to look out the window for visual guidance! Having this rating generally makes for a safer pilot, one equipped to manage and avoid changes in environmental conditions during flight. A pilot who possesses this rating is a better life insurance risk!

Each carrier has its own criteria for determining the “aviation risk” or extra mortality charges that may come in the form of a Flat Extra premium or a downgrade in underwriting class (Standard versus Preferred) or a combination of both.

If you have clients that do not want to pay for Aviation Risk in their life insurance policies, many of our carrier partners offer aviation exclusion riders as an option.

The best way to begin a case with a client who is a pilot is to have them complete our AgencyONE Aviation Questionnaire. With this important data, AgencyONE will find you and your client the most competitive rate class.

AVOCATION & UNDERWRITING

You may also have clients who love adventure. Hobbies like rock climbing, mountain climbing, scuba diving, drag racing, and heli-skiing are great fun, but the enjoyment they offer can add quite a bit of cost to your client’s life insurance premiums. As in medical underwriting, carriers can view the same information very differently. If your client answers “yes” to any of these questions, it is very important to request and complete the specific avocation questionnaire(s) that apply. To find these questionnaires, log into theAgencyONE website to access your Advisor Dashboard and navigate to the Underwriting drop down tab. AgencyONE can discuss exclusion options, if available, or provide details to our carriers so we can negotiate with them to obtain the most favorable rates available for your clients.

UNDERWRITING AVOCATION – CASE STUDY

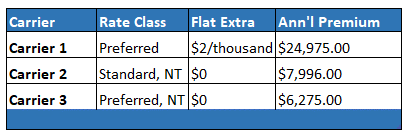

Harry Daredevil is a 35-year-old executive with no significant medical history. He has a student pilot license and has logged only 12 hours of flight time over the last year. He intends to fly an additional 30 hours over the next year and complete the requirements to get a Private Pilot certificate. Mr. Daredevil is applying for $10M of TERM coverage and does not want to exclude aviation from the risk.

AgencyONE sent the pertinent details to several of our carrier partners. Some carriers will maintain a standard rate class regardless of medical history while others may allow a preferred offer with a Flat Extra rating. EIGHT – but not all – carriers wanted to charge between a $2 and $3 Flat Extra premium, per thousand dollars, for the entire duration of the TERM coverage!

Take a look at the premium difference between carriers:

Each avocation risk is unique and requires special consideration and handling. Regardless of your client’s special avocation, AgencyONE’s goal is always the same – to obtain for your client the lowest possible rating class BOTH medically AND for the avocation risk. Give AgencyONE a call the next time you “gotta guy” who pilots a plane, rock or mountain climbs, scuba dives, or has dreams of flying to the moon! AgencyONE can get them underwritten for you.

We hear you loud and clear! The traditional underwriting process often presents many challenging hurdles – lengthy applications that include multitudes of invasive and personal questions, varying carrier requirements including blood, urine, EKGs, and the time-consuming attempts to get APS information. It can take MONTHS to get everything required to approve a policy!

Insurance companies are regulated by the individual states (NAIC State Insurance Regulation) in which they are licensed to sell insurance AND operate under specific requirements outlined in their reinsurance treaties. They are audited regularly. Like it or not, all underwriters are REQUIRED to ascertain specific information to assess mortality accurately and approve the desired death benefit.

That said, AgencyONE’s carrier partners are equally frustrated with the time-consuming underwriting process. As a result, they have developed many NEW and IMPROVED life insurance opportunities for you to offer your clients, with much LESS invasive or NO underwriting at all.

This ONE Idea addresses the opportunities to add coverage to your client’s existing portfolio OR to apply for new coverage with LITTLE TO NO UNDERWRITING!

Opportunities If You Have Sold Life Insurance To Clients In The Last Three To Five Years

Add More Insurance Coverage

Did you know that programs are available that allow you to add more coverage using older underwriting requirements? You may have clients with policies that are a perfect fit for these programs. It is time to take a look at your existing book of business!

Basics: The programs that allow you to add coverage require the in-force policy to be fully underwritten at an approved carrier within the last three to five years at standard rates or better. Depending on the carrier, these programs offer additional Permanent coverage equal to the face amount of the existing policy up to $1M, $2.5M or $3M, with a maximum age of 65.

Case Example: Cheryl Smith bought a $2MM, 10-year Term key-person policy two and a half years ago. Since that time, Cheryl bought a new house and got married. Cheryl’s life changes prompted the need to increase her personal coverage. Her Advisor suggested one of our top carrier partner’s Term Plus Perm Program. The new insurance company was able to use Cheryl’s old labs and ran the MIB, Script Check and MVR. Cheryl was approved and purchased an additional $1MM UL policy with a Long-Term Care Rider – WITHOUT A NEW EXAM OR LABS AND IN LESS THAN TWO WEEKS!

External Conversion or Exchange Programs

If you have a client with Term coverage in-force at a carrier with limited conversion options OR Permanent coverage in-force at a carrier with an uncertain future, your clients have options to consider for policy conversion or exchange.

Basics: With External Conversion Programs, your client will surrender the original policy for a new one. Perhaps your client was enticed by the new carrier’s product specifics – a rider, better pricing, longer guarantees, or better company ratings. Generally, the face amount for the new policy will match the existing policy up to $1M and up to age 65. The original policy must have been fully underwritten at an approved carrier within the last three to five years at standard rates or better.

Case Example: Seth Gold is a 56-year-old attorney who bought a fully underwritten $1MM, 10-year Term policy four and a half years ago at Preferred rates. During his annual planning review, Seth was advised to purchase Permanent coverage. Because he was not satisfied with the conversion options at his policy’s existing carrier, Seth’s Advisor suggested a Term to Perm Exchange program with a different carrier. Within two weeks, Seth was able to exchange his Term coverage for an IUL policy which included an imbedded chronic illness rider – WITHOUT GOING THROUGH FULL UNDERWRITING!

Underwriting Options For New Insurance Coverage

Accelerated Underwriting – more options, higher face amounts, NO LABS and fast approval!

We refer to accelerated underwriting (AUW) as a yes/no, lab-free, algorithmic-based program. The first AUW program hit the market in 2014 and since then, many carriers have followed suit. These programs have historically been geared toward your healthier clients under age 60. This is generally still the case; however, the face amounts being considered have INCREASED quite a bit! Today, we have carrier partners who are approving applicants through age 50 for up to $5MM and up to age 60 for $3MM – using ONLY the application, telephone interview, MIB, MVR, Script Check, etc. to underwrite the case. Some carriers offer an entirely digital experience!

Expedited Underwriting – expanded options, older ages, higher face amounts, with NO LABS!

During COVID, getting an insurance exam became extremely challenging. Carriers had to pivot to get business placed. Those who had been piloting alternative data sources like patient portals, electronic health records, lab data, etc. had to quickly incorporate these tools into their underwriting. We also saw carriers temporarily modify their established AUW guidelines. These modifications allowed cases to be approved at higher ages and face amounts WITHOUT an insurance exam IF the carrier could procure enough recent medical information to satisfy the exam requirements (labs, build, blood pressure, smoking status, etc.) through these alternative data sources. In many instances, particularly with the Human API portal data, we were able to obtain what we needed to approve the case in minutes!

What began as a “temporary” fix to the insurance exam issue, as a result of COVID, has now become a part of the permanent guidelines at many carriers. Expedited or frictionless underwriting sets parameters (age, face amount and other criteria) and allows an underwriter to use digital or clinical data (including the traditional APS) to satisfy exam requirements. We now have an opportunity to issue up to $10 Million of coverage, up to age 70, WITHOUT AN INSURANCE EXAM if the client has had a physical and labs within the last twelve months! (And for higher net worth individuals who receive executive physicals, we may be able to secure even MORE coverage through Executive Underwriting Programs).

Updated Tool for You!

Please review the updated Accelerated Underwriting Programs spreadsheet which includes ALL the new and expanded carrier programs. You can always find the most current version on the AgencyONE website on your Advisor Dashboard in the Underwriting drop-down tab. There are SEVERAL hyperlinks there which will direct you to additional information.

Underwriting Has a Shelf-Life – “We Aren’t Selling Bicycles!”

The insurance solutions you offer are VERY meaningful to the families and businesses they protect. AgencyONE strives to get your clients’ insurance coverage in place as quickly and efficiently as possible. Underwriting delays can have serious repercussions – especially if your client experiences a health change, or worse, before the policy is placed in force.

We work with our AgencyONE 100 Advisors to prevent delays by helping them identify and Ask The Necessary Questions, be aware of and understand the available underwriting programs, and to foster engagement among all of the involved parties. Let AgencyONE’s underwriting team help you – we have all the information you need at our fingertips!

Please contact AgencyONE’s Underwriting Department at 301.803.7500 for more information or to discuss a case.

AgencyONE’s weekly ONE Ideas are designed to discuss a range of industry topics that are linked to current trends in Advanced Markets, Case Design, and Underwriting. There has been a lot of activity within the industry over the last 6 months (COVID, the election, ongoing interest rate pressures, and product changes) so this week’s ONE Idea will offer a RECAP for this past month with links to the full copy of each AND a list of all of our published ONE Ideas since the beginning of 2021 with a hotlink to the full article.

JUNE ONE IDEA RECAP

We started out the month with an Underwriting ONE Idea on June 4th entitled You Want Preferred Offers? You Need to Understand Preferred Criteria! This well-written ONE Idea from our underwriting experts discusses the details of a PREFERRED rating and WHAT the carrier expects to place the offer. This ONE Idea provides a deeper understanding of the rating and is intended to help you have meaningful and educated conversations with your clients while setting the proper expectations at the outset of the case.

Our second ONE Idea for the month came From the Desk of Gonzalo Garcia, CLU on June 11th and is entitled End of Term Insurance Period STICKER SHOCK! This article discusses what happens to Term policies at the end of their term period, the Annual Renewable Term rate that goes into effect and the various product options and carrier restrictions that the advisor and the insured need to understand. The assistance of a savvy advisor is CRITICAL to helping the client establish his/her financial needs and goals, and to understand the impact of physical health on the renewal or conversion of a policy.

ONEIdea number three for the month came From the Desk of Ed Stark, CLU, ChFC on June 18th and is entitled A Premium Finance Insurance Case (with options) That Went Well! This article highlights examples of the Premium Finance cases we see at AgencyONE, why advisors and clients like the Premium Finance option, the difficulty in illustrating a Premium Finance case, and a case study that shows the detail that goes into planning and executing a successful Premium Finance case.

SIX MONTHS OF ONE IDEAS

Following is the list of all ONE Ideas from January to May 2021:

Each of these ONE Ideas is meant to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciated the opportunity to serve you and your clients.

Please contact AgencyONE’s Marketing Department at 301.803.7500 for more information or to discuss a case.

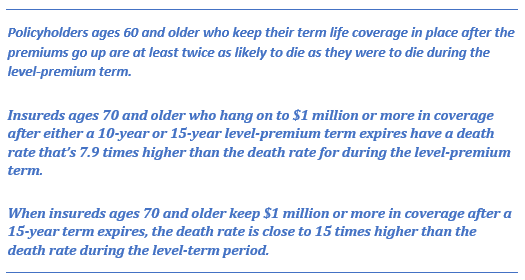

Have you ever had a client who came to the end of their level term insurance period and then got a renewal notice that made them happy? More than likely, they were very upset and called you expressing “End of Term Insurance Period STICKER SHOCK!”

LEVEL TERM PREMIUM TO ANNUAL RENEWABLE TERM

Most carriers change from a level term premium during the term guarantee period to an annual renewable term (ART) rate, considering the insured’s attained age at that time. The problem? Since there is no new underwriting upon renewal, the carrier charges rates that are reflective of a much higher risk profile. This higher risk profile translates to possibly a lot more money AND the “End of Term Insurance Period STICKER SHOCK!” The reality of course, is that most clients who are still healthy enough and need continued coverage, (at the advice of their insurance advisor), will not pay the increased premium and WILL subject themselves to underwriting to obtain “freshly underwritten rates” that are more reflective of their health status for another guaranteed term policy. If they are not healthy, and feel they need life insurance coverage going forward, they will exercise their conversion privilege OR continue to pay an ever-increasing premium at the high (ART) rates.

SOCIETY OF ACTUARIES STUDY

A May 2021 study, commissioned by the Society of Actuaries from SCOR Global Life USA Reinsurance Company (SCOR), may provide some answers and shed light on many issues affecting the direct writing carriers today. Of note and the purpose of this ONEIdea is that it may explain many of the pricing and conversion option decisions being made as a result of some of the findings and how you can advise your clients.

Allison Bell’s June 4th article for Advisor Magazine entitled “When Term Life Policyholders Leave the Level-Premium Bubble” notes two significant statistics from the SCOR study and concludes that “consumers who face a huge premium increase turn out to be good at judging their health”.

Ms. Bell notes that:

Indeed, when a consumer reluctantly pays for “substandard rates on an increasing basis”, they often know the end is near.

A PERSONAL STORY

When my aunt was in hospice some years ago and in her final days of life, it coincided with the expiration of a 20-year term policy that she had purchased. In fact, her 21st year renewal billing statement was sitting in her mailbox when I was visiting her. My uncle asked if he should pay the increased premium, to which I, of course, replied with an emphatic “YES”! The premium was almost 5 times what her level premium had been, but it was the best “investment” my uncle ever made since the company was obliged to pay the death claim a few days later.

TERM CONVERSION PREDICAMENT

This same predicament is being felt by insurance companies, and has been for some time, on conversions. Most clients who know that they are not healthy and can still convert their policies will do so, to avoid the uncertainty of an increasingly burdensome premium requirement at the end of the term period.

Claims experience from many, if not most, insurance companies has not been favorable on term conversions for many of the same reasons….consumers are good at judging their own health and often know something is “not right” with their health.

It is no wonder that carriers DO NOT WANT customers to do what the industry calls “late term conversion” and have taken steps to change their conversion period or limit the products available for conversion. More and more we are seeing long term durations limit the years in which a client can convert a policy or, alternatively, limit the product options available to a client for conversion. Most often, the product limitations are very expensive and take into consideration impaired mortality.

In a recent conversation with a carrier who will remained unnamed, I was told point blank that they favored early conversions, but “late term conversions” were a real problem for them.

It is also no wonder why life settlement companies are so interested in buying policies from consumers just prior to the term expiration period and converting them to a permanent policy. Settlement companies are investors, and they are looking for returns – BIG returns. So, much to the insurance company community’s chagrin, it makes sense that life settlement companies are looking for clients who do not want their old term policies and are NOT in good health.

LOOK BEYOND PRICE

Today more than ever, advisors should look beyond price when making recommendations for term insurance to their clients. I cannot tell you how many times I have received telephone calls from advisors asking if I can help them get an exception for a client whose guaranteed term period or conversion privilege has expired, and the client is not in good health, maybe completely uninsurable. The answer is “NO”. Insurance companies know that these cases are claims waiting to happen well before they priced for them.

Term conversion privileges vary greatly from company to company. When making term recommendations, look for the following:

How long the conversion period is relative to the term period. Most carriers do not allow conversion for the full-term duration, in fact many carriers limit this option rather dramatically.

Carriers that offer term products that allow conversion to ANY product they offer. Beware of a carrier who offers a conversion period but only allows that the client convert to a “conversion product”. These products are generally priced significantly higher than a fully underwritten product, often as high as 200% more in mortality charges.

The availability of a conversion extension rider. If a carrier offers this rider, consider recommending it to your client with the understanding that it comes at an additional cost. This will offer your client options should they find themselves in impaired health as they near the end of their term guarantee period.

AgencyONE’s sales support team monitors and tracks carrier conversion data and can help you advise your clients and direct them to the best carriers and products according to their financial and insurance needs.

Please contact AgencyONE’s Marketing Department at 301-803-7500 for more information or to discuss a case.

I typically see Premium Finance cases in the concept stage and probably see about 3-4 of these cases per week. A lot of advisors would like to offer Premium Finance to their high-net-worth clients who need insurance, but not every case makes the cut. In this week’s ONEIdea we discuss a Premium Finance insurance case – with options – that went well!

THE PREMIUM FINANCED CONTRACT

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the linked blog post from Gonzalo Garcia, CLU). Others are actual Premium Finance cases that have been discussed in detail with the advisor and client who like the strategy of using leverage to obtain the required financial and insurance goals.

THE ATTRACTION OF A PREMIUM FINANCE CASE

Advisors continue to show Premium Finance cases because they are typically LARGE, and they appeal to high-net-worth clients who like the idea of borrowing funds to pay for the life insurance rather than liquidating existing investments. The majority of the cases we see at AgencyONE request a design where the client:

pays as little as possible;

posts NO collateral;

pays minimal interest; and

pays off the loan using the value in the policy.

ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

One reason is that the typical criteria for the sale is NOT REALISTIC! It is best for clients to have some “skin in the game” and to be prepared to pay interest annually and post the needed collateral AT A MINIMUM. The more the client contributes to a Premium Finance case the more likely the policy will perform as designed and remain viable to help the client “weather” any down years that might impact the contract. Benefits of the client financially contributing to a Premium Finance deal are:

flexibility on borrowing amounts;

flexibility on years to borrow;

ability to exit the loan earlier and more efficiently; and

less risk to the policy over time.

ILLUSTRATING PREMIUM FINANCE DESIGNS UNDER AG49A

Limits are set on the allowable max index rates and also for par loans. When par loans are used the crediting rate of the policy is restricted to 50 basis points higher than the par loan rate. Example – a 5% par loan restricts the crediting rate of the illustration to 5.5%. Real performance is not affected, but these AG49A restrictions are an issue for some advisors since we are not permitted to show anything above the established illustration parameters.

A PREMIUM FINANCE INSURANCE CASE (with options) THAT WENT WELL

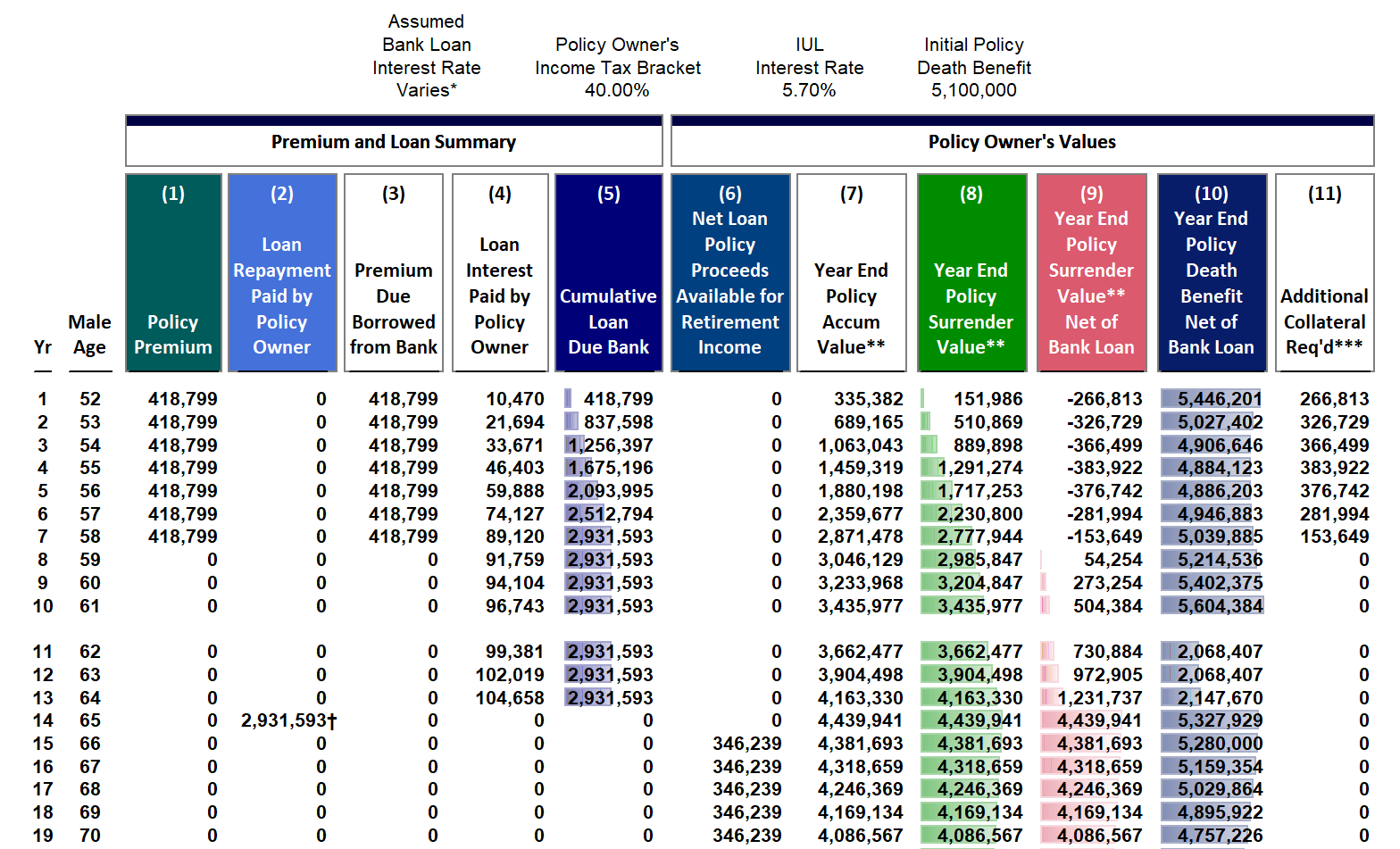

Recently, an AgencyONE 100 advisor presented a 52-year-old male client who was heavily invested in real estate and needed about $5,000,000 in life insurance coverage. The client had plenty of net worth but not much available cash for paying the insurance premiums. The client was in a position to pay the interest but was concerned about how he could exit the loan efficiently. The original request from the agent was to use a participating policy loan to pay off the bank loan. I explained that this design just MOVES the loan from the bank to the life insurance policy. The burden of the loan still exists but is shifted elsewhere. I then explained the risks of leaving the loan inside the policy. The contract would have to continue to perform and maintain positive cash value for the life of the insured to make this plan work. If the policy were to lapse, a huge taxable event would occur for the policy owner. The advisor and client were not comfortable with this possibility, so we continued to discuss the case and other available options.

PREMIUM FINANCE ALTERNATIVE OPTION #1

Discussions between the advisor and client revealed that the client had been considering selling some of his real estate rental properties in the next 10 -15 years. Could he use the sale proceeds to pay off the bank loan? This plan would leave the client with a cash-rich life insurance policy that could generate tax free income down the road. On the other hand, If the real estate sale proceeds were deposited into a brokerage account (instead of an IUL life policy) the growth would be taxable – an unacceptable and avoidable option.

AgencyONE uses Insmark to illustrate Premium Finance cases. The Insmark illustration below shows the client borrowing an annual premium of $418,799 per year for 7 years. Since the client was not using the policy value to pay off the loan, he was able to borrow LESS. The client pays all the interest along the way AND pays the loan off by selling a portion of his rental property. He can then take withdrawals to basis/standard loans from the policy of approximately $346,239 per year for the years 15 to 38 –

The finance sheet above has quite a bit of useful information: premiums borrowed, projected interest payments due, cumulative loan, policy values, and additional collateral required in the right-hand column. The advisor and client were amenable to paying interest but were unsure about the additional collateral required (column 11). To address this concern, AgencyONE presented another option for the client to consider.

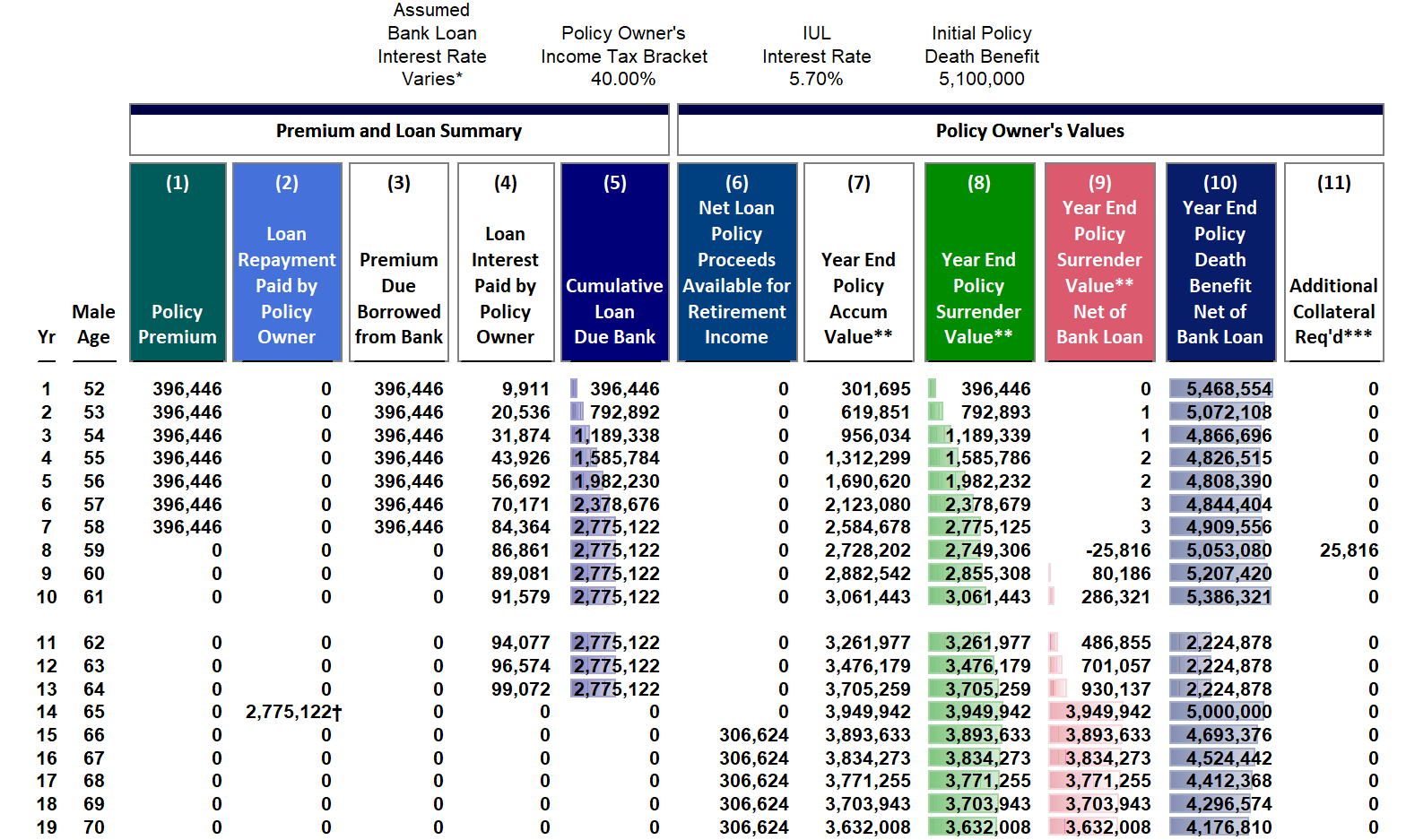

PREMIUM FINANCE ALTERNATIVE OPTION #2

In this scenario, we added an Early Cash Value (ECV) rider to the contract that would OFFSET the collateral requirement the client was required to pay (except for a small projected amount in year 8). The addition of the ECV rider:

LOWERED the borrowed amount;

impacted advisor compensation by spreading comp over 4 years;

added a chargeback provision; and

also reduced the projected income to the client by $39,615 per year.

The ECV rider will, however, provide the full 100% Cash Surrender Value (CSV) to offset the collateral through year 7.

BUT, is adding the ECV rider to avoid posting collateral worth losing a projected $950,760 of income over the time period illustrated, years 15 to 38? This depends upon client preference and requires detailed discussions between the advisor and the client. The AgencyONE 100 advisor presented both options to the client for review.

AgencyONE’s Advanced Markets and Case Design Team possess the knowledge and expertise to assist with all of your Premium Finance cases. We are available to talk concept, design, and implementation, AND we have strategic relationships with funders, such as US Bank, who can assist with lending on your cases.

Please contact AgencyONE’s Case Design Team at 301.803.7500 for more information or to discuss a case.

We get it. You are out there pounding the pavement, finding clients, convincing them YOU are the ideal advisor to help with their financial planning needs. YOU want to deliver the best solutions from the right carriers who offer the most affordable premiums. YOU are competing with that “other advisor” who always shows best class numbers whether they are warranted or not and tries to convince your client that he or she can do better. At the same time, you are contending with on-line and TV ads that offer “quick and easy” insurance products. AgencyONE recognizes that your GOAL is to deliver only the best product and price to your clients, ideally at PREFERRED or BEST CLASS offers. BUT if you want PREFERRED Offers, you need to understand PREFERRED criteria!

KNOWLEDGE IS POWER – ARM YOURSELF

Understanding preferred criteria arms YOU with the information you need to have meaningful, educated conversations with your clients. YOU can set realistic expectations and demonstrate a greater depth of knowledge while ENGAGING your clients in the underwriting process. In this ONE Idea, we are going to take a closer look at what goes into a preferred offer and WHAT AND HOW you need to communicate with your clients.

THE DEVIL IS IN THE DETAILS

Assuming your client does NOT have a ratable medical impairment, avocation, occupation, foreign travel or driving record, meaning they are considered a true STANDARD RISK, AgencyONE looks at a carrier’s preferred criteria to see where the client can qualify for the best possible rate class. This allows YOU to deliver the desired product at the most economical cost. The number of preferred classes (Standard Plus, Preferred, Super Preferred, etc.) and the parameters around each vary from carrier to carrier. Typically, preferred criteria includes specific metrics around:

BuildBlood Pressure

Cholesterol

Tobacco Use

Family History

Foreign Residence and Travel

BUILD

The COVID pandemic has kept a lot of us away from the gym and possibly snacking a bit more than usual, and the result may have been unwanted weight gain. A 10-to-15-pound weight INCREASE can result in a rate class DOWNGRADE! Did you know, for any recent and significant weight LOSS, most carriers will add half of the weight BACK until the weight loss has been maintained for an entire year? Each carrier has MULTIPLE build charts. In addition to preferred build criteria, carriers may have DIFFERENT parameters for males and females, Accelerated Underwriting Programs, Long Term Care Riders, TERM, UL, and Hybrid products. Many carriers underwrite by your Body Mass Index (BMI) which you can calculate here. Clients considered UNDERWEIGHT (generally a BMI < 18) can also be knocked out of preferred classes!

SO, WHAT SHOULD YOU DO?Be specific with your clients. EXPLAIN WHY you need their ACTUAL weight, not their GOAL weight, and how this information can translate into premium dollars. AgencyONE has all the necessary information at our fingertips and can help guide you and your clients toward the ideal carrier.

BLOOD PRESSURE

A “normal” blood pressure reading can vary depending on who you ask, but 120/80mm/Hg is typically the means for comparison. The preferred parameters for blood pressure readings differ for each carrier, each rate class, the age of the client, and in some cases, if the clients are treated for hypertension. Many carriers will average 12 months of blood pressures to determine your client’s class qualification.

SO, WHAT SHOULD YOU DO? If your client says that he or she has high blood pressure, ask how well it is controlled. If your client takes medication, remind him or her to TAKE IT as prescribed leading up to AND on the morning of the insurance exam. Advise your client to LOOK at the examiner’s blood pressure reading, and if it seems higher than is normal, REQUEST IT BE TAKEN AGAIN. Understanding the economic impact of the blood pressure will help your clients engage.

CHOLESTEROL

Total Cholesterol and cholesterol ratio are considered with preferred criteria. [The cholesterol ratio is total cholesterol divided by HDL (good cholesterol)]. These parameters also vary by carrier, rate class, age, and if the client is treated for high cholesterol. Although not typically included in preferred criteria, an elevated triglyceride level can also affect underwriting offers.

SO, WHAT SHOULD YOU DO? If your client says that he or she is on a statin for their cholesterol, ask them how well it is controlled. Explain how the cholesterol readings on the insurance exam can COST or SAVE your client money. Encourage your client to watch his or her diet and alcohol intake leading up to the exam, and to make sure to take any recommended medication regularly.

TOBACCO USE

If your client used to smoke cigarettes and has quit, it can take anywhere from 1 to 5 YEARS to qualify for a preferred or best class offer depending on the carrier. There are differing parameters around cigars, dip, chew, Nicorette Gum…. even marijuana smoking.

SO, WHAT SHOULD YOU DO? DISCLOSURE is EVERYTHING. Make it VERY CLEAR to your clients that you need ALL the details. If your client quit smoking cigarettes recently, get the actual quit DATE (most people know it). If your client tells you that he (or she) smoked a cigar on the golf course – find out how often and when your client had the last “puff”. The fact is, there are carriers that will take cigar, dip, chewers, Nicorette users at their lowest preferred class (Standard Plus band) and NON-tobacco rates, even with nicotine in the urine…as long as they know it IS NOT from cigarettes. With Marijuana – same story – preferred rates are possible. Disclosure and frequency of use are imperative details to collect and will help AgencyONE point your case in the right direction.

FAMILY HISTORY

Your genes matter! Carriers look at the age and cause of death for an applicant’s parents and sometimes his or her siblings. Many carriers will not offer ANY client preferred or preferred best classes if he or she has ONE parent that passed away prior to age 60 to 65 from cancer or heart disease. There are carriers that ignore family cancer histories all together, some that will offset family cardiac histories if the applicant has had certain medical testing, and other carriers that will consider a preferred offer if ONLY ONE parent died before age 60. Some carriers throw these parameters out of risk assessment entirely once the applicant reaches” insurance age” 59, while others never do. The guidelines are “all over the place” with family history!

SO, WHAT SHOULD YOU DO?Ask your client if anyone in his or her immediate family passed way. If so, what was their relationship to the insured, age, and cause of death? Again, AgencyONE uses this very important information to guide you and your client towards the best carrier for your case.

CASE STUDY

Client: John Smith, 59-year-old male applying for $5,000,000 of 10-year Term, Key Man coverage Build: 6’3” in height, 245 pounds Blood Pressure: Normal, averaging 123/82mm/Hg Cholesterol: 293 HDL 50 – TC/HDL ratio of 5.86 on the insurance exam Tobacco: Non-smoker Family History: Father was a heavy smoker, passed away at age 57 from heart attack

AgencyONE HAS YOUR BACK

We have created several tools to make gathering and relaying this information easier. Our AgencyONE Informal Inquiry and Exam Prep Video provide detailed information about what is required to start the underwriting process. Good, clear communication between advisor and client is extremely important. Explain WHY the details matter and how accurate collection of the details will very likely save your client time and money.

AgencyONE’s Underwriting Team has many years of well-regarded experience, deep carrier relationships, knowledge of underwriting guidelines, and a mastery of carrier niches to direct your client’s cases to the RIGHT CARRIER at the RIGHT PRICE EVERY TIME! We are COMMITTED to providing you and your clients with exceptional underwriting, competitive offers, and extraordinary back-office support.

At the time of writing this, 2021 is already half over and AgencyONE was seeing quite a few of our carrier partners introduce their compliant Section 7702 IUL options. From a design standpoint, our case design team has noticed that the initial face amounts generated are noticeably lower and the income is higher based on the 7702 changes. Some advisors have expressed concern that their clients are sacrificing too much death benefit for such a small increase in projected income. This week’s ONEIdea will discuss death benefit design options using Section 7702 products.

PROJECTED INCOME – TRUE MINIMUM NON MEC DESIGN

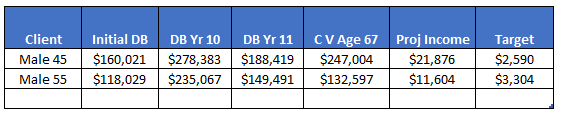

If projected income is the most important aspect of the sale, than a true minimum non mec design will provide the highest possible income for your client (Click here for a FAQ and explanation of MEC). This design requires leveling and dropping the death benefit at the end of the premium payment period to further maximize the design. Let’s consider two different ages since these comparisons perform differently based on age. Assume the following:

Male 45 and Male 55, both preferred non-tobacco

$10,000 premium for 10 years; then a maximum death benefit drop in year 11

Income from ages 68 – 85 using withdrawals to standard loans

Maximum carrier AG49 rate

The table below shows a true minimum non mec design illustrated today:

The information set forth in the table above does not allow any extra room for additional funding and also does not provide much death benefit, if needed. Many of our AgencyONE 100 advisors prefer to have additional cushion built into the death benefit so that their clients can increase premiums down the road. While they do not keep a policy optimally funded, the new product versions offer clients the option to increase future premiums.

DOUBLE MINIMUM NON MEC FACE AND MAINTAIN PREMIUM

Another scenario to consider is to keep the premiums the same but double the previous minimum non mec face to see what that looks like. The table below explores this option:

TWO SCENARIOS – DIFFERENCES

The main differences between the two comparisons above are that the face amounts are higher for 10 years in one scenario but then drop quite a bit after the reduction to the corridor limits in year 11. Cash values are lower which cause the income to also decrease. Target is 2X the minimum non mec amount. Even though the design builds in premium and allows room for the client to increase the funding later, it drags down the values. There is too much death benefit for the premium paid and, if the client does not increase the funding of the policy, it will impact the policy’s future values in a negative way.

A BALANCED OPTION

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

RESULTS OF A BALANCED OPTION

This balanced option provides more initial death benefit and only slightly impacts the cash values and income. The percentage drops are within a more acceptable range and allow the clients to increase contributions down the road as their income levels increase. This design gives the client more options without impacting the cash value and income – as much as the doubling of the face amount scenario. Is the small decrease in values worth the extra death benefit trade off? Only you and your client can decide that.

AgencyONE’s Case Design Department is very well-versed in carrier product intelligence, has an exceptionally high degree of case design experience, and stands ready to assist our AgencyONE 100 Advisors and their clients in considering the best death benefit design options using Section 7702 products.

Medical Underwriting today requires two very different phases of assessment with the variety of living benefits currently offered and sold. While AgencyONE is consistently estimating MORTALITY for the life product, closer attention to your client’s MORBIDITY risk is required when Long-Term Care or Chronic Illness Riders are part of the case. These two phases of assessment may be why you are asking the question – WHY is My Client a Preferred Life Risk, but Declined for Long-Term Care?

MORTALITY VS MORBIDITY

Simply put, when underwriting MORTALITY, the focus of our medical assessment is on the probability of DEATH. However, the probability of becoming disabled exceeds that of death. To go on a Long-Term Care claim, the applicant must demonstrate an inability to perform two of six activities of daily living (bathing, continence, dressing, eating, toileting, transferring), or have a severe cognitive impairment. As such, when underwriting MORBIDITY, we are looking at conditions that could result in a long-term need for different levels of convalescent care. There is a greater focus on an applicant’s OVERALL state of HEALTH and FUNCTIONALITY, and how it could impact their ability to care for themselves.

In this ONE Idea, we are going to walk you through some of the differences in underwriting and demonstrate how knowing the CORRECT carrier for mortality AND morbidity can greatly impact the success of your case.

LONG-TERM CARE RIDERS (LTC) VS CHRONIC ILLNESS RIDERS (CIR)

A traditional LTC rider is underwritten similarly to a life insurance product. Impairments are carefully vetted and offers can range from preferred to a table rating, SEPARATE from the life offer. Chronic illness riders fall into a “yes” or “no” category. Many have a short “knock-out” list, but if the life offer is table D/4 or better the rider generally CAN BE included.

A FEW MORBIDITY RED FLAGS

Osteoporosis is a metabolic bone disorder which results in a reduction of bone mass. As the bones deteriorate, they weaken which can lead to fragility and fractures. Bone density is measured by a test called a DEXA scan. The severity of osteoporosis is underwritten based on that score and/or a history of falls and fractures. Osteoporosis would not generally affect the life offer, but it ALWAYS puts LTC offers and insurability at risk.

Recent surgery, particularly ORTHOPEDIC, would only affect the life offer if a complication or chronic pain component existed. The TYPE of surgery alone can make your clients uninsurable for a traditional LTC rider. Certain carriers will DECLINE LTC for applicants who have had spinal fusions, multiple back surgeries, or joint replacements because of chronic osteoarthritis.

Physical therapy is a treatment commonly found in medical records for a multitude of reasons. We would not give this a second thought if your client is applying for a life product alone. However, clients actively receiving physical therapy are declined for LTC for about 6 months after it concludes. Then, ratings would depend on WHY physical therapy was ordered and how the client is functioning thereafter.

COVID “long haulers” continue to emerge and many have residual physical and emotional symptoms. For now, each applicant will be handled on a case-by-case basis; however we anticipate guidelines for LTC/CIR and life underwriting will continue to evolve.

A WORD ON COMORBIDITIES

Comorbidities are the presence of two or more diseases and/or medical conditions. Often, one condition has the potential to make the other worse. For example, an applicant with diabetes who is also obese may have a more difficult time controlling his/her blood sugar and cholesterol, is less likely to be exercising, and could be considered a less favorable risk. Underwriters like long-term stability when it comes to ANY chronic condition. When your clients present with comorbid conditions, the “big picture” is scrutinized more closely. Greater attention is paid to the individual’s:

build;

lifestyle and social habits;

medical surveillance and follow-up;

compliance with treatment; and

mental health history, cognition, and social support.

NOT ALL CARRIERS UNDERWRITE LTC THE SAME – CASE STUDY

Jane Smith is a 59-year-old, nonsmoking female applying for a $1MM policy with an LTC rider. She has a history of high blood pressure and high cholesterol which is medically managed and well controlled. Jane had in-situ breast cancer 10 years ago without recurrence, is postmenopausal, and has suffered bone loss. Calcium and vitamin D supplements are a part of her regular regimen and she has no history of falls. The APS indicates Jane exercises regularly, is up to date with screening mammogram, PAP testing, and colonoscopy. Her recent blood work is normal and most recent DEXA scan showed her greatest bone loss at -2.9, which indicates that Jane has osteoporosis.

We know immediately that at least TWO carriers would DECLINE the LTC rider due to the DEXA score and that one may be MORE competitive on the life offer with this history. AgencyONE presented the case to the two companies we felt would be most competitive for this client:

$1MM UL policy, all pay to age 100, LTC at 2% – LTC benefit $20K monthly.

IF LTC OR CIR IS A PART OF THE CASE, WE NEED TO KNOW UP FRONT!

It is imperative to let us know up front when LTC or CIRs are included in the case. This changes the path of the case, not only in the APS information we need, but which carriers we price and recommend for your client. Details about your client’s lifestyle that will provide the carriers with an accurate and holistic representation of the case are also very important to include.

Long-Term Care and Chronic Illness Riders offer an extremely valuable benefit for your clients. If you are not talking with your clients about these options, START NOW. Our case design team are experts with the various products available. Together, we can help you choose the ideal carrier(s) AND negotiate the offer your client deserves.

protection against risk, properly structured temporary and permanent life insurance coverage can help mitigate the risks to which HNWFN are exposed – including generational wealth transfer and taxation on their worldwide income and assets.

protection against risk, properly structured temporary and permanent life insurance coverage can help mitigate the risks to which HNWFN are exposed – including generational wealth transfer and taxation on their worldwide income and assets. Taxation issues may arise for couples when one partner is NOT a US citizen and become problematic upon the death of one spouse. Most clients are NOT aware that taxes will be due …until the IRS letter arrives! The solutions to this problem lie in strategic estate planning and the necessary life insurance protection.

Taxation issues may arise for couples when one partner is NOT a US citizen and become problematic upon the death of one spouse. Most clients are NOT aware that taxes will be due …until the IRS letter arrives! The solutions to this problem lie in strategic estate planning and the necessary life insurance protection.

We often say at AgencyONE that the details will make or break a case. The HNWFN market is exciting, challenging and rewarding. Term and permanent coverage are available from many carriers, but it is CRITICAL to understand the carrier NUANCES – there are MANY. The HNWFN platforms that the carriers offer are unique in that they are even MORE competitive than the products offered. Securing coverage is the key and AgencyONE has the KNOWLEDGE and RELATIONSHIPS to direct your client to the right carrier!

We often say at AgencyONE that the details will make or break a case. The HNWFN market is exciting, challenging and rewarding. Term and permanent coverage are available from many carriers, but it is CRITICAL to understand the carrier NUANCES – there are MANY. The HNWFN platforms that the carriers offer are unique in that they are even MORE competitive than the products offered. Securing coverage is the key and AgencyONE has the KNOWLEDGE and RELATIONSHIPS to direct your client to the right carrier!

the SAME mortality risk as a non-pilot, meaning they would be underwritten at the top Preferred class in which they qualify. Some licensed pilots also fly PRIVATE, which CHANGES the risk perception for insurance companies.

the SAME mortality risk as a non-pilot, meaning they would be underwritten at the top Preferred class in which they qualify. Some licensed pilots also fly PRIVATE, which CHANGES the risk perception for insurance companies. VISUAL FLIGHT RULES (VFR) mean that the aircraft is intended to operate in Visual Meteorological Conditions (VMC), i.e., clear skies, nice weather, ideal visibility. Fog, heavy precipitation, low visibility, and otherwise adverse weather conditions are supposed to be avoided (which is why these “rules” were a big topic of discussion surrounding Kobe Bryant’s death, as the helicopter was flying under MODIFIED VFR rules).

VISUAL FLIGHT RULES (VFR) mean that the aircraft is intended to operate in Visual Meteorological Conditions (VMC), i.e., clear skies, nice weather, ideal visibility. Fog, heavy precipitation, low visibility, and otherwise adverse weather conditions are supposed to be avoided (which is why these “rules” were a big topic of discussion surrounding Kobe Bryant’s death, as the helicopter was flying under MODIFIED VFR rules). a bit of cost to your client’s life insurance premiums. As in medical underwriting, carriers can view the same information very differently. If your client answers “yes” to any of these questions, it is very important to request and complete the specific avocation questionnaire(s) that apply. To find these questionnaires, log into the

a bit of cost to your client’s life insurance premiums. As in medical underwriting, carriers can view the same information very differently. If your client answers “yes” to any of these questions, it is very important to request and complete the specific avocation questionnaire(s) that apply. To find these questionnaires, log into the Harry Daredevil is a 35-year-old executive with no significant medical history. He has a student pilot license and has logged only 12 hours of flight time over the last year. He intends to fly an additional 30 hours over the next year and complete the requirements to get a Private Pilot certificate. Mr. Daredevil is applying for $10M of TERM coverage and does not want to exclude aviation from the risk.

Harry Daredevil is a 35-year-old executive with no significant medical history. He has a student pilot license and has logged only 12 hours of flight time over the last year. He intends to fly an additional 30 hours over the next year and complete the requirements to get a Private Pilot certificate. Mr. Daredevil is applying for $10M of TERM coverage and does not want to exclude aviation from the risk.

their reinsurance treaties. They are audited regularly. Like it or not, all underwriters are REQUIRED to ascertain specific information to assess mortality accurately and approve the desired death benefit.

their reinsurance treaties. They are audited regularly. Like it or not, all underwriters are REQUIRED to ascertain specific information to assess mortality accurately and approve the desired death benefit.

During COVID, getting an insurance exam became extremely challenging. Carriers had to pivot to get business placed. Those who had been piloting alternative data sources like patient portals, electronic health records, lab data, etc. had to quickly incorporate these tools into their underwriting. We also saw carriers temporarily modify their established AUW guidelines. These modifications allowed cases to be approved at higher ages and face amounts WITHOUT an insurance exam IF the carrier could procure enough recent medical information to satisfy the exam requirements (labs, build, blood pressure, smoking status, etc.) through these alternative data sources. In many instances, particularly with the

During COVID, getting an insurance exam became extremely challenging. Carriers had to pivot to get business placed. Those who had been piloting alternative data sources like patient portals, electronic health records, lab data, etc. had to quickly incorporate these tools into their underwriting. We also saw carriers temporarily modify their established AUW guidelines. These modifications allowed cases to be approved at higher ages and face amounts WITHOUT an insurance exam IF the carrier could procure enough recent medical information to satisfy the exam requirements (labs, build, blood pressure, smoking status, etc.) through these alternative data sources. In many instances, particularly with the

Our second ONE Idea for the month came From the Desk of Gonzalo Garcia, CLU on June 11th and is entitled

Our second ONE Idea for the month came From the Desk of Gonzalo Garcia, CLU on June 11th and is entitled

Each of these ONE Ideas is meant to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciated the opportunity to serve you and your clients.

Each of these ONE Ideas is meant to help you and your clients gain a better understanding of the planning, product selection, design, and underwriting that goes into the purchase of life insurance. We hope you find these ONE Ideas helpful when assisting your clients with their financial, wealth, and estate planning needs. Thank you for entrusting your business to AgencyONE. We greatly appreciated the opportunity to serve you and your clients.

A May 2021 study, commissioned by the

A May 2021 study, commissioned by the

statement was sitting in her mailbox when I was visiting her. My uncle asked if he should pay the increased premium, to which I, of course, replied with an emphatic “YES”! The premium was almost 5 times what her level premium had been, but it was the best “investment” my uncle ever made since the company was obliged to pay the death claim a few days later.

statement was sitting in her mailbox when I was visiting her. My uncle asked if he should pay the increased premium, to which I, of course, replied with an emphatic “YES”! The premium was almost 5 times what her level premium had been, but it was the best “investment” my uncle ever made since the company was obliged to pay the death claim a few days later. Claims experience from many, if not most, insurance companies has not been favorable on term conversions for many of the same reasons….consumers are good at judging their own health and often know something is “not right” with their health.

Claims experience from many, if not most, insurance companies has not been favorable on term conversions for many of the same reasons….consumers are good at judging their own health and often know something is “not right” with their health.

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the

Some of the Premium Finance requests I see involve hypothetical cases that might be a good fit and are worth showing the client. Some are previously presented finance cases that AgencyONE is analyzing and evaluating to get a better picture of what was shown to the client (such as the one discussed in the  ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

ILLUSTRATING A PREMIUM FINANCE DESIGN CAN BE DIFFICULT

The COVID pandemic has kept a lot of us away from the gym and possibly snacking a bit more than usual, and the result may have been unwanted weight gain. A 10-to-15-pound weight INCREASE can result in a rate class DOWNGRADE! Did you know, for any recent and significant weight LOSS, most carriers will add half of the weight BACK until the weight loss has been maintained for an entire year? Each carrier has MULTIPLE build charts. In addition to preferred build criteria, carriers may have DIFFERENT parameters for males and females, Accelerated Underwriting Programs, Long Term Care Riders, TERM, UL, and Hybrid products. Many carriers underwrite by your Body Mass Index (BMI) which you can

The COVID pandemic has kept a lot of us away from the gym and possibly snacking a bit more than usual, and the result may have been unwanted weight gain. A 10-to-15-pound weight INCREASE can result in a rate class DOWNGRADE! Did you know, for any recent and significant weight LOSS, most carriers will add half of the weight BACK until the weight loss has been maintained for an entire year? Each carrier has MULTIPLE build charts. In addition to preferred build criteria, carriers may have DIFFERENT parameters for males and females, Accelerated Underwriting Programs, Long Term Care Riders, TERM, UL, and Hybrid products. Many carriers underwrite by your Body Mass Index (BMI) which you can  for each carrier, each rate class, the age of the client, and in some cases, if the clients are treated for hypertension. Many carriers will average 12 months of blood pressures to determine your client’s class qualification.

for each carrier, each rate class, the age of the client, and in some cases, if the clients are treated for hypertension. Many carriers will average 12 months of blood pressures to determine your client’s class qualification. If your client used to smoke cigarettes and has quit, it can take anywhere from 1 to 5 YEARS to qualify for a preferred or best class offer depending on the carrier. There are differing parameters around cigars, dip, chew, Nicorette Gum…. even marijuana smoking.

If your client used to smoke cigarettes and has quit, it can take anywhere from 1 to 5 YEARS to qualify for a preferred or best class offer depending on the carrier. There are differing parameters around cigars, dip, chew, Nicorette Gum…. even marijuana smoking. classes if he or she has ONE parent that passed away prior to age 60 to 65 from cancer or heart disease. There are carriers that ignore family cancer histories all together, some that will offset family cardiac histories if the applicant has had certain medical testing, and other carriers that will consider a preferred offer if ONLY ONE parent died before age 60. Some carriers throw these parameters out of risk assessment entirely once the applicant reaches” insurance age” 59, while others never do. The guidelines are “all over the place” with family history!

classes if he or she has ONE parent that passed away prior to age 60 to 65 from cancer or heart disease. There are carriers that ignore family cancer histories all together, some that will offset family cardiac histories if the applicant has had certain medical testing, and other carriers that will consider a preferred offer if ONLY ONE parent died before age 60. Some carriers throw these parameters out of risk assessment entirely once the applicant reaches” insurance age” 59, while others never do. The guidelines are “all over the place” with family history!

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

What is the best way to offer more death benefit and provide room for more premium BUT not impact the cash values and income? Some of our carrier partners have come out with basic charts that provide increase percentages based on sample ages. While fairly generic in nature, one of our carrier partners has created a special solve for this in their software. It is an option called “Balanced Solve”. This option typically falls between the 2 versions shown above. However, each case needs to be based on the agent recommendations and the needs of the client. This special solve option provides a quick way to see how the design will be impacted and what the tradeoffs are for more initial death benefit.

a Long-Term Care claim, the applicant must demonstrate an inability to perform two of six activities of daily living (bathing, continence, dressing, eating, toileting, transferring), or have a severe cognitive impairment. As such, when underwriting MORBIDITY, we are looking at conditions that could result in a long-term need for different levels of convalescent care. There is a greater focus on an applicant’s OVERALL state of HEALTH and FUNCTIONALITY, and how it could impact their ability to care for themselves.

a Long-Term Care claim, the applicant must demonstrate an inability to perform two of six activities of daily living (bathing, continence, dressing, eating, toileting, transferring), or have a severe cognitive impairment. As such, when underwriting MORBIDITY, we are looking at conditions that could result in a long-term need for different levels of convalescent care. There is a greater focus on an applicant’s OVERALL state of HEALTH and FUNCTIONALITY, and how it could impact their ability to care for themselves.

is also obese may have a more difficult time controlling his/her blood sugar and cholesterol, is less likely to be exercising, and could be considered a less favorable risk. Underwriters like long-term stability when it comes to ANY chronic condition. When your clients present with comorbid conditions, the “big picture” is scrutinized more closely. Greater attention is paid to the individual’s:

is also obese may have a more difficult time controlling his/her blood sugar and cholesterol, is less likely to be exercising, and could be considered a less favorable risk. Underwriters like long-term stability when it comes to ANY chronic condition. When your clients present with comorbid conditions, the “big picture” is scrutinized more closely. Greater attention is paid to the individual’s: